Download

1 / 24

240 likes | 335 Views

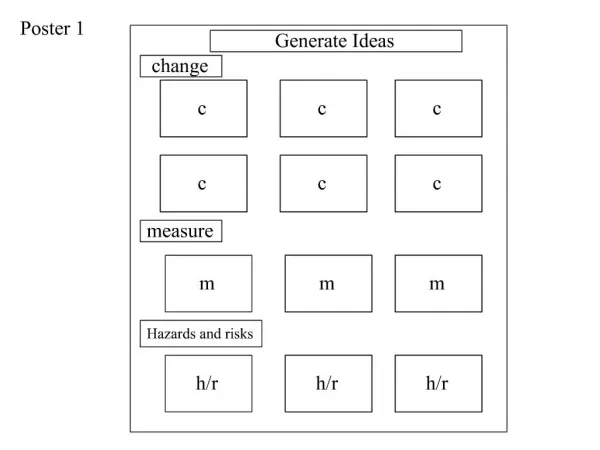

BORROW FROM LOCAL AND INTERNATIONAL BANKS. INVEST IN CORPORATION. GENERATE FUNDS. COLLECT TAX. SELL PUBLIC LANDS AND GOVERNMENT PROPERTIES. POLITICAL INSTITUTIONS. TAX VS TAXATION. % FROM INCOME, PROPERTIES, TRANSACTIONS. A FEE/ BURDEN. TO SUPPORT THE “SERVICES” OF THE GOVERNMENT.

E N D

BORROW FROM LOCAL AND INTERNATIONAL BANKS INVEST IN CORPORATION GENERATE FUNDS COLLECT TAX SELL PUBLIC LANDS AND GOVERNMENT PROPERTIES

TAX VS TAXATION % FROM INCOME, PROPERTIES, TRANSACTIONS A FEE/ BURDEN TO SUPPORT THE “SERVICES” OF THE GOVERNMENT

SYSTEM OF RAISING/ COLLECTING POWER OF THE LEGISLATURE REGULATES FLOW OF INCOME TO CHECK INFLATION

COMPUTATION: INCOME TAX RATES • GROSS INCOME • TAXABLE INCOME • TAX DUE • WITHHOLDING TAX • TAX PAYABLE VS TAX REFUND

I. GROSS INCOME (GI) • Gross income (Monthly Income) x 12

II. TAXABLE INCOME (TI) • GROSS INCOME – ALLOWABLE EXEMPTIONS • (P50,000 (STATUS) + NO. OF DEPENDENTS (not to exceed 4) x P25,000

Qualifications of qualified dependent: • Must be parents, children, brothers or sisters • Must be minor, unmarried and unemployed • Must depend upon the taxpayer for chief support • For dependents over 21 years old, must be incapable of self-support due to mental or physical defect.

III. TAX DUE (TD) • Refer to the tax rate table • AMOUNT UNDER THE RATE COLUMN + PERCENTAGE (TAXABLE INCOME – AMOUNT UNDER THE OVER COLUMN)

P 22, 500 + [ 25% (P 250, 000 – P 140, 000)] • = P22, 500 + [25% (P110, 600)] • =P22, 500 + P27, 500 • NOTE: 250, 000 = NET TAXABLE INCOME

IV. WITHHOLDING TAX (WT) • Refer to the withholding tax table • Step 1: check the status • ME1 OR S1 • ME: MARRIED EMPLOYEE • S: SINGLE • 1: NUMBER OF QUALIFIED DEPENDENT • Step 2: Select whether the monthly income falls under the categories of employees with or without qualified dependents. Align the monthly income to the nearest possible amount not exceeding the subsequent constant numerical value on the right column. • Step 3: after aligning the amount, subtract the monthly income to the matched nearest amount on the table. The difference should not be negative. • Step 4: multiply the result that you got from step 3 to the indicated % on the status row • Step 5: add the result to the “exemption amount” • MULTIPLY THE ANSWER BY 12 MONTHS, WITHHOLDING TAX SHOULD CLOSELY MATCH THE TAX DUE

V. TAX PAYABLE VS TAX REFUND • TAX DUE – WITHHOLDING TAX THAT WAS MULTIPLIED BY 12 • TAX REFUND • NEGATIVE: RETURN OF EXCESS TAX • TAX PAYABLE • MORE THAN 0: ADDITIONAL CREDIT TO THE GOVERNMENT

EXAMPLE • MR. O, MARRIED, HAS A MONTHLY SALARY OF P32,000. HE HAS 7 CHILDREN. FOUR ARE ALREADY WORKING. TWO ARE STILL IN HIGH SCHOOL & ONE IN ELEMENTARY. • FIND THEIR: • (A) GROSS INCOME, • (B) NET INCOME, • (C) TAX DUE, • (D) WITHHOLDING TAX, • (E) TAX PAYABLE OR TAX REFUND