Download

1 / 23

300 likes | 728 Views

Value Chain Analysis. A Changed Perspective. Results of Operations vs. operating information for results. Michael Porter’s Value-Chain. Developed in 1985 by Michael E. Porter in Competitive Advantage Highlights cost advantages and distinctive capabilities --the value processes

E N D

A Changed Perspective • Results of Operations vs. operating information for results

Michael Porter’s Value-Chain • Developed in 1985 by Michael E. Porter in Competitive Advantage • Highlights cost advantages and distinctive capabilities--the value processes • But note that there is no one template.

Value Chain Analysis • Multiple Approaches • Porter’s approach…see next slide • MAG 41 approach • Ansari’s approach

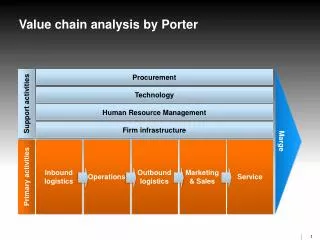

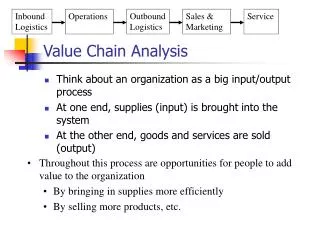

Value Chain Modelfrom Michael E. Porter’s Competitive Advantage SUPPORT ACTIVITIES Firm Infrastructure (General Management) Human Resource Management Customer Value Margin Technology Development Procurement Inbound Logistics Outbound Logistics Sales & Marketing Service and Support Ops. Margin Customer Value PRIMARY ACTIVITIES

Customer Value Added Margin Orientation Primary Activities Inbound Logistics Operations Outbound Logistics Sales and Marketing Service and Support Support Activities Firm Infrastructure Human Resources Tech. Development Procurement Value Chain Elements

Goal of Value Chain • Driven by customer perceptions • Increase margins • Focus on value processes • Distinctive capabilities • Cost advantages • Some examples • Southwest Airlines • Intel Corporation

Porter Focus • Value processes • Cost advantage • Core competencies

Value Chain and the QCT Triangle • VC allows alignment of processes with customers. This generates a quality advantage. • VC focuses cost management efforts. • VC provides for efficient processes which improves the timeliness of operations.

Value Chain and the TBC Triangle • Technical: • Increases knowledge of no profit zones • Increases knowledge of forward and/or backward integration opportunities • Identifies value processes • Identifies win-win alliance opportunities • Behavioral: • Focus shifts to “the customer” • Focus shifts from conflict to partnering with customers & suppliers • Cultural • Creates externally focused mindset • Generates information sharing environment with respect for confidentiality

Using the Value Chain • Helps you to stay out of the “No Profit Zone” • Presents opportunities for integration • Aligns spending with value processes • Provides for reconfiguration of the value chain • outsourcing • off-shoring • co-location with customers or suppliers • redesign for efficiency • Involves chain partners: customers & suppliers

Value Chain Analysis • Document the activities • Understand the cost and margins at each step. • Use Activity Based Costing • Map the value chain to the industry value chain • Look for core competencies • Map the cost structure • Note that external values drive cost advantages

Performance Based Measurement • Measures the essential • Performance measurement elements • Performance measurement reporting

Performance Based Measurement Elements • Define Strategies • Identify Critical Success Factors (CSF’s) • Create Measures • Establish Standards through Benchmarking • Collect Data • Evaluate and Revise • Reward

Critical Success Factors • Required for Strategic Objective Attainment • Select one CSF for each objective • Selection process can be difficult • Some CSF Examples

CSF Measurement Alternatives • Non-financial Measures • Operational Focus • Consider the Ease of Data Collection

Monitoring and Adjustment • Remember the ease of collection • Use meaningful measures • Monitor at least weekly…even daily • Make real-time adjustments • Invite participation in the solution process

Reward System Integration • Include CSF attainment in the reward system • Avoid sub-optimizing rewards

Implementation Keys • Begin with the Finance Department • Follow the management of change process • Use what data is available • Be prepared for resistance • Automation is NOT required • Create opportunities for celebration • Publicize on-going success

Strategic Positioning Analysis(concerned with role of Cost Management in the firm) • Firms choose to compete either through cost leadership or product differentiation • Strategy chosen influences cost management perspective

Cost Drivers There are two main types of cost driver: • A resource driver, which refers to the contribution of the quantity of resources used to the cost of an activity. • An activity driver, which refers to the costs incurred by the activities required to complete a particular task or project.

Linkages Among Value Chain Analysis, Strategic Positioning Analysis and Cost Driver Analysis • Understanding the value chain helps define the optimal positioning strategy • Understanding the value chain and positioning strategy helps identify the relevant cost drivers