Download

1 / 1

10 likes | 25 Views

credit providers check your credit score to determine approval or rejection as well as to figure out other crucial details of your loan terms such as interest rate and payment terms....Read more to know how raising a fair credit score to very good could save your money.

E N D

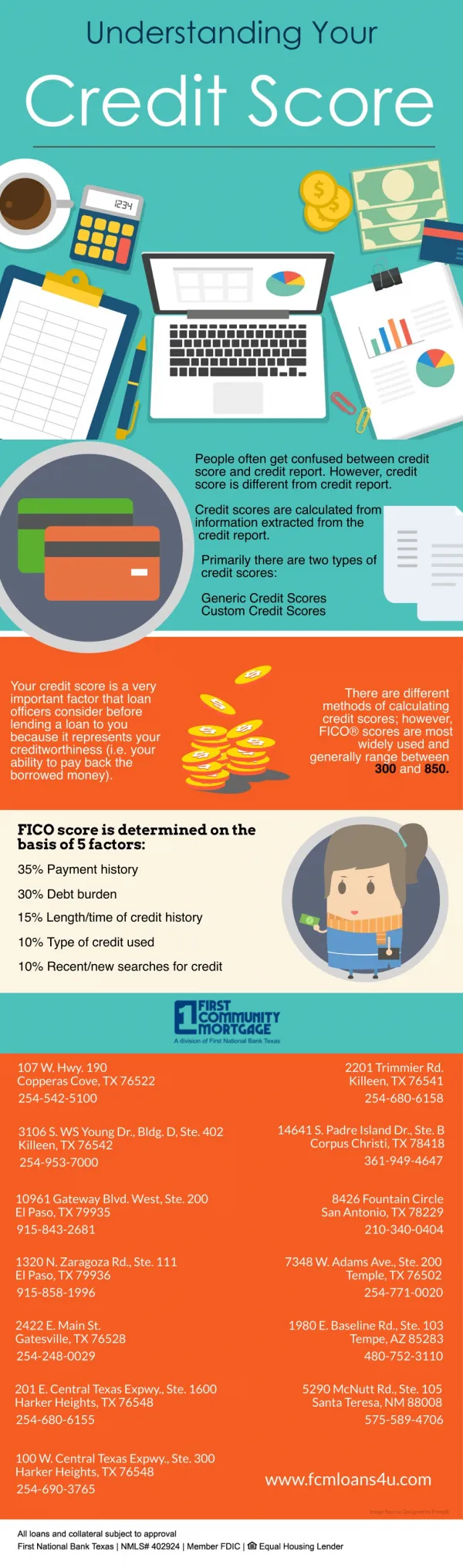

Blog Raising a Fair Credit Score to Very Good Could Save Your Money Making a habit to check your credit score is critical so you can maintain a healthy credit record. Personal loan providers and lenders use credit score in order to check eligibility for personal loan and determine whether or not they should extend credit to you. When you apply for personal loan, it pays to know your credit score because apart from the various documents required for personal loan application, credit providers check your credit score to determine approval or rejection as well as to figure out other crucial details of your loan terms such as interest rate and payment terms. The lower your credit score is, the less likely that you will get approved for the loan you are applying for. Should you get approved despite a low credit score, high interest rates typically follow, which can only mean more cost to pay in the long run. This is why improving your credit rating is always advisable before you even apply for personal loan. This will help you save a good deal of money in terms of lower interest rates and better loan terms when you get free credit score from fair to a very good rating. Credit scores can typically be broken down into five general categories, each constituting a particular percentage of the entire credit rating. Your payment history typically makes up 35% of your credit rating, followed by total amounts owed, which accounts for 30%. The length of your credit history makes up 15% of your credit score, while type of credit in use and new credit constitute 10% each. There are many ways that you can improve your credit score to get better chances of having your loan requests approved. You can do this by organizing your existing loans and making payments on time, never missing due dates, and keeping your total debt load and dues under control. It also pays refraining from opening new accounts and instead keeping old accounts open and healthy. This will allow creditors to see how well you maintain your credit history, causing them to rule in favor of your loan.