Download

1 / 40

400 likes | 551 Views

Income and Expenditure account. Introduction. Non-profit making organizations such as clubs, societies and associations usually do not have a professional and full-time accountant, the preparation of final accounts for these organization is quite different from before.

E N D

Introduction • Non-profit making organizations such as clubs, societies and associations usually do not have a professional and full-time accountant, the preparation of final accounts for these organization is quite different from before.

Receipts and payment account • It is summary of bank and cash transactions Receipt and payment account for the year ended 31 Dec XXXX Receipts $ Bank balance 1.1XX X Cash balance 1.1.XX X Membership fees X Sales of fixture X Receipts from tea or drink X X Payments $ Sports stadium expenses X Wages X Purchase of tea and drink X Sundry expenses X Bank balance 31.12.XX X Cash balance 31.12.XX X X

Preparation of final accounts • Bar trading account – to compute the bar profit (one of the income of non-profit making organization and include in I&E) • Income and expenditure account (I&E) – to compute the surplus or deficit of the organization for one year • Balance sheet – to show the financial position of the organization

Bar Trading Account • It may be called Bar Trading and Profit and loss account • Bar sales, bar purchases and expenses related to the bar operation will also be included

XXXX Sport club Bar Trading Account for the year ended XXXX $ $ Sales (wk1) X Less : COGS Opening stock X Add: Purchases (wk2) X Less: Closing stock X X Gross Profit X Less: Expense Barmen wages (wk3) X Barmen commissions X Bar expenses X Depreciation of Bar equipment X X Net profit to I&E X Expenses related bar trading only

wk1 Total Debtors Bal b/f X Cash X Sales (bal.fig.) X Bal c/f X X X wk2 Total Creditors Bank X Bal b/f X Bal c/f X Purchases (bal. Fig.) X X X wk3 Expense/income incurred = cash paid/received + prepaid last year – accrued last year – prepaid this year + accrued this year

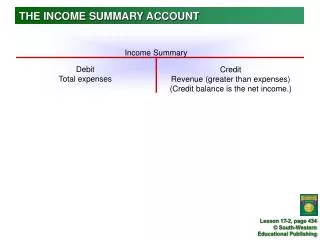

Income and Expenditure Account XXXX Sport Club Income and Expenditure account for the year ended XXXX Expenditure Income

XXXX Sport Club Income and Expenditure account for the year ended XXXX $ $ Income Income received X Subscriptions – Annual subscriptions X - Life membership fees X - Joining fees/Entrance fees X Profit on fund raising activities ( Related Proceeds – Related Expenditure )X Profit on disposal X Donations/Subsidies received X X Expenditure Expenses incurred X

$ $ Subscriptions/bad debt written off X Loss on fund raising activities (Expenditure- proceed) X Loss on disposal X Depreciation X Bar loss (from bar trading a/c) XX Surplus/ (deficit) X

Balance Sheet as at 31 Dec XXXX Cost Dep. Net $ $ $ Fixed Assets Plant & Machinery X X X M.V. X X X X X X Current Assets Bar Stock X Subscription in arrears X Prepayment X Bank X Cash X X Less:Current Liabilities Creditors – Bar purchases X Subscription in advance X Accrued expenses X Working Capital X X

$ $ $ Accumulated Fund Balance as at opening date X Add/Less: Surplus/(Deficit) of I&E X Add :Life membership fees (when life members die) X : Material donations/legacies received X X Life Membership Fund X Entrance Fees/Joining Fees X Other Fund (e.g. Training /Building Fund) X X Long-term Liabilities X X

Fund Raising Activities • The profit or loss on the fund raising activities must be computed before transferring to income and expenditure account Example Receipt and payment account Receipts Proceeds of dance party 9500 Receipts from refreshment 5000 Payments Printing of dance party tickets 500 Purchase of refreshments 4500 Sundry expenses of dance party 1020 Additional information: The opening stock of refreshments was valued at $3200 and the closing stock of refreshments was valued at $2400

Ans: Income and expenditure Income Profit from dance party (9500-500-1020) 7980 Expenditure Loss from the sale of refreshment (3200+4500-2400-5000) 300 The related revenue and expense are group together to compute profit or loss on some activities Back

Donations • Donations/Subsidies received • Ordinary donations/subsidies • Large donations/legacies Dr Bank Cr Donations/Subsidies Dr Donations/subsidies Cr Income and expenditure With the amount received Transferring to income and expenditure For general purposes Dr Bank Cr Accumulated fund For specific purposes Dr Bank Cr special fund(e.g. training fund, Building fund)

Donations to other charities • For general purposes • Dr Donation to XXX • Cr Bank • For special purposes • Dr Income and Expenditure • Cr Donation to XXX With the amount paid Transferring to I&E as an expense

