Download

1 / 8

80 likes | 159 Views

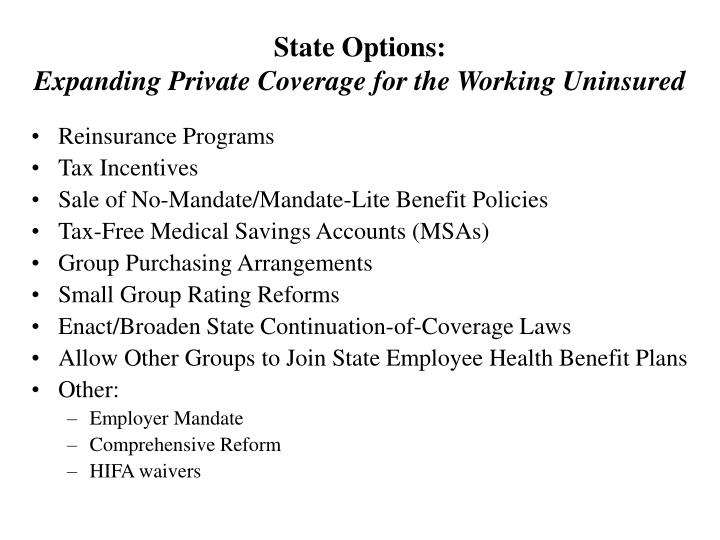

State Options: Expanding Private Coverage for the Working Uninsured. Reinsurance Programs Tax Incentives Sale of No-Mandate/Mandate-Lite Benefit Policies Tax-Free Medical Savings Accounts (MSAs) Group Purchasing Arrangements Small Group Rating Reforms

E N D

State Options: Expanding Private Coverage for the Working Uninsured • Reinsurance Programs • Tax Incentives • Sale of No-Mandate/Mandate-Lite Benefit Policies • Tax-Free Medical Savings Accounts (MSAs) • Group Purchasing Arrangements • Small Group Rating Reforms • Enact/Broaden State Continuation-of-Coverage Laws • Allow Other Groups to Join State Employee Health Benefit Plans • Other: • Employer Mandate • Comprehensive Reform • HIFA waivers

Expanding Private Coverage for the Working UninsuredReinsurance Programs • Reduce steep premium increases for small employers with high claims experience • Present in at least 21 states • VA: Unsuccessful attempts to establish pilot projects • Lessons Learned: • Many state pools are inactive or have low enrollment • Substantial subsidies and marketing efforts needed • Keys to success: • Low (subsidized) premiums, high benefits, significant insurer participation • VA Regulatory Implications ??

Expanding Private Coverage for the Working UninsuredTax Incentives • Tax relief (deductions or credits) to employer/individual who purchases health insurance • Examples • Oklahoma: 100% credit for employers whose eligible employees participate in state-certified basic benefit plan • VA: 2005 bill would provide income tax credit for small employers (< 50 employees) for cost of health insurance premiums • Several states allow self-employed individuals to deduct full amount of insurance premium payments • Subsidies appear to have minimal impact on increasing coverage; To be effective, subsidies must be substantial (60%+). • VA Regulatory Implications?

Expanding Private Coverage for the Working UninsuredSale of No/Low Mandate Benefit Policies • Intent: By dropping requirement to cover mandated benefits, price of coverage will decline and more will buy coverage. • Handful of states have exempted certain insurers from covering certain state health benefit mandates • VA: Established special advisory committee (1990) to examine efficacy of mandated health benefits; 2004 bill would place moratorium on new insurance mandates until 2009. • Lessons Learned • Not clear that waiving benefit mandates increases coverage • Benefit mandates have strong negative impact on small employers • VA Regulatory Implications?

Expanding Private Coverage for the Working UninsuredTax-Free Medical Savings Accounts • MSAs: For covered individuals that assist to finance part of cost of deductibles, copays, other medical expenses not covered by insurance plan • Most states allow income tax deductibility for MSAs as allowed under federal law • VA: 2002 implementation plan found to show low participation to date and # insurers offering MSA coverage has declined; 2005 bill would develop system of tax deductions for employers contributing to HSAs, providers delivering reduced/free care to HSA holders, and working poor. • Lessons Learned: Unclear if MSAs have had measurable impact on coverage rates; Tax deductibility appears to mainly benefit upper and middle income employees (less likely to be uninsured). • VA Regulatory Implications?

Expanding Private Coverage for the Working UninsuredGroup Purchasing Arrangements • Most such arrangements permit small employers to band together to purchase insurance and negotiate provider discounts • Over 20 states have authorized formation of purchasing cooperatives • VA: Previous studies found cooperatives not to be effective in achieving significant savings; current legislation requests: 1) state to design voluntary public/private purchasing pool, 2) provider groups to report on high-deductible insurance plans • Lessons Learned: Little evidence that group purchasing increases coverage rate or ability of small employers to offer such insurance. • VA Regulatory Implications?

Expanding Private Coverage for the Working UninsuredSmall Group Rating Reforms • Designed in part to increase # of small employers that offer insurance by controlling variability in premium rates. • Examples • NY: Requires insurers to charge all small employers the same per-employee rate for the same coverage • VA: Small employers are provided with guaranteed issue and can also participate in association-sponsored health plans; Earlier consideration given to including self-employed in small group market. • Lessons Learned: Small group reforms have not appeared to raise chances of small employers offering coverage or employees taking up coverage. • VA Regulatory Implications?

Expanding Private Coverage for the Working Uninsured • State Continuation-of-Coverage Laws • Allow employees to continue health coverage under employer-sponsored plan after employee leaves • Nearly all states require insurers to offer continuation coverage • Lessons Learned: No state studies exist; Studies of federal COBRA shown to have positive influence. • VA Regulatory Implications? • Allow Others to Join State Employee Health Benefit Plans • State-employee health benefit plans in at least: • 30 states cover public colleges/universities; 20 states cover public schools; 22 states cover cities and counties • VA: 2004 law allows part-time state employees to participate; 1990 measure allows local gov’t employees to participate • Lessons Learned: Not known; no studies exist • VA Regulatory Implications?