Download

1 / 38

380 likes | 510 Views

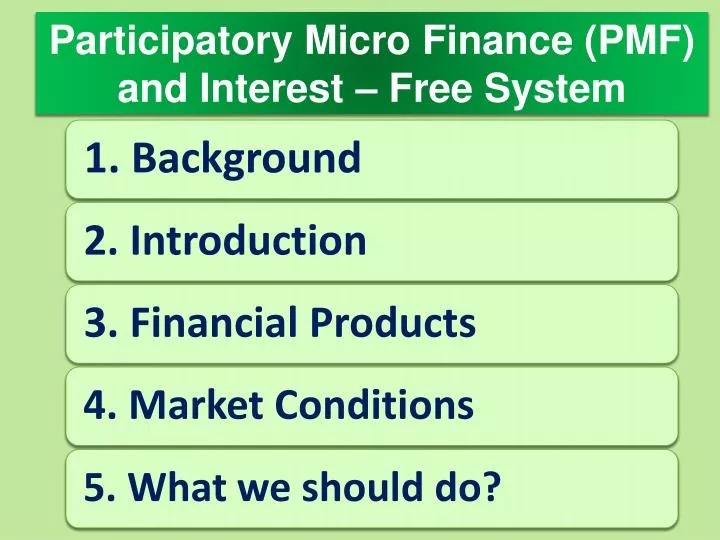

Participatory Micro Finance (PMF) and Interest – Free System. 1. Background. 1.1 Finance for Economic Growth. No person, enterprise, community or economy can attain desired economic growth if not allowed to access affordable source of finance.

E N D

Participatory Micro Finance (PMF) and Interest – Free System

1.1 Finance for Economic Growth • No person, enterprise, community or economy can attain desired economic growth if not allowed to access affordable source of finance. • Like the corporate sector, the household workers, farmers and micro and small enterprises in the unorganized sector also need equity funds (without fixed cost of finance) to attain target of economic growth without tension of interest. • There is certainly a need to develop source of interest free financial system for poor farmers, workers, enterprises and communities as well.

1.2 Unjust Credit Disbursement • Borrowers (with credit under Rs. 2 Lakhs) though shares 87.05% of loan accounts, have just 12.29% share in outstanding credit extended by SCBs; whereas the richer borrowers (with credit over Rs. 1 crore) share 0.17% of loan accounts share 61.93% of total outstanding credits. • Rich borrowers (with credit over Rs. 1 crore) sharing 75% loans with annual rate of interest below 10%, whereas poor borrower’s (with credit between Rs. 2 to 5 Lakh) share less than 9%. The same rich borrowers have 27% share compared to 60% by poor borrowers when the rate of interest exceeds 20%.

1.3 Micro Finance in India • Since Majority of Indian being poor and financially excluded from the mainstream financial segment, to let them access finances through formal sources, the Government of India introduced Micro Finance system in India. • The financial supports by Government agencies help development of Micro Finance Institutions. They grew their businesses through interest based lending from Public institutions or Banks. • Micro Finance sector in India is suffering due to lack of equity funds and high interest cost on lending money routed through Banks.

1.4 Financial Exclusion of poor • NSSO data reveal that 45.9 million farmer households in the country (51.4%), out of a total of 89.3 million do not access credit, either from institutional or non-institutional sources. • Indian Council for Research on International Economic Relations suggets that only 12 per cent of unorganized retailers have access to institutional credit and 37 per cent felt the need for better access to commercial bank credit. • Sachar Committee Report reveals that only 10% Muslims access formal banking services.

1.5 Need of financial inclusion • So far to improve financial inclusion, the demand side efforts including improving human and physical resource endowments, enhancing productivity, mitigating risk and strengthening market linkages been undertaken up. • RaghuramRajan Committee has suggested that measures be taken to permit the delivery of interest-free finance on a larger scale, including through the banking system. This is in consonance with the objectives of inclusion and growth through innovation.

2.1 Definition of Participatory Micro Finance (PMF) • Participatory Micro Finance (PMF) is a process wherein the Financier with small amount of finance (instead of lending money on interest) participates in anyone’s business activities either through bearing the capital risks of that business or by buying and selling tangible goods or assets required for that business. • Since Participatory Micro Finance adheres to the principles of Islam, it may be used as alternative to Islamic Micro finance in countries like India, Turkey, Japan, Nepal and China etc.

2.2 Fundamentals of Participatory Micro Finance • Fundamentals of Participatory Micro Finance are drawn up from Islamic Economics based on teachings of the Holy Quran, practices referred in the Hadiths and Islamic Jurisprudence etc. • Riba (Interest of any magnitude) is strictly prohibited in Participatory Micro Finance • Financing activities involving like alcohol, pork, gambling, non tangible assets, interest bearing financial products, porn, uncertain business risk, short selling etc. are not allowed. • It promotes sharing of business risks.

