Download

1 / 24

240 likes | 267 Views

Explore production, cost, and revenue concepts to maximize profit in business. Learn economic vs. accounting costs, production functions, cost concepts, and market forms. Discover rules for maximizing profit in perfect competition and monopoly scenarios.

E N D

Chapter Outline • Production • Costs • Revenue • Maximizing Profit

Basic Definitions • Profit: The money that business makes: Revenue minus Cost • Cost: the expense that must be incurred in order to produce goods for sale • Revenue: themoney that comes into the firm from the sale of their goods

Economic vs. Accounting Cost • Economic Cost: All costs, both those that must be paid as well as those incurred in the form of forgone opportunities, of a business • Accounting Cost: Only those costs that must be explicitly paid by the owner of a business

Production • Production Function: a graph which showshow many resources we need to produce various amounts of output • Cost Function: a graph which shows how much various amounts of production cost

Inputs to Production • Fixed Inputs: resources that you cannot change • Variable Inputs: resources that can be easily changed

Concepts in Production • Division of Labor: workers divide up the tasks in such a way that each can build up a momentum and not have to switch jobs • Diminishing Returns: the notion that there exists a point where the addition of resources increases production but does so at a decreasing rate

Output D Production Function C B A Workers Figure 1 The Production Function

Costs • Fixed Costs: costs of production that we cannot change • Variable Costs: costs of production that we can change

Total Cost Total Cost Function D C B A Output Figure 2 The Total Cost Function

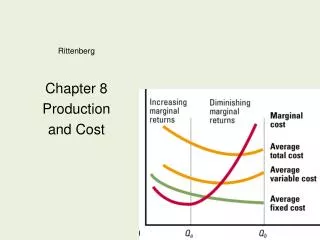

Cost Concepts • Marginal Cost: the addition to cost associated with one additional unit of output • Average Total Cost: Total Cost/Output, the cost per unit of production • Average Variable Cost: Total Variable Cost/Output, the average variable cost per unit of production • Average Fixed Cost: Total Fixed Cost/Output, the average fixed cost per unit of production

P MC ATC AVC AFC Q Figure 3 Marginal Cost, Average Total, Average Variable, and Average Fixed Cost

Numerical Example * MC is per 100

Revenue • Marginal Revenue:additional revenue the firm receives from the sale of each unit

P P S P* P*=Marginal Revenue D Market for Memory Our Firm Figure 4 Setting the Price When There are Many Competitors

P MR D Market for Memory Figure 5 Marginal Revenue When there are No Competitors

Numerical Example For the Many Competitors Case * MR is per 100

Maximizing Profit • We assume that firms wish to maximize profits

Market Forms • Perfect Competition: a situation in a market where there are many firms producing the same good • Monopoly: a situation in a market where there is only one firm producing the good

Rules of Production • A firm should a) produce an amount such that Marginal Revenue equals Marginal Cost (MR=MC), unless b) the price is less than the average variable cost (P<AVC).

Numerical Example of Profit Maximization With Many Competitors

Numerical Example of Profit Maximization With No Competitors