Download

1 / 35

350 likes | 371 Views

Explore the changing landscape of air travel payment systems and the impact on airlines, corporations, and credit card companies. Discover the challenges and options available to bring down credit card costs. Join the discussion on credit card economics and practices.

E N D

Air Travel Payment Systems …what is next ? Alexander Houston Airplus International

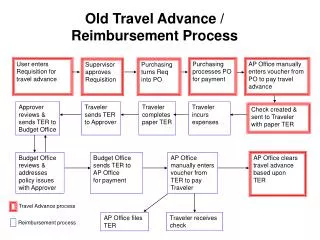

United To Shift Card Costs To AgenciesThe Beat ~ a travel business newsletterNew York City6/24/09 7:30 PMUnited Airlines has informed an unknown number of travel agencies that as of July 20, they will be required to process all credit card transactions using their own merchant accounts.

Agenda • Credit card economics and practices • Analysis of different surcharging models and their effects on: • Airlines • Corporations • Credit Card companies • Options for the Corporation and consumer • Questions / Discussion

Air Travel Payment Systems • Economics and Technology drive Change! • Merchant Fees…the cost of the cards continues to rise • Payment alternatives emerge

Challenges to the interchange model spell change for merchants and buyers.

“Challenges to the current credit card business model will result in greater transparency to the components of the interchange model, and ultimately, to the unbundling of interchange pricing and shifting of roles in the payments value chain among current and new players.” • - A New Business Model for Card Payments, Amy Dawson and Carl Hugener. Cost Transparency – Unbundling Source: “A New Business Model for Card Payments” by Diamond Management Consultants – October 2006

What are merchant fees? What is Interchange? • Merchant fees are the fees merchants pay to the banks to accept the credit card • Interchange refers to the fee banks charge to process a credit card as a form of payment

Current four-party system of the credit card industry Issuer Acquirer Interchange fee e.g. 1.80% of X • Annual fees are often an exception for medium and large corporations • Rebates are on the way to becoming a standard • Bonus programs are on the rise for SMEs Incentives, rebates, bonus programs(optional) e.g. 1.90% of X Annual fee(optional) Merchant fee (Corporate)Cardholder Merchant

The cost of cards • Pressures on Interchange / Merchant fees • Regulatory and litigation • Merchant pressure for transparency • Non-acceptance and increased competition • The transformation is underway • Surcharging • Alternative forms of payment

2/3 of Corporate Card Volume is Spent in Air and Hotel Typical Corporate Card Usage (USA) Source: Runzheimer International Mobility Report, Oct 2006

Merchants Pay a Significant Proportion of the Costs! Card Holders Merchants • Annual fees, if any • Conversion fees • ATM fees • Late, overlimit fees, etc • Revolving credit • interest • Merchant Service Charge 10% - 30% of total 70% - 90% of total Source: AirPlus estimate

Almost 50% of Credit Card costs Spent in Rewards and Branding !!! Typical Corporate Card / Cost breakdown (USA) Source: Diamond Partners

Distribution Economics – The Downward Spiral • Travel intermediaries use the excess funding to buy the business of their customers • Airlines overpay distribution intermediaries for their services • Rebate/Incentive competition drives airlines costs higher

Credit Card Charges GDS fees Travel Agency Commissions Zero-Commission Airlines and other merchants cut distribution costs Terminator 3 Major distribution cost elements for an airline ??? Terminator 2 Surcharging for full content Terminator 1

Merchant Service Fees Range from 1.0% to 2.5% Airlines, Hotel, Car Rental for Corporate Cards Amex 2.0% – 2.5% Visa / MC 2.0% – 2.4% UATP 1.0% – 1.65% Source: Airplus – fees shown typically air only

Average Credit Card Merchant Feefor an Airline Ticket is $12 Ticket Price Expensive Credit Card Inexpensive Credit Card OAK-LAX 80 US$ 2 US$ 0.80 US$ Avg. Ticket for network carrier: 520 US$ 13 US$ 5 US$ ORD – LHR 4,000 US$ 100 US$ 40 US$

Airlines Increasingly Focus on Credit Card Costs „Today Northwest pays more to credit card companies than to GDS‘“ -- Al Lenza, Vice President of Distribution and E-Commerce for Northwest Airlines -- at The Masters Program 2005

„Today Northwest pays twice as muchto credit card companies than to GDS“ - Al Lenza, Vice President of Distribution and E-Commerce for Northwest Airlines - at The Masters Program 2007

