Download

1 / 23

230 likes | 320 Views

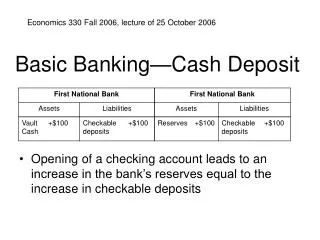

Commercial Law: Deposit Accounts and Cash Proceeds. Deposit Accounts. Two ways to perfect in money in a bank account: Perfection by CONTROL directly against the bank account as original collateral. [9-314]

E N D

Deposit Accounts Two ways to perfect in money in a bank account: • Perfection by CONTROL directly against the bank account as original collateral. [9-314] • Perfection in OTHER COLLATERAL that is then sold for PROCEEDS deposited in the account. [9-315]

Perfection by Control of Deposit Accounts • Perfection by Control Accomplished in three ways: • BE the depository bank. [9-104(a)(1)]; • AGREE with the three parties (SP, Debtor, and Dep. Bank) that the bank will let SP control the account. [9-104(a)(2)]; • BECOME the account owner (SP becomes the bank’s customer. [9-104(a)(3)]

Priorities in Deposit Accounts • Perfection by Control > Perfection by other means (proceeds); [9-327(1)] • Control by Bank > Control by agreement and Proceeds. [9-327(3)] • Control by Ownership or subordination agreement > Control by Bank. [9-327 (4) and 9-339]

Advanced Priority in Deposit Accounts • Control > Control in order of TIME. [9-327(2)] • Proceeds > Proceeds in order of priorities in original security interest.

Moving Money in Deposit Accounts • What to do about money that LEAVES the bank account (can you go get it back?) • What to do about money that STAYS and is COMMINGLED in the bank account (whose money is whose?)

Part I: Transfers Out of Bank Accounts • Money (proceeds OR original collateral) that is transferred to someone else out of a bank account is free and clear once it is transferred. [9-332] • Example: I sell inventory, deposit proceeds in a bank account. I then write a check on the bank account to pay for groceries. The grocery store is free and clear. • Collusion standard: If the transferee COLLUDES with the debtor to transfer the money, the court can undo the payment. [9-332(a), (b)]

Part II: Commingling and Tracing What about money that stays in the bank account? • The problem: money that is proceeds of sales of collateral gets mixed with non-proceeds money in the same account. • USUAL case: merchant mixes proceeds from sales of inventory in with everything else in his general operating account.

Commingling (con’t) • Commingling isn’t a problem if the SP has a DIRECT interest, secured by control, in the bank account. Then, all the money that comes into that account is collateral. • Commingling IS a problem for proceeds of sales of collateral.

Tracing • Most common tracing rule is Lowest Intermediate Balance. (non-Code law). [9-315(b)(2)] • This is a rule of logic: if the account balance drops below the amount of proceeds deposited, then that amount of proceeds logically MUST have been dissipated.

Practical LIB • Step 1: When account balance dips below proceeds amount, that is the new LIB; • Step 2: Add all new deposits of proceeds that come after the LIB above (i.e., LIB + new proceeds deposits is your new total); • Step 3: If the account balance dips again below the new total in Step 2, that’s the new LIB. Go back to step 1.

So What do Sophisticated Parties Do? • Perfect in pledgeable collateral (chattel paper, notes) by possession, to prevent sales to third parties; • Create lock-box accounts that limit the debtor’s ability to commingle and transfer proceeds.