Download

1 / 1

E N D

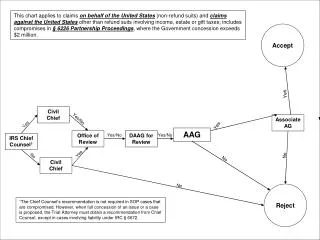

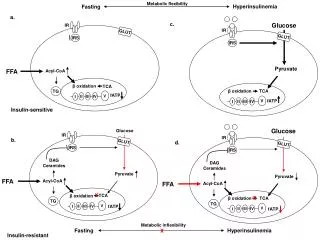

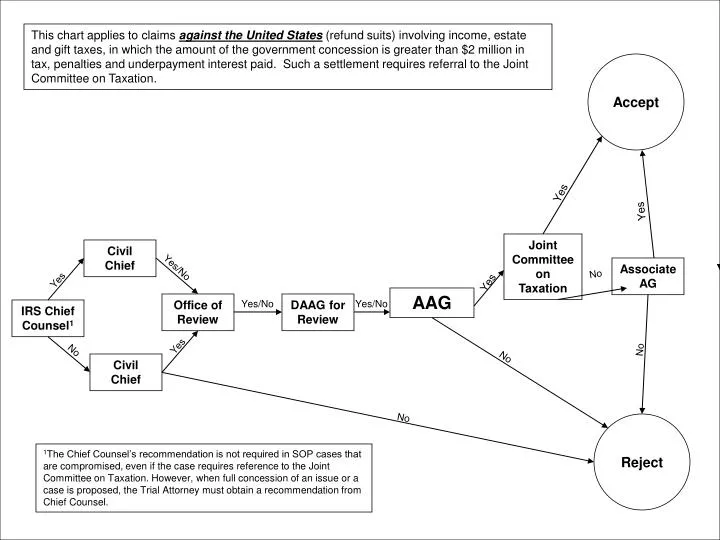

Reject Accept This chart applies to claims against the United States (refund suits) involving income, estate and gift taxes, in which the amount of the government concession is greater than $2 million in tax, penalties and underpayment interest paid. Such a settlement requires referral to the Joint Committee on Taxation. Yes Yes Joint Committee on Taxation CivilChief Yes/No Associate AG No Yes Yes AAG Office of Review Yes/No DAAG for Review Yes/No IRS Chief Counsel1 Yes No No No CivilChief No 1The Chief Counsel’s recommendation is not required in SOP cases that are compromised, even if the case requires reference to the Joint Committee on Taxation. However, when full concession of an issue or a case is proposed, the Trial Attorney must obtain a recommendation from Chief Counsel.