Download

1 / 29

300 likes | 557 Views

Vicente J. Gonzaga Erl Malboeuf Team 6. Roth IRA vs. Traditional IRA. Overview. What are IRAs? Roth vs. Traditional The Scenario Analyses and Comparisons Conclusions. What are IRAs?. IRA = I nvestment R etirement A ccount

E N D

Vicente J. Gonzaga Erl Malboeuf Team 6 Roth IRA vs. Traditional IRA

Overview • What are IRAs? • Roth vs. Traditional • The Scenario • Analyses and Comparisons • Conclusions

What are IRAs? • IRA = Investment Retirement Account • Specialized savings accounts specifically geared for post-retirement funding • Tax features • Tax-deductible • Tax-deferred • Tax -free

Choices, Choices • So why are we up here? • IRAs come in two main flavors: • 1) Traditional • 2) Roth • Which one?

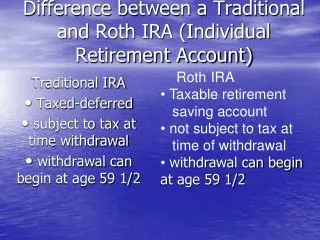

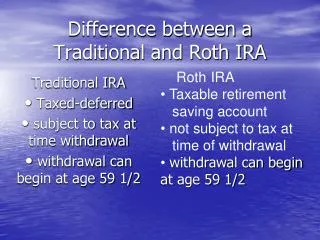

Roth vs. Traditional • Traditional IRA • Contributions are tax-deductible • $75,000 gross salary • Deposit 10% ($7,500) into a Traditional • ($75,000 -$7,500)=$67,500 (new gross income) • Cool beans, right?

Traditional IRA • Contributions are tax-deductible, but withdrawals are taxed based on the income bracket they fall under • Traditional IRAs • Tax-deductible contributions • Tax-deferred balance growth • Taxed withdrawals/distributions

Roth IRA • Roth IRA • Contributions are not tax deductible • $75,000 gross salary • $75,000 – [25%($75,000)]=$56,250 • THEN deposit 10% ($5,625) into the Roth IRA • $5,625<$7500 (from Traditional) • Ew… right?

Roth IRA • Contributions are made with after-tax dollars, but withdrawals are tax-free. • Roth IRA • Contributions based on after-tax dollars • Balance growth is tax-free • Withdrawals/distributions are tax-free

Roth and Traditional • Important fact to keep in mind: • Both Roth and Traditional IRAs impose contribution caps (equal for both) • Caps are adjusted for inflation every few years. • For simplicity, we treated cap adjustment as continuous • These caps greatly affect the dynamics of the savings plan given initial conditions.

The Pitch • You are Yoda (you can live for a very, very long time). • You have used the force to earn an engineering degree and have landed a position with $60,000 gross annual pay “Long, I live.”

Major Assumptions • Deposits will always be a fixed percentage of available income • “Excess” savings (explained later) will go into market investment • We later neglect “excess” • Assumeno pension • Tax brackets always apply where appropriate

Default Values • Starting Gross Salary: $60,000 • Expected Annual Raise=8% • Annual deposit rate: 10% • Applies to available income • Deposits between accounts are not equal • This is strictly followed • Post-retirement Lifestyle: $65,000 • Total years employed: 41

Default Values • Inflation: 3.5% • IRA Caps increase by inflation (=3.5%) • Interest earned on both IRAs: 5% • Market ROR: 9.00% • Retirement Assets ROR: 6.00%

The Reference Parameter? • Debt-free years after retirement! • How long under each account given equal conditions will you last after retirement?

Our Goal • UNPRECEDENTED , NEEDLESSLY METICULOUSL ACCURACY • (Flip to excel file and previous presentation on similar topic)

Assumptions Made (from a past class’ presentation) • Equal contributions to both plans • Roth IRA ineligibility ignored • Flat tax (not tiered) • Annual salary raises kept up with inflation at 3% • ROR is 10% • No 401K matching from employer • No Social Security Benefits • No investment fees • 35 working years

So Far… • It looks like Traditional IRA is the better choice- • But is this the whole story? • Remember that we’ve been including excess savings (that have been invested with an ROR of 9.00%) • Let us now neglect excess savings

The Tables have Turned! • So what just happened? • Excess Included => IRA wins • Excess neglected => Roth wins • Which one really wins? • The answer lies in the circumstances, and may change according to certain factors blahblahblah…

BASICALLY • It depends! • Traditional IRA “won” with excess • This implies that the Traditional IRA allows for more flexibility with extra savings! • Roth IRA “won” when excess was neglected • This implies that between the two, Roth IRA has the longest staying power based purely on account withdrawals!

The Bottom Line • The Roth IRA is the safer option for people who choose to invest extra savings minimally. If left to account balance alone, the Roth will outlast the Traditional. • People who tend to rely on earned interest and surefire, small investments should choose the Roth.

The Other Bottom Line • The Traditional IRA allows for creative use of large excess savings but does not have as much post-retirement staying poweras the Roth. It is therefore slightly riskier. • People who are more confident investors and are investment-savvy may benefit more from a Traditional IRA, or may find the Traditional more appealing.