Download

1 / 42

420 likes | 600 Views

Lecture 5 Monopoly practice and the competitive limit.

E N D

Lecture 5Monopoly practice and the competitive limit The latter parts of the lecture analyze other aspects of monopolistic practices. We discuss mechanisms for setting prices and quantities, the role of commitment, market segmentation, and product bundling. Then we investigate the effects of competition,the competitive limit and the related concept of competitive equilibrium.

A dynamic inconsistency? But what if the monopolist set price so that marginal revenue equals marginal cost, and the demanders whose valuations exceeded the price immediately purchased the item at the beginning of the game?

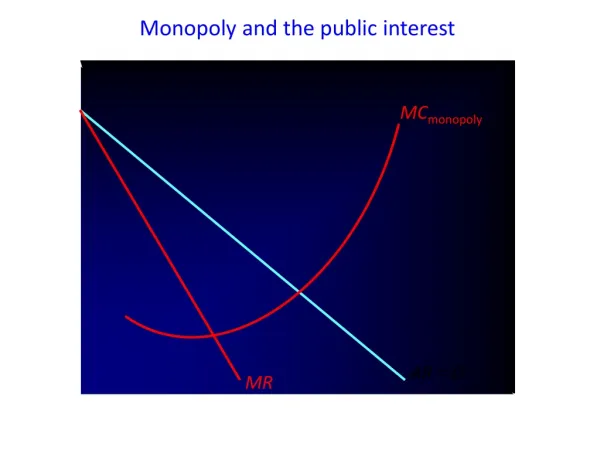

The static solution illustrated Price in dollars 20 inverse demand curve Uniform price solution unit cost 10 marginal revenue curve quantity 0 Uniform quantity solution

Residual demand Price New vertical axis for origin of residual inverse demand 20 Uniform price solution Unit cost 10 New marginal revenue curve Quantity 0

Will price fall to marginal cost? • The solution to this game is for the monopolist to let the price decline to where marginal revenue equals marginal cost at the end of the game, thus presenting each consumer simultaneously with a take it or leave it offer at that price. • Equivalently, the monopolist can commit to a uniform price policy by committing to everyone the lowest price he offers to anyone. • Letting a firm split can also resolve the problem if each of the new break off firms guarantee to match each other’s discounts.

Durable goods monopoly • One way of avoiding the problem associated with a random cut-off time is to rent the good for short periods. • But this is not always possible, and it might be desirable to attempt to price discriminate between consumers. • There are two cases to focus on: • 1. Constant marginal cost • 2. Fixed supply

Discriminating monopolist • Price and product discrimination is more widespread than in durable goods problems, where the monopolist may be able to sort customers by their urgency. • Suppose the monopolist knows the valuations of the players, and can commit to prices. • Make a take it or leave it offer to each person: multi person ultimatum game. • Now imagine that it cannot prevent players from buying in any market they like. • Now let monopolist condition on characteristics that are related to their valuations which he cannot observe.

Multiple markets • Consider now another related method for segmenting market demand to extract greater economic rent. • The firm exploits the idea that customers who demand several of the firm’s products might exhibit more elastic demands (be more price sensitive) than customers who only wish to purchase a smaller subset of the firm’s products. • Perhaps the most common example of this behavior is quantity discounting (sometimes enforced through packaging).

Other examples • Firms sell assembled goods such as cars or other durables for new car buyers and demand from previous buyers, plus replacement parts arising from collision damage or wear and tear. • Restaurants (furniture stores, car dealers) offer complete dinners (suites, high performance and luxury packages) with a limited (selected) range of items, and also offer portions a la carte (set pieces, individual components). • Ski resorts (amusement parks, cellular phone companies internet or cable operators) offer vacation packages for lodging and tickets (entry or connection plus service charges) as well as sell tickets (services) by themselves.

A product bundling monopolist • A resort owner has a monopoly over two products, called accommodation on the mountain, and ski lift tickets. • Some demanders visit the mountain resort to ski downhill, while others come to cross country ski or snowshoe (neither of which requires lift tickets). Demanders also choose between commuting from the city 90 minutes by road, or by renting an apartments or a hotel room at the resort. • What should the resort owner charge for ski tickets, for accommodation, and for the holiday package of both?

