Download

1 / 8

80 likes | 84 Views

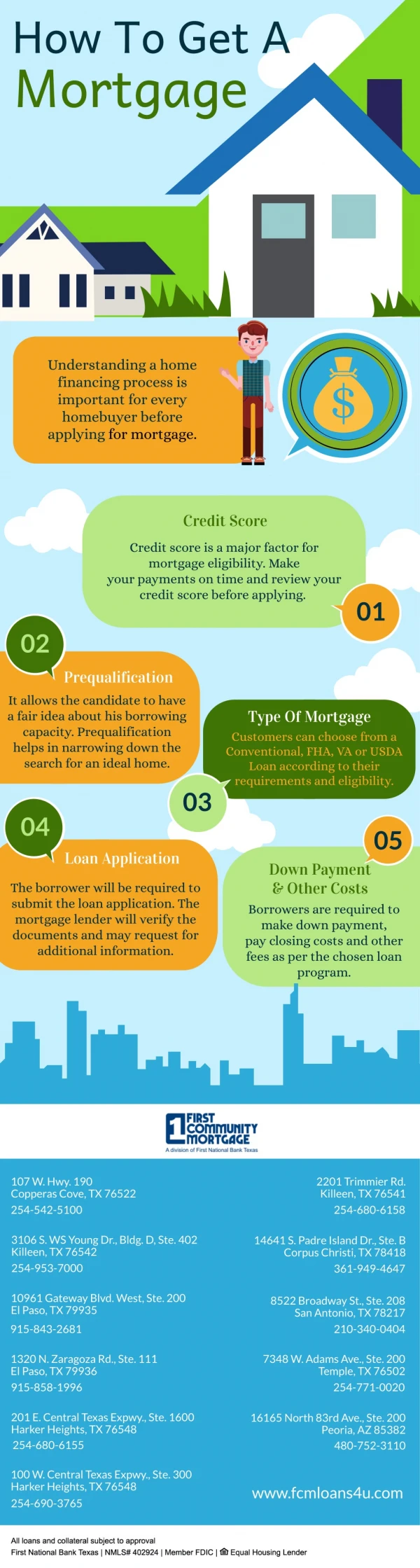

Canadas new mortgage rules can have an impact upon your mortgage, whether youu2019re looking to purchase your first home, or want to switch mortgages or refinance; the following guide should help you make an informed choice:<br><br>

E N D

Canadas new mortgage rules can have an impact upon your mortgage, whether you’re looking to purchase your first home, or want to switch mortgages or refinance; the following guide should help you make an informed choice: The Canadian Mortgage Stress Test Introduced back in 2018, the stress test was designed to protect Canadian homeowners by asking banks to check whether borrowers are still able to make their mortgage payment at a rate that’s higher than the one they will actually pay.

As a Canadian citizen, if you want to qualify for a regulated bank loan, you’ll need to pass the stress test, and this can be achieved by proving that you can afford a mortgage at a qualifying rate. If you make a down payment of 20% or more, the qualifying rate is determined using the Bank of Canadas five-year benchmark, or the interest rate offered by the lender plus 2%, whichever is higher. If your down payment is less than 20%, the qualifying rate will be the higher of the Bank of Canada five-year benchmark rate, and the interest rate your lender is offering you.

Should you be seeking to refinance, change mortgage lenders or take out a secured line of credit, the stress test is also applicable. Other Canadian mortgage rules Last year, in July 2020, high-ratio mortgages (also known as default insured mortgages) to be insured by the Canada Mortgage and Housing Corporation (CMCH), were subjected to several changes, and below are some of the most recent:

Qualification rate Anyone applying for a mortgage will be limited to spending 35% of their gross income on housing, at the most, and are only permitted to borrow up to 42% of their gross income once other loans are accounted for. Previously, the figures were 39% and 44%. Credit score Borrowers are now also required to have a good credit score, at a minimum of 680, and if buying a home with a partner, at least one of you must have a score of 680, up from 600 previously.

Down payment Instead of borrowing funds to do so, buyers must now use their own funds to make a down payment, meaning that they’re no longer able to use unsecured personal loans, unsecured lines of credit or credit cards to help fund it. For buyers making a down payment of 20% or less than the purchase price, must buy mortgage default insurance. If the property they plan to buy costs $1 million or more, they are not eligible for mortgage default insurance.

CMCH projections As a result of various factors, from the pandemic to job losses and a drop in immigration, CMCH have predicted a decrease in housing prices of between 9 and 18% from June 2020 to June 2021, but as of yet, this hasn’t been the case. One of the best ways to make sure that the new Canadian mortgage rules don’t catch you out, is to work with a local, qualified mortgage broker, who will be up-to-date on all laws, rules and regulations, and could even help you get a better deal than you would by shopping around independently.

Mortgage-broker-Calgary is your best resource for finding a mortgage for your property. Luke Wile, is the best mortgage broker in Calgary and is proud to serve clients from across Canada, while being centered in Calgary, Alberta. Luke is proud to serve his clients with a personalized approach to finding his clients the best and lowest Canadian interest rates and terms offered by the major banks and private lending institutions. If you are looking for a Calgary mortgage agent, with Luke Wile you can get fast and personal expertise for your mortgage!