Download

1 / 31

400 likes | 1.04k Views

Chapter 5: Production and Cost. Brickley, Smith, and Zimmerman, Managerial Economics and Organizational Architecture , 4th ed. Production and cost objectives. Students should be able to Write a production function and distinguish between returns to scale and returns to a factor

E N D

Chapter 5: Production and Cost Brickley, Smith, and Zimmerman, Managerial Economics and Organizational Architecture, 4th ed.

Production and costobjectives Students should be able to • Write a production function and distinguish between returns to scale and returns to a factor • Use isocosts and isoquants to illustrate production trade-offs • Employ short- and long-run cost curves to describe firm characteristics

Production functions A production function specifies maximum output from given inputs:

Empirical production functions • Cubic Q=a0+a1XY+a2X2Y+a3XY2+a4X3Y+a5XY3 • Cobb-Douglas Q = aXbYc log Q = log a + b log X + c log Y

Returns to scale Defined: The relation between output and a proportional variation of all inputs together Increasing returns to scale:Q=KL Decreasing returns to scale:Q=K1/3L1/3 Constant returns to scale:Q=K1/2L1/2

Returns to a factor Returns to a factor refer to the relation between output and variation in only one input • Total product • Average productQ/L • Marginal productQ/L

Returns to a factor Production function: Q=S1/2A1/2

Illustrating production choices with isoquants • Isoquants portray technical combination of inputs to produce a given level of output • Shape of isoquants indicates substitutability between inputs

Isocost lines • Isocosts portray combinations of inputs that entail the same cost • Isocosts change as input prices change

Optimal input mix Where MPi is the marginal product of input i and Piis the price of input i.

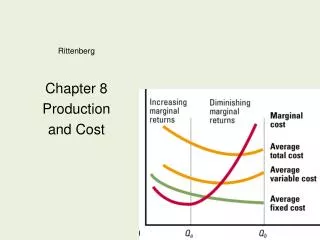

Cost concepts • Total cost • relation between total cost and output • Marginal cost • change in total cost when output rises one unit • Average cost • total cost divided by total output • Opportunity cost • value of best alternative resource use

Short run versus long run • Short run • at least one input is fixed • cost curves are operating curves • Long run • all inputs are variable • cost curves are planning curves • Fixed costs--incurred even if firm produces nothing • Variable costs--change with the level of output

Long-run average costenvelope of short-run average cost curves

Additional cost concepts • Minimum efficient scale • plant size at which long-run average cost first reaches its minimum point (Q*) • Economies of scope • cost of producing a joint set of products is less than cost of producing separately in separate firms • Learning curves • costs decline with production experience

Profit maximization • A firm should increase output as long as marginal revenue exceeds marginal cost • A firm should not increase output if marginal cost exceeds marginal revenue • At the profit-maximizing level of output, MR=MC

Factor demand Efficient production requires that MPi/Pi= MPj/Pj The reciprocals represent marginal cost Pi/MPi=Pj/MPj=MC At the optimum output level Pi/MPi=MR From which we derive the demand curve for input i Pi=MRMPi

Cost estimation • Effective management decisions should incorporate estimates of short- and long-run costs • Use regression analysis • Short-run costs may be approximately linear VC = a + bQ