Download

1 / 16

230 likes | 336 Views

Learn about Responsibility Centers, Efficiency vs. Effectiveness, Revenue, Expense, and Profit Centers, and Goal Congruence within Management Control Systems to achieve strategic business goals.

E N D

Responsibility Centers Chapters 3 & 4, Management Control Systems, 12th Ed., Anthony and Govindarajan

Strategy(From Previous Lecture) • Corporate Strategy • To maximize use of resources • Business Strategy • To compete in selected markets

Goals and Strategy(From Chapter 1) • Strategy Formulation • Goals • How to attain • Strategy Implementation (Execution) • Objectives • Management Control Systems

Where Are We Going??? • Develop a Strategy • Develop Goals (to support the strategy) • Develop Objectives (to achieve the goals) • Refine Organizational Structure (in support of the objectives) • Develop Evaluation Items (in support of achieving the objectives) • Assign Responsibility Centers (within the organizational structure)

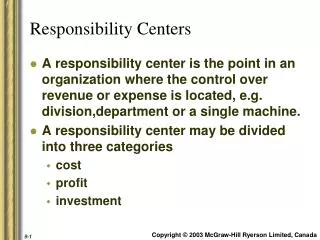

Responsibility Center • An organizational unit with a manager responsible for its activities • Usually refers to a unit within the organization • Exists to accomplish an objective

Inputs & Outputs • Optimum relationship between inputs and outputs • Within management control system, must be measurable • Unit measurements • Hours of labor, quantities of materials, etc. • Monetary measurements • Costs, revenues

Efficiency & Effectiveness • Not mutually exclusive • Two criteria used to judge responsibility centers • Efficiency: • Ratio of outputs to inputs • Higher is better! • Effectiveness: • Relationship of output to predetermined objectives • Again, higher is better!

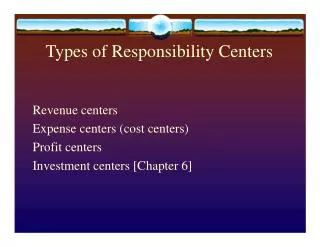

Types of Responsibility Centers • Revenue centers • Expense centers (cost centers) • Profit centers • Investment centers [Chapter 6]

Revenue Center • Output, and only output, is measured • Measurement is normally in monetary terms • Typically, sales/marketing • Cannot set price • Have no control over costs

Expense (Cost) Center • Inputs, and only inputs, are measured • Measurement is normally in monetary terms • Two types • Engineered expense centers • Optimal relationship between inputs and outputs • Discretionary expense centers • Optimal relationship cannot be established between inputs and outputs

Conflicts & Goal Congruence • Managers of revenue and expense centers • May seek excellence at high costs • Many $$$ for slight improvement in output • May seek output rather than quality • Increase of lesser quality products • Need special budgetary controls • Must consider goal congruence

Profit Center • Both inputs and outputs are measured • Measurement is in monetary terms • Inputs are related to outputs

Profit Center • Two conditions must be met to create a profit center • Relevant information must be available • Effectiveness of managers decisions must be measurable

Business Units • Full autonomy – normally not feasible • Goal congruence – risk of loss increases • Capital Budgeting – normally limited

Selection of Measurement Items • If manager can influence an item, it could/should be used as a measurement of performance • Total control is not necessary • Degree of control is relevant

Remember Two Things • Not all units within an organization need to be the same! • Profit centers do not have to make a profit!