The number of rivals • Now we investigate how the solution to trading games is affected by relaxing the assumption that there is only a single supplier (or more generally dealer) in each market. • First we analyze how monopoly power breaks down with competition from rival producers. • This leads us to define price taking behavior and a definition of competitive equilibrium.

The competitive limit • We first consider two extensions of the multiunit auction, where there is a constant marginal cost of production. • In the first case we assume that entry occurs sequentially until it is unprofitable to do so. This corresponds to a competitive market where rival suppliers compete for demanders. • In the second case we assume that the monopolist or cartel maximizes producer surplus.

Duopoly Considering the monopoly problem of the previous lecture, let us now introduce a second seller with same marginal cost schedule, and no fixed costs.

Three or more producers • Continuing in this vein, one could fragment the organization of production even more. • For example consider how three or more producers would compete against each other. • Can we endogenously determine the number of entrants?

Price competition and capacity constraints • It seems that a remarkably small number of competing firms suffice to drive the price down to marginal cost. • But this result is partly driven by the cost structure. • Now suppose there is a two stage game, where firms construct capacity for production in the first stage, and market their produce in a second stage.

Declining marginal cost Now suppose unit costs fall with scale of production. For example suppose there is a fixed cost of entry (technological know how or plant set up) as well as a constant marginal cost. If there is only one producer, then the profit maximizing quantity for the firm is What happens in the case of two producers?

Is there convergence? • A natural question to ask is where this process would converge, and whether there is an easy way to model what would happen in the limit. • Do our experiments suggest that the limit point depends on the cost structure? • Another question is how many firms are required to reach this limit (that is when it exists).

Free entry • Consider first the uniform distribution. In a second price auction • In the first case we assume that entry occurs sequentially until it is unprofitable to do so. This corresponds to a competitive market where rival suppliers compete for demanders. • In the second case we assume that the monopolist or cartel maximizes producer surplus.

Definition of competitive equilibrium A competitive equilibrium is a single price, or a price band (an interval on the real line), with two defining properties: 1. Traders treat each point in the competitive equilibrium as a fixed price, seeking to buy or sell units of the good that maximize their objective function at that fixed price. 2. At every price above those in the competitive equilibrium, demand exceeds supply. At every price below those in the competitive equilibrium, supply exceeds demand.

Competitive equilibrium as a tool for prediction • The key advantage from assuming that markets are in competitive equilibrium is that models of competitive equilibrium are relatively straightforward to analyze. • For example, deriving the properties of a Nash equilibrium solution to a trading game is typically more complex than deriving the competitive equilibrium for the same game. • In other words, using the tools of competitive equilibrium we can sometimes make accurate predictions with minimal effort.

An economy with one stock • Consider the following economy: • There is one stock, as well as money. The common value of the asset is constant, and every one is fully informed. • There are a finite number of player types, say I. Every player belonging to a given player type has the same asset and money endowment, and the same private valuation. • Players belonging to type i are distinguished by their initial endowment of money mi and the stock si, as well as their private valuation of the stock vi. Thus a player type i is defined by the triplet (mi, si, vi).

Example 1 • To make matters more concrete, suppose there are 10 players, with private valuations that take on the integer values from $1 to $10. • Suppose the third player (with valuation $3) is endowed with 4 units of the good, and everybody else has $12 to buy units of the good. • We also assume that everyone has the same access to the market, and can place limit or market orders.

Example 2 • Now we modify the example a little. • To make matters more concrete, suppose there are 10 players, with private valuations that take on the integer values from $1 to $10. • Suppose the third player (with valuation $3) is endowed with 4 units of the good, and everybody else has $12 to buy units of the good. • As before we assume that everyone has the same access to the market, and can place limit or market orders.

Using supply and demand curves to derive competitive equilibrium • To derive the competitive equilibrium, compute the demand for the asset minus the supply of the asset (both as a function of price), otherwise known as the net demand for the asset. • Then aggregate across players to obtain the aggregate net demand. • The set of competitive equilibrium prices is found by applying the second part of the definition: every price below (above) prices in the set generate positive (negative) aggregate net demand.

