Download

1 / 29

290 likes | 410 Views

Building the Balanced Scorecard. Introduction. Balanced Scorecards provide a framework for communicating strategy in operating terms (measurements and targets). You must communicate strategy in operating terms if you expect people to execute on your strategy.

E N D

Building the Balanced Scorecard Matt H. Evans, CPA, CMA, CFM

Introduction • Balanced Scorecards provide a framework for communicating strategy in operating terms (measurements and targets). • You must communicate strategy in operating terms if you expect people to execute on your strategy. • When people are asked about strategy, they reach for their balanced scorecard. Matt H. Evans, CPA, CMA, CFM

Agenda • This slide presentation will outline the major steps for building a balanced scorecard. • How you execute these steps will depend upon many factors: Company culture, tolerance for change, leadership, etc. • However, please try to follow the same sequence, focusing on the strategic maps. Matt H. Evans, CPA, CMA, CFM

Overview • Balanced Scorecards are constructed from strategic maps • Throughout the process, we will refer back to these maps, making sure everything is linked. This is very important since we want to capture a “cause and effect” relationship in building the scorecard. Matt H. Evans, CPA, CMA, CFM

Why the Balanced Scorecard • Improves how you communicate strategy • Superimposes a discipline whereby you capture cause-effect; otherwise you create pockets of under-performance. • Also forces you to think about strategic measurement as opposed to tactical or operating type measurements Matt H. Evans, CPA, CMA, CFM

Start with Strategy • Begin with your strategic plan – what things are critical to future success? • Focus on customers – what values will we add to our customers • Define the processes – how will we deliver these services to our customers • Build the organization – what capabilities must we put in place Matt H. Evans, CPA, CMA, CFM

Strategic Goals • The first components of your strategy are goals. • Strategic goals establish direction in concrete terms. • Strategic goals anchor the rest of the process. • Strategic goals should fit with the vision and mission of the organization. Matt H. Evans, CPA, CMA, CFM

Goal Attributes • Very short statement • Directly relates to the mission • Broad in scope • Covers long time period (such as 3 years) • Examples: - Improve Customer Service - Leverage Core Competencies - Develop more innovative products Matt H. Evans, CPA, CMA, CFM

Strategic Objectives • Once we establish our first anchor (goals), we can develop a set of strategic objectives. • Strategic objectives define what actions must be taken to reach the strategic goals. • Objectives are critical to future success. For example, in order to grow revenues, we must introduce new products and expand our market share. Matt H. Evans, CPA, CMA, CFM

Objective Attributes • Longer statement than goal statement • More specific than goal statement • Indirect relationship to mission • Covers shorter time period than goal (such as 6 months or 1 year) • Example: - We will expand call center services to include technical support Matt H. Evans, CPA, CMA, CFM

Strategic Themes • Based on strategic goals, three to five strategic themes should emerge. • From these themes, we will develop a strategic map. • Four common strategic themes are: Operating Efficiencies, Customer Relations, Product Innovation, and Growing the Business. Matt H. Evans, CPA, CMA, CFM

Strategic Model • Strategic Models can emerge from four principles: 1. Translate strategies into operating terms. 2. Link strategies throughout the entire organization. 3. Commit everyone to implementing strategy. 4. Make strategizing a continuous process of learning and adjusting to change. Matt H. Evans, CPA, CMA, CFM

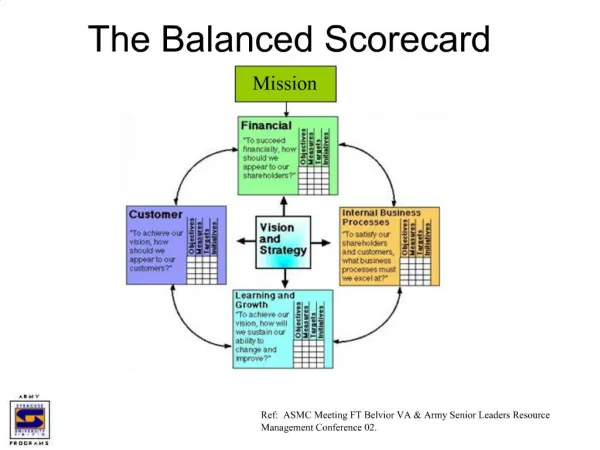

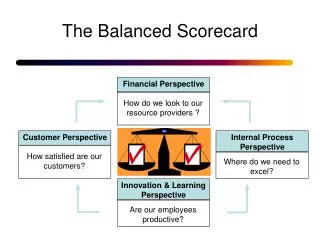

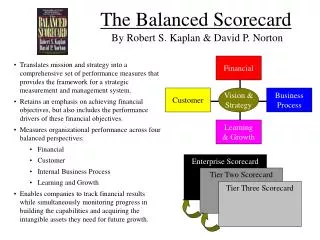

Four Perspectives • Before we build strategic maps, we need to define four perspectives: Financial: Top layer in the map, represents financial outcomes (profits, revenues, etc.) Customer: Next layer down, enables financial results (service, image, price, quality, etc.) Internal Processes: The values added to customers, such as delivery, production, distribution, etc. Learning & Growth: The people, systems, and organization that enable processes. Matt H. Evans, CPA, CMA, CFM