2.3 Practical Applicability of PMF • Applicability of Participatory Micro Finance are tested and recognized as ultra modern financial products in over 70 countries. • Considering high growth rate in Islamic Finance, even the secular countries are opening gateway for Islamic Micro Finance. • Participatory Financial Products like Musharaka, Mudaraba, Murahabha, Ijara, Bai Salam, Takaful and Sukuk are helpful in reducing debt burdens, fiscal deficit and inflationary pressure. • It helps combating inflation and recession.

2.4 How different from other Finances? • Charging interest on lending money is normal business in conventional finance which is not permissible under Participatory Micro Finance. • Conventional finance does not allow bearing business risk of any enterprise, whereas Participatory Micro Finance encourages doing so. • Buy and sell of goods and assets is normal practice under Participatory Micro Finance, which is hardly found in conventional model. • Participatory Micro Finance negates currency capital where conventional finance accepts it.

2.5 Advantages of PMF over others • It helps for financial inclusion of Muslims. • PMF assures 100% utilization of funds for livelihood program and also helps accelerating income generation process. • Backs the finances through goods/asset. • It helps countering economic problems like high inflation, fiscal deficit and economic recession. • It protects banks and financial institutions from financial crisis due to imbalances in the assets and liabilities accounts.

3.1 Musharaka (Equity Finance) • Equity Finance (Musharaka) is a mechanism wherein group of persons pull their equities (capital resource) for any business with condition to shares the profit / loss at mutually consented ratios among the subscribers. • This products is used to raise equities for venture capitals, facilitating cooperatives for farming, processing industry and exports etc. Mutual Funds could well support Micro Small and Medium Enterprises (MSMEs) allowing them to compete with the Corporate Sector.

3.2 Mudarabah (Trust Finance) • Trust Finance is a mode of finance wherein the Financier keeping faiths on any person / party extends funds allowing the party to manage that fund for execution of any business activity with a condition that all financial risks shall be on financier; but profit shall be shared on mutually agreed ratios among both parties. • Mudaraba is useful to promote entrepreneurship among such poor persons who holds required knowledge and skills for business but lacks finance to conduct sought business.

3.3 Murabaha (Cost – Plus Finance) • Cost Plus Finance (Murabaha) is a mechanism where financier instead of lending money to the client consider him as a customer; buys required goods for him; adds a mark up profit (in consent of the buyer) over the actual costs and sells to the client with deferring the receipt of payments for a specific period of time. • Since one Murabaha leads to at least two trades, it allows the economy gain more growth in trade activities compared to registered growth in the financial sector.

3.4 Ijara (Lease Finance) • Lease Finance (Ijara) is a mechanism where the financier buys any tangible asset or equipment and lends that to the customer (on rent basis) for a specific period of time (with provision to either return back after use or own that after paying the title / ownership fees). • Ijara enables the poor to acquire high value assets, premises, vehicles, tools and machineries etc. to use valuable assets by paying regular monthly rents in installments (instead of interest on loan) to purchase that assets . It is very popular financial product to purchases premises, machines and vehicles etc.

3.5 Istisna (Progressive Finance) • Istisna (Progressive Finance) is a process where payments are made in stages to facilitate step wise progress of the processing/construction work. • Istisna enables the construction company get finance to construct slaps / sections of a building by availing finances in installments for each slap. • Istisna also helps manufacturers as it could be used to finance manufacturing / processing cost for any goods in stages. • Istisna helps use limited funds to develop higher value goods/assets in stages.

3.6 Bai Salam (Forward Sale) • Under Forward Sale (Bai Salam) the buyers and sellers negotiate price of a commodity which is not present, but supplier assures to provide that after a period of time; the buyer makes the payment in advance for set quantity of those goods to be delivered by the supplier later on set date. • Bai Salam enables traders and exporters procure agro products at pre determined price; stabilizes product’s prices. It also empowers the farmers by interest free finance during time of sowing along with assured good sale price for their produces.

3.7 Qard E Hasna (Benevolent Loan) • Qard E Hasna (Benevolent Loan) is the only scheme under PRTF where the customer can get credit in cash to meet financial needs for even non economic activities like socio-cultural, educational, medical or marital purposes. • Under Qard E Hasna, the financer lends money to the borrower without interest. • Under Qard E Hasna only actual cost of operation along with principal amount is allowed to recover from the beneficiary.

3.8 Interest free Deposits Deposit Schemes • Al Wadia (Current Deposits) - accounts where deposits are secured but not considered for interest or profit sharing. • Musharaka / Murabaha Deposits - are used to mobilize funds for Investment purposes and allows the depositors to earn profit / loss on businesses financed. • Mutual Funds are used to raise finances for investment in different projects. • Sukuk is used to raise funds needed for infrastructural developments.

3.9 Takaful (Islamic Insurance) • Takaful is Shariah compliant insurance system where pool of members mutually subscribes premiums to compensate the losses if recorded in the businesses run by the members of that group. • The members agrees to invest the fund collected by way of subscribing the premium amount with condition to share the profit / loss realized through investing the funds in legal and ethical businesses. • Insurance company manages the funds and assures insurance subscribers to compensate business losses if any.

