Download

1 / 12

120 likes | 219 Views

Perspectives on Renewable Portfolio Standard Authority. NARUC Summer 2007 July 17, 2007 Richard Sedano. Introduction. Regulatory Assistance Project

E N D

Perspectives on Renewable Portfolio Standard Authority NARUC Summer 2007 July 17, 2007 Richard Sedano Website: http://www.raponline.org

Introduction Regulatory Assistance Project RAP is a non-profit organization, formed in 1992, that provides workshops and education assistance to state government officials on electric utility regulation. RAP is funded by the Energy Foundation, US EPA & US DOE. Richard Sedano was Commissioner of the Vermont Department of Public Service, 1991-2001

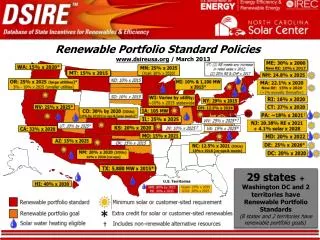

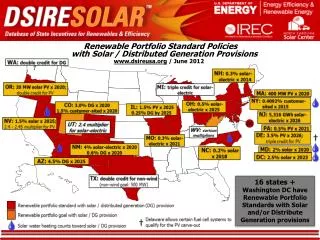

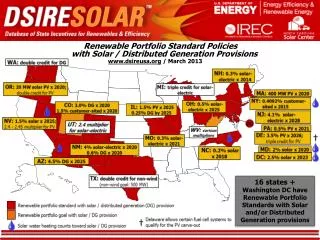

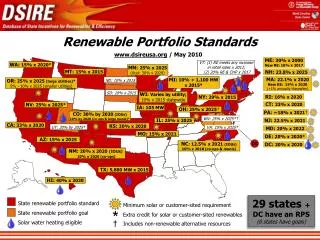

DSIRE: www.dsireusa.org June 2007 Renewables PortfolioStandards ME: 30% by 2000 10% by 2017 goal - new RE MN: 25% by 2025 (Xcel: 30% by 2020) VT: RE meets load growth by 2012 *WA: 15% by 2020 • NH: 23.8% in 2025 WI: requirement varies by utility; 10% by 2015 goal MT: 15% by 2015 MA: 4% by 2009 + 1% annual increase OR: 25% by 2025 (large utilities) 5% - 10% by 2025 for smaller utilities RI: 15% by 2020 CT: 23% by 2020 • NV: 20% by 2015 IA: 105 MW • NY: 24% by 2013 • CO: 20% by 2020 (IOUs) *10% by 2020 (co-ops & large munis) IL: 8% by 2013 • NJ: 22.5% by 2021 CA: 20% by 2010 • PA: 18%¹ by 2020 MO: 11% by 2020 • MD: 9.5% in 2022 *NM: 20% by 2020 (IOUs) 10% by 2020 (co-ops) • AZ: 15% by 2025 *DE: 10% by 2019 • DC: 11% by 2022 *VA: 12% by 2022 TX: 5,880 MW by 2015 HI: 20% by 2020 State RPS State Goal • Minimum solar or customer-sited RE requirement * Increased credit for solar or customer-sited RE • ¹PA: 8% Tier I / 10% Tier II (includes non-renewables); SWH is a Tier II resource Solar water heating (SWH) eligible

Some RPS Purposes • Public, structured commitment to selected resources that gets results • Impresses the public • Impresses qualifying resource development teams and inspires their confidence • Takes guess work out of public value of renewables (avoids other sources) for monopoly service and is competitively neutral • Can be part of a coherent clean energy strategy • Market solution (not like PURPA QF contracts) • Targets may stretch out in time ahead of supply

(Should we be saying “Clean Energy Standard?”) • Choice of resources: mixed policy considerations (expansive as possible) • Truly renewable in nature • High efficiency DG sources • Tending to be locally available • Addressing other economic development or environmental or political issues • Energy efficiency, demand response

A National RPS • Extends purposes to all states applying uniformly to all customers (requirement, not a goal) • Applies to utilities of all ownership structures • Applies consistently to all states, including those without sufficient impetus to adopt a state standard • Would need national tracking system, which may be able to meld current regional systems (A REC is A REC is A REC, no double counting) • What about states that have adopted a standard – will the national standard accommodate or obliterate state standards?

It Depends • National RPS can be flexible, accommodating all categories of most states • Some administrative process that is relatively easy to manage will keep the categories fresh • States should be able to qualify what they want for their own standard • National RPS can establish a minimum standard of renewable energy and alternative compliance, states can exceed it

State Concerns • Preemption (on resource and cost recovery) • Fed RPS won’t shield states from cost concern • Absence of locally available renewables • Most states have some renewable sources, but as with current regional markets for electricity supply and demand of electricity, a market for RECs can and will form, and some areas will be buyers • Rates (compared with past or future?) • Consistency in definition (states already have tiers) and alternative compliance (sum, state CE funds)

Other Concern • Encouraging new renewable sources while crediting existing renewable ones • Underscores the “game” that a portfolio standard creates • Best “bang for buck” of ratepayer dollar focuses on new sources • Existing units use “fairness” argument to win a place in the system • State systems work this out (“tiers” seems best way), no national consistency

Other Concern • Deliverability – does power associated with the REC need to be deliverable within the market where the REC is sold? • National program would probably include no requirement for deliverability • Makes market much thicker – renewable rich areas can “mine” RECs for the whole country • May strain credulity of public, or not

Why Can’t We All Just Get Along? • Growing consensus on need for alternative, clean generating sources >> imperative? • Question of whether lack of state actions is OK -- does there needs to be a base? • Federalism vs. Commitment • Federal RPS perspective: Measure benefit to climate compared with other solutions

The Regulatory Assistance Project • RAP Mission: RAP is committed to fostering regulatory policies for the electric industry that encourage economic efficiency, protect environmental quality, assure system reliability, and allocate system benefits fairly to all customers.