Strategic Mapping • Strategic Maps are the foundation of the Balanced Scorecard. • You will need one strategic map for each strategic theme. • Maps are constructed over four perspectives. • Strategic objectives are mapped over the four perspectives, linked together. Matt H. Evans, CPA, CMA, CFM

Linking • Strategic objectives need to be placed in the Strategic Map according to which perspective fits with the objective. • Objectives may cross over more than one perspective. • We usually start at the top with outcomes and work our way down, looking at what enables (drives) the outcome. Matt H. Evans, CPA, CMA, CFM

Approval • Once you have completed the strategic maps, you will need to get approval from executive management. Does this map accurately tell the “story” of our strategy? • If management disagrees with the map, go back and redo the maps. We need to get this step right since it represents the foundation for the entire scorecard. Matt H. Evans, CPA, CMA, CFM

Measurements • For each strategic objective, you need one measurement. • Measurement provides us with feedback on meeting the strategic objective. • Most organizations will use many of their existing measurements. • Organizations requiring major change should include driver type measurements. Matt H. Evans, CPA, CMA, CFM

Measurement Criteria • Measurements should drive change, providing teeth to our strategy. • Measurements define objectives in specific terms. A good measurement should tell you what your objective is – this is an indicator of good linkage. • Measurements should be repeatable, quantifiable, and verifiable. Matt H. Evans, CPA, CMA, CFM

Good Measurements • Customer satisfaction: - Response time to service customer - Satisfaction survey scores • Process Efficiency: - Cycle time - Downtime - Number of Restarts Matt H. Evans, CPA, CMA, CFM

Lead and Lag Measurements • Leading measurements are drivers behind performance and provide some predictability (forward looking) • Lagging measurements are usually final outcomes that look back, such as customer satisfaction or return on investment • Balanced scorecards should include both leading and lagging type measurements Matt H. Evans, CPA, CMA, CFM

Targets • Once you establish measurements, you need to set a target for each measurement. • Targets push the organization to a required level of performance. • Targets put focus on the strategy, expressing the specifics of the strategy. • When an organization hits its targets, then it has successfully implemented its strategy. Matt H. Evans, CPA, CMA, CFM

Examples of Targets • Total Time to Recruit New Employees: Less than 40 days by year-end • Utilization of rental facilities: Increase to 85% during peak summer months • Growth in top line revenues: 10% increase over last year • Improve overall customer satisfaction: Total scores exceed 90% Matt H. Evans, CPA, CMA, CFM

Initiatives • In order for things to happen in an organization, you must initiate major projects or programs. For example, improving customer service may require a new customer management system. • Once you launch appropriate initiatives, you should be able to meet your strategic objectives. This closes the loop, everything is now linked and away we go! Matt H. Evans, CPA, CMA, CFM

Initiative Attributes • Sponsored by senior management • Designated owners manage project(s) • Includes deliverables or milestones • Usually has some time deadlines • Could be difficult to launch – lack of support, no funding, poorly defined, etc. Matt H. Evans, CPA, CMA, CFM

Templates Throughout this process, we will use templates to capture, analyze and document data. Templates are used for strategic mapping, defining measurements, etc. Matt H. Evans, CPA, CMA, CFM

Other Important Steps • Scorecards are built around three teams: Leadership Team (upper level management), Core Team (middle level management) and Measurement Team (lower level functional personnel). • Scorecards are built around at least four group meetings: Kick Off Meeting followed by at least one meeting for each of the three teams. Matt H. Evans, CPA, CMA, CFM

Implementation • The minimum time for developing a balanced scorecard is three months. • Full deployment of scorecards throughout the entire organization can take more than one year. • The best place to start building a scorecard is where all components of the value chain are in place: Customer, Innovation, Production, Delivery, Services, etc. Matt H. Evans, CPA, CMA, CFM

Summary • Balanced Scorecards are the best way of communicating strategy. • Scorecards rely on a fully integrated approach: Goals, Objectives, Mapping, Measurements, Targets, and Initiatives. • The building of a balanced scorecard can be experimental, whereby you test your strategies, refine, and make changes as you get feedback and learn what works. Matt H. Evans, CPA, CMA, CFM

Where to Get More Information • Formal training in balanced scorecards is available through the Balanced Scorecard Collaborative (www.bscol.com) • Consulting services are available. My training in balanced scorecards comes directly from the Balanced Scorecard Collaborative. If you have questions, feel free to email me. Matt H. Evans, CPA, CMA, CFM