Subscriptions • Annual Subscription • Life membership fund • Entrance fees/joining fees

Annual Subscriptions Receipt and Payments account for the year ended 31 Dec 1996 • Example 1 Receipts Subscriptions from members for 1995 110 1996 2472 1997 80 2662 Additional information: Subscription in arrears at 31 Dec 96 = $132 Subscription in advance at 1 Jan 96 =$60

Ans: Income and Expenditure account for the year ended 31 Dec 1996 Income $ Subscriptions (2472+60+132) 2664 Subscription= Cash received from members+Opening prepayment-opening accrued + closing accrued- closing prepaid

Receipt and Payments account for the year ended 31 Dec 1996 • Example 2 Receipts Subscriptions from members for 1995 100 1996 2472 1997 80 2562 • Additional information: • 1 Jan 1996 31 Dec 1996 • Subscription in arrear $110 $132 • Subscription in advance $60 $80 • 2. The club has a policy of writing off any subscription that • are outstanding for more than one year

Ans: Income and Expenditure account for the year ended 31 Dec 1996 Income $ $ Subscriptions (2472+60+132) 2664 Expenditure Subscription written off (110-100) 10

Example 3 The financial year end of the club is 31 December, but The subscriptions are payable in advance on 1 October each Year. The subscriptions received on 1 October 1995 were $8000 and 1 October 1996 were $ 12000, without any subscription in arrears.

Ans: Income and Expenditure account for the year ended 31 Dec 1996 Income $ Subscriptions from 1 Jan-30Sept96 ($8000*9/12) 6000 from 1 Oct-31 Dec96 ($12000*3/12) 3000 9000 Back

Life membership fund • Life membership fees are income earned over a long period, and therefore, they should not be treated as income in one year. • Usually a life membership fund would be set up, part of it would be written off in each year as income.

Several points be noted • A life membership fund can be written off over: • The number of years of annual subscriptions purchased • The estimated average life of life members

From 1 January 1995, the club began to recruit life members. • On joining the club each life member has to pay a life • membership fee of $4000. • As at 31 December 1995, 20 people had been admitted as • life members. • In 1996, 5 people joined the club as life members • The life membership fee is to be recognized as income evenly • over 10 years. • Example 4

Ans: Life membership fund 1995 $ 1995 $ Dec 31 I&E (80000*1/10) 8000 Dec 31 cash (20*$4000) 80000 Dec 31 Bal c/d 72000 80000 80000 Income and Expenditure account for the year ended 31 Dec 1995 $ Income 8000 Subscriptions Balance Sheet (Extract) 1995 $ Life membership subscription 72000

Ans: Life membership fund 1995 $ 1995 $ Dec 31 I&E (80000*1/10) 8000 Dec 31 cash (20*$4000) 80000 Dec 31 Bal c/d 72000 80000 80000 1996 $ 1996 $ Jan 1 Bal b/d 72000 Dec 31 I&E (20000*1/10)+ (80000*1/10) 10000 Dec 31 Cash (5*4000) 20000 Dec 31 Bal c/d 82000 92000 92000

Income and Expenditure account for the year ended 31 Dec 1995 $ 1996 $ Income 8000 10000 Subscriptions Balance Sheet (Extract) 1995 $ 1996 $ Life membership subscription 72000 82000

Life membership fund can be transferred directly to the accumulated fund when an individual life member dies

The life membership fund was $8000 as at 1 January1996. • In 1996, two people joined the club as life members. • During the year 1996, three life members died. • It is the club’s policy to transfer the life membership fund of • $400 each directly to the accumulated fund when life members • die. • Example 5

Ans: Life membership fund 1996 $ 1996 $ Jan 1 Bal b/d 8000 Dec 31 Accumulated fund (3*$400) 1200 Dec 31 Cash (2*400) 800 Dec 31 Bal c/d (19*$400) 7600 8800 8800 Back

Entrance fees/joining fees • Entrance /joining fees can be included as income in the year that they are received, or written off over the number of years determined by the clubs

The balance of the entrance fees as at 31 December 1995 was • made up of: • Year of joining Balance • 1993 $1000 • 1994 $1500 • 1995 $3000 • On joining the club, each new member has to pay an entrance • fee of $500 • The entrance fee is to be recognized as income evenly over four • years • During the year of 1996, 10 new members had been admitted • Example 6

Income and Expenditure account for the year ended 31 Dec 1996 $ Income Entrance Fees (1000+1500*1/2+3000*1/3+500*10*1/4) 4000 Balance Sheet (Extract) $ Accumulated fund X Add surplus of I&E X X Entrance fees (1500*1/2+3000*2/3+500*10*3/4) 6500