Download

1 / 10

130 likes | 315 Views

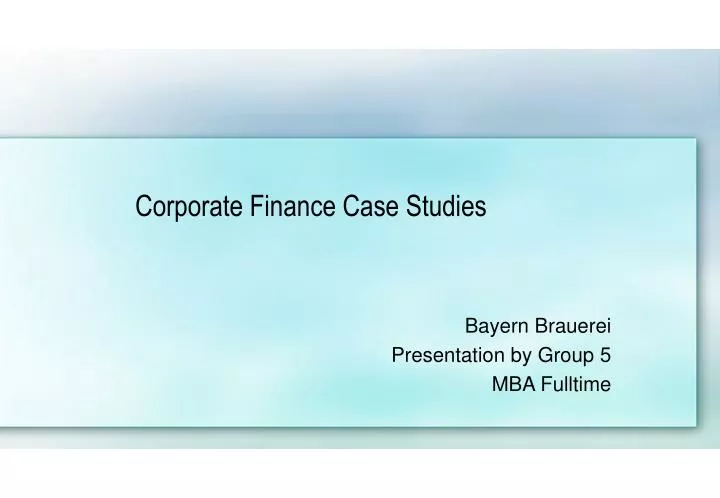

Corporate Finance Case Studies. Bayern Brauerei Presentation by Group 5 MBA Fulltime. 1. Rapid growth in sales. 1. Reasons for rapid growth. Remarkable sales growth only in the east From 0 % in 1989 to 18.4% of s ales in 1992 146 % s ales growth in the e ast (1990-1992)

E N D

Corporate Finance Case Studies Bayern Brauerei Presentation by Group 5 MBA Fulltime

1. Reasons for rapid growth • Remarkable sales growth only in the east • From 0 % in 1989 to 18.4% of sales in 1992 • 146 % sales growth in the east (1990-1992) • 2 % sales growth from 1989 to 1992 in the west • Completely new market in the east • Relaxed credit terms • Field inventories for distribution • Marketing Manager running the business

2. Sustainable growth 1989 1990 1991 1992 Equity Retention Rate 24,99% 25,00% 25,90% 25,55% ROE 9,72% 10,25% 6,30% 7,28% Self Sustainable Growth Rate 2,43% 2,56% 1,63% 1,86% Growth in Sales 4,98% 14,24% 9,14%

2. Reasons for unsustainable growth • Retention of profits too low • Growth in sales is much higher than SSGR • Lack of market research • Sustainable growth only achievable through: • Higher retention • Otherwise: • Raise new equity (Shares, etc.) • Long Term Debt financing

3. Increasing debt • No increase in total debt • Decreasing LTL • Increase only in STL • Debt is the only way to compensate growth rate • Increase in Inventory • Increase in Receivables • Cash surplus from 6m to 12m

4. Accounting Break Even Chart Deutsche Mark (millions) 160 140 120 100 80 60 40 20 0 Revenue Total cost Variable cost Fixed cost 0 100 200 300 400 500 600 700 800 900 1000 Hectolitres of beer sold (thousands)

5. Financial Plan • 8.8m DM in Plant and Equipment • 8.6m DM in Warehouse • Dividends payout: 545,500.00 DM • Should not be approved: • There is no market for further production, if we get the same market share in the east, we are at this point now • We are producing beer, distribution is not our business focus • It should not be financed with STL • Instead... • Rather cut inventories and receivables • Get receivables back to 2% 10 and net 40 • Retain more earnings to finance further expansion plans

Managerial Balance Sheet 1989 1992 Cash 6764 12% 12283 23% WCR 2549 4% 11585 21% Investments 3911 7% 3914 7% Net Assets 44162 77% 26539 49% 57386 100% 54321 100% STL 3765 7% 7884 15% LTL 20306 35% 11066 20% Equity 33315 58% 35371 65% 57386 100% 54321 100%

6. Financially Health • Profitability (ROE) is lower than growth rate and decreasing • Growth in sales is higher than the SSGR • Times interest ratio declines, showing high interest rates on STL • Low retention rate • High reliability on STL • No application of financial and accounting principles • Liquidity ratio from 3.71 (1989) to 1.72 (1992) • Bad WCC-management • Max Leiter´s compensation?