Individual optimization in a competitive equilibrium • In a competitive equilibrium with price p the objective of player i is to pick the quantity of stock traded, denoted qi, to maximize the value of his or her portfolio subject to constraints that prevent short sales (selling more stock than the the seller holds) or bankruptcy (not having enough liquidity to cover purchases). • The value of the portfolio of player i is:

Constraints in the optimization problem The short sale constraint is: The solvency constraint is These constraints can be combined as:

Solution to the individual’soptimization problem The solution to this linear problem is to specialize the stock if vi exceeds p, specialize in money if p exceeds vi, and choose any feasible quantity q if vi = p. That is: and:

Aggregate demand • Summing across the individual demands of players we obtain the demand across players curve D(p). • Let 1{ . . .} be an indicator function, taking a value of 1 if the statement inside the parentheses is true, and 0 if false. Then, the demand from those players who wish to increase their holding of the stock is: • Thus D(p) declines in steps, for two reasons. As p falls the number of players with valuations exceeding p increases, and demanders who are willing to buy at higher prices can now afford to buy more units.

Aggregate supply • Summing over the individual supply of each player we obtain the aggregate supply curve S(p), the total supply of the asset from those players who want to sell their shares, as a function of price : • Following the same reasoning as on the previous slide, the supply curve is a step function which increases from min{v1,v2, . . . ,vI}, where the steps have variable length of si.

Indifferent traders • This only leaves stockholders whose valuation vi = p, who are indifferent about how much they trade. They are equally well off selling up to their endowment si versus buying up to their budget constraint mi/p: • The next step is to those prices for which there is excess supply, which we denote by p+. Then we derive those prices for which there is excess demand, denoted p-. • The set of competitive equilibrium are the remaining prices.

Solving for competitive equilibrium • We find those prices for which there is excess supply, which we denote by p+. Then we derive those prices for which there is excess demand, denoted p-. The set of competitive equilibrium are the remaining prices. • By definition the p+ prices are defined by the inequality that: • Similarly the p- prices are defined by:

Aggregate supply in the first example • At prices above $3, the third player will supply 4 units, and at price $3, the player is indifferent between supplying quantity between 0 and 4. No one supplies anything to the market at less than $3. • Define q as any quantity satisfying the inequalities: • Then the supply function is:

Aggregate demand in the first example • To make the problem more manageable we will assume that traders can buy fractions of units, rather than just whole ones. • Then we can write the demand schedule as:

Competitive Equilibrium in the first example • In this example, there is a unique equilibrium price at Note that at prices above , demand shrinks quite markedly because infra marginal demanders can no longer afford more than one unit. Similarly at prices below , demanders want considerably more than what producers can supply. • However at the unique equilibrium price not all demanders are able to fulfill their plans. In limit order markets those demanders who enter their orders first receive priority over those who recognize the equilibrium price later.

Aggregate supply in the second example • Recall that aggregate demand in the both examples is the same. We now derive supply as a function of price. • At prices above $3, the third player will supply 4 units, and at price $3, the player is indifferent between supplying quantity between 0 and 4. No one supplies anything to the market at less than $3. • Define q as any quantity satisfying the inequalities: • Then the supply function is:

Competitive equilibrium in the second example • In this example, there is a band of equilibrium prices. At every price between and suppliers and demanders wish to trade units between them. At all these prices both demanders and suppliers are able to fulfill their plans. • However the price is not determined uniquely by the theory of competitive equilibrium. Whereas in the previous example demanders competed with each other for the limited supplier, here demanders and suppliers can bargain over who should receive the most gains from trading.

Optimality of competitive equilibrium • The prisoner’s dilemma illustrates why games reach outcomes in which all players are worse off than they would be in one of the other outcomes. • Notice that in a competitive equilibrium is a single the potential trading surplus is used up by the traders. It is impossible to make one or more players better off without making someone else worse off. • This important result explains why many economists recommend markets as a way of allocating resources.

But is competitive equilibrium realistic? • The short answer is maybe. Whether or not this is true depends on the: • Cost structure • Durability and nature of product demand • Number of firms in the industry • Threat of entry by new firms • Clearly strategy consultants search for situations where these factors are not conducive to the existence of a competitive equilibrium.