Download

1 / 8

80 likes | 110 Views

Explore the treatment of non-performing loans (NPLs) and the market impact of auctioning associated collaterals through foreclosure processes in Greece. Analyze the trends, challenges, and potential for real estate assets flooding the market. Understand the perspectives of banks, real estate owners, investors, and valuers in this evolving landscape.

E N D

The treatment of the NPLs and the market effect of the associated collaterals once auctioned through foreclosure procedures Dr Aris Karytinos, CEO, NBG PANGAEA REIC 19.10.2018

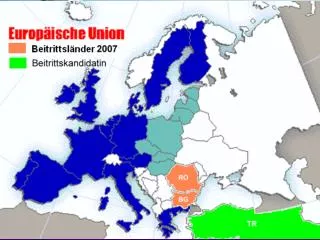

Non-performing loans in the European Union Source: EBA Risk Dashboard

NPLs ratio evolution (2016 – 2018): Greece vs EU Source: BoG, EBA Risk Dashboard

Breakdown and evolution of the NPLs in Greece Source: BoG

How real estate collaterals find their way into the market • Banks proceed with foreclosure of specific real estate collaterals; in this case assets are either absorbed by the market or the banks acquire the assets themselves with a view to minimizing losses and disposing of the assets at a later stage, when market has recovered and a better price can be achieved (so far statistics show that banks acquire 80% of the assets through foreclosure process) • Banks sell packaged groups of NPLs (e.g. Piraeus Bank’s Amoeba; Alpha Bank’s Jupiter etc.); the acquirer of such NPLs undertakes the foreclosure process • Banks reach an agreement with the owner for the disposal of the asset before it has been repossessed; in this way significant legal delays are avoided and in some cases better pricing can be achieved allowing some benefit for the owner as well

Should we expect real estate assets to flood the market? • Annual foreclosures prior to the crisis: ca 55,000 | 2017 foreclosures: ca 5,000 • Foreclosures are very time consuming from a legal perspective • The servicing of NPL portfolios in order to “sanitize” the assets and mature the properties with a view to being sold requires the existence of well organized platforms that are currently being established in the Greek market • A number of legal and technical issues regarding the properties need to be addressed before the properties can be sold • A small percentage of properties are characterised by strong real estate fundamentals • Banks are likely to acquire the assets themselves at a first stage and gradually release them into the market, anticipating an improvement of the economy and increase in prices • The pace of the release of real estate collaterals into the market is correlated with the overall performance of the Greek macros which affect both the users market and the investors market A rationalised release (in terms of both size and pace) of real estate collaterals into the market is the most likely scenario

What happens with residential real estate in particular? • In contrast with investment grade commercial real estate market, the residential market is lagging in signs of recovery as a result of low disposable income (lower earnings and increased taxation) and limited financing (mortgage lending has dropped to 10% of the pre-crisis levels) • New construction of residential properties is still extremely low (€1bn in 2017 vs €25.2bn in 2007) • Properties that can be used for short term leases (e.g. Airbnb) and / or secure Golden Visa are the exception to the rule and the main force driving investment in residential construction through conversion and refurbishment of existing properties Release of residential real estate collaterals should also be rationalised in order for the market to be able to absorb it

The investor’s point of view Given that currently investment product is scarce and the number of investors is increasing, the stock to be released through the management of NPL collaterals will help the market, assuming that the macro fundamentals improve is such a way that there will be sufficient demand by the end users The valuer’s point of view Still a limited amount of transactions, mostly relating to packaged NPLs and not specific real estate sales turning valuations into a very challenging exercise An interesting time to be a valuer in Greece