Zero-Commission New Products Surcharging Regulate/Negotiate Consumer products like debit cards or PayPal Change credit card business model to user pay principle Flat: Charge the same amount for all credit card bookings European Commission & Anti-trust cases And/or and/or or and Corporate – low cost credit cards & Direct debit Do not accept (some) credit cards on (some) corporate rates Differentiated: Charge according to credit card costs CO branding Airlineshave four major Options Objective: Bring credit card costs down

Zero Commission:Overwhelming Benefits but with Implementation Issues Flat Surcharging:Sounds Easy, But Does Not Change the Costs At All Regulate / Negotiate:More likely overseas than in US New products:Technology can reduce costs, but it takes time

Zero Commission:Overwhelming benefits, but with implementation issues Pros Cons • Merchants can cut up to 90 % of costs, they pay little or no fee • User pays, user selects card • Corporations can choose an inexpensive provider • Price authority with issuer • Implementation has to be simultaneously for all credit cards • if not, credit card providers with no zero-commission have an advantage and an increase in market share • Card holder pays for credit card usage What‘s happening in Asia and France • Hong Kong: • - Credit cards not accepted on corporate net rates. Travel agencies surcharge a fee for credit card usage on Corporate Net Rates. Same for British Airways in the UK. • Mainland China: - Travel agencies surcharge a fee (~4 %) for payments with international credit cards • France: - Low local interchange fees, leading to high annual fees for cardholders and high transaction fees when used outside Eurozone (e.g. 2.4 % of trx volume + 0.70 €)

Surcharging:Sounds easy, but does not change the costs at all Pros Cons • Increased revenue through additional surcharge • Easy implementation • Increased transparency via differential surcharging as costs vary card to card • Corporate / card holder has to pay for card usage • Surcharge does not equal costs • Not legal in all areas • Sends unintended message that credit cards are not preferred What‘s happening in Europe • Merchants surcharge either a fixed amount or a percentage to cover their collection costs Examples in the airline industry: - Lufthansa: € 3 on economy tickets for credit card online sales - British Airways: £ 3 for credit card online sales with invoice address in UK - Ryanair: € 2.50 per coupon for credit cards; no charge for VISA electron; Amex is not accepted - Germanwings: € 6 for credit card sales, except for proprietary credit card

Regulate / Negotiate:Not likely in US Pros Cons • Low cost strategy, because legal approach • Merchants can co-operate and hide behind associations • „Smash banking fees“ popular approach for regulators • Lobbying initiatives focus on VISA and MasterCard as easy targets • No level playing field as Independent providers will immediately benefit • In B2B merchants risk to increase costs What‘s happening in the USA and EU with the authorities • USA: • Authorities have not yet focused on this market • European Commission: - Harmonization of internal market: Single Euro Payments Area (SEPA) to be introduced in 2008 - Visa / MasterCard interchange fees are subject to investigations by European Commission and national anti-trust authorities

New products:A territory not yet fully explored Pros Cons • New products make new pricing more easily accepted • Debit card ideal from a merchant‘s perspective • Debit cards, PayPal, Check Free etc. are B2C products only • New corporate products will require implementation efforts like zero-commission for travel agencies What‘s happening • Airlines upgrade the acceptance of debit consumer cards • Direct debit options for corporations • New corporate products not available yet

The United States is a Mature credit card Market • Credit card usage is culturally ingrained • Incumbent issuers with strong brands and resources • Regulations vary between states But • Cost of the cards keep increasing • Technology is enabing alternatives • It is not just an …“airline thing“

What do I Prefer…? Zero-Commission • Zero-commission aligns credit card costs with other payment options for merchants/airlines • Issuer must cover its costs with its own fees • Stronger price competition between issuers will drive overall costs down • More transparency Differential Surcharging

What do I think will happen…? Incentives to Use lower cost options • Carrot rather than the stick approach in a mature market • Some payment options are better than others for merchants/airlines • Acceptance of new technology in a changing demographic base Negotiation and co-branded cards Technology enabled alternatives

Difficult for Credit Card Companies and the Airlines to Change the Business Model by Themselves Annual Fees Surcharging Traditional Interchange Model Low Cost Cards Open Book

Credit Card Costs: WHAT can I do ?Move Your Cheese or Someone Else Will • Transparency - Information on credit card costs needs to become available…you are paying for it ! • Corporations – be aware of and/or move to a low cost form of payment • Airlines – Incentive for the use of low cost form of payment • Focus on costs will drive costs down • First movers will make the market, e.g. open book policy with credit card company

My prediction…. • Economics and Technology will continue to drive Change! My Advice…. • Know what options are available for your program …Be ready to move! • Proact don’t React!