4.1 Demand forces yet to envisage • Since Participatory Micro Finance is not offered by any big bank / financial institution in India; and people are mostly unaware about it, we have yet to envisage demand forces for PMF. • Small and a few financial institutions with limited resources and under constraint conditions offering PMF at local levels, which are not known to all people, so demand forces are yet to envisage. • No genuine envision for demand forces of Participatory Micro Finance is done by any reputed financial institution / research institute.

4.2 Regulatory hurdles for PMF • The Reserve Bank of India (RBI) as Regulator of Banks and MFIs in India has yet to consider provisioning grounds for Participatory Finance. • Banks and MFIs registered with RBI are not allowed to raise equity funds / funds with provision to invest in business. • RBI not encourages banks / MFIs to buy and sell goods and assets. • Takaful and Sukuk are so far not allowed by respective Indian regulators. • Double stamp duty on Ijara transactions adds cost of assets thus hurdles Ijara growth.

4.3 Infrastructural deficit for PMF • Since demand forces for PMF is not envisaged so far, there is no significant effort to create required infrastructure for Participatory Micro Finance. • No source for equity funds is available to meet requirement of MFIs to promote PMF in India. • No institutional network to promote cooperation and coordination among institutions dealing in Participatory Micro Finance in India. • There is no institutional effort to promote inter banks / MFIs transactions to promote liquidity for Participatory Micro Finance businesses in India.

4.4 Taxation Problems for PMF • Like Ijara, there is also taxation problems for other PRTF products like Murabaha, Bai Salam and Istisna etc. where bank or MFI need to buy and sell commodities sought for sale. • The taxes imposed on commodities bought by Bank or MFI for sale through Murabaha, Ijara or Bai Salam increases the net cost of commodities, thus make it challenging to compete with other sellers in the open market because majority of sellers in the unorganized market avoids collecting and paying taxes on their sale.

4.5 Shortage of Equity Funds • No Bank or MFI in India are allowed to raise equity funds which is basic source for PMF, so banks and MFIs find it difficult to start PMF. • In absence of Equity Funds, banks / MFIs cannot afford to finance businesses on principles of Participatory Finance. • There is no provision to create mutual funds by Banks / MFIs for their specific needs. • There is no regulator to raise funds for Takaful (Islamic Finance) which may have otherwise boosted Participatory Micro Finance in India.

4.6 Accounting and IT software • There is no ready to use accounting package for Participatory Micro Finance which hurdles even the experiment of PMF products. • There is no ready to use IT software suitably meeting the requirements of PMF business. • In absence of suitable Accounting and IT software banks / MFIs cannot even think to start piloting Participatory Micro Finance business. • There is also no institution to lead development of required Accounting software and information technology required for PMF.

4.7 Education & Training of staff • There is not enough institutional effort to provide education and training on PMF; only a few institution has recently started course on Islamic Banking and Finance however they have still to arrange proper training and apprentice programs. • Little job opportunities in Participatory Micro Finance is also a big challenge for those institutions who are providing education on PMF. • Qualified and expert teacher and trainers are also not available in Indian market to provide education and training on PMF.

5.1 Create Public Awareness Public awareness could be created through - • Arranging awareness campaigns • Publishing articles and analytical reports • Distributing handbills and pamphlets • Arranging seminars and workshops • Holding Interactive discussion sessions • Inviting suggestions and public feedbacks • TV serials advocating interest free system • Educational and training sessions

5.2 Establish Business Groups • Most significant means to promote Participatory Micro Finance in India could be creating a network of Business Associations / groups. • Businessmen, farmers and artisans seeking Participatory Finance should form groups at local levels according to convenience of interaction • Members of Business Groups should so interact that they could understand each others financial need and economic prospects. • Business Group should be eager to share financial resources and economic expertise.

5.3 Create Funds for PMF • Since there is no existing source of Participatory Finance, members associated with business groups formed to promote Participatory Finance need to create funds through mutual deposits / subscription of participatory (equity funds) • Such deposits and participatory (equity funds) could be used to promote participatory finance among the members of business group in urban areas and farmers and non farm workers in rural areas through mode of Musharaka, Mudaraba, Murabaha, Ijara, istisna, Bai Salam and Takaful etc. to allow mutual help the members.

5.4 Create Takaful Fund • Members of the business groups, farmers and artisans associations could well establish a Takaful fund (mutual insurance fund) to subscribe risks associated to business of members. • Takaful funds would work as hedge to protect the members of the group by compensating the business losses if occurred for any member. • Small takful funds at local leveles may further be linked to large scale Takful funds at regional, national and international levels to ensure reinsurance of the Takaful Funds.

5.5 Develop Interest Free System • Participatory Finance will not only help India attain goal of financial inclusion and foster economic growth but also allow India counter side effects of interest like fiscal deficit, financial loss due to interest payment on debt by Government and extending subsidies on interest. It will help India develop Interest free system to stabilize price levels, protect money value and exceed economic growth with social justice. • Are We ready to develop Interest free system?