Download

1 / 15

150 likes | 263 Views

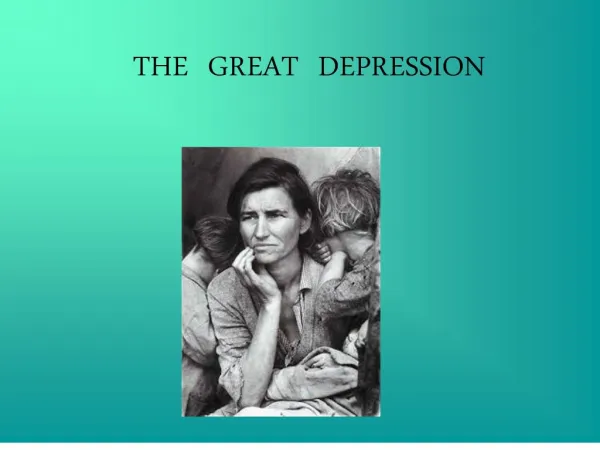

The Great Depression. The United States Experience 1929-1941. What Caused the Great Depression?. Why was aggregate demand so low? Is there evidence to support monetary impotence or evidence of a failure of the economy to self correct?

E N D

The Great Depression The United States Experience 1929-1941

What Caused the Great Depression? • Why was aggregate demand so low? Is there evidence to support monetary impotence or evidence of a failure of the economy to self correct? • Did the aggregate supply curve shift down and to the right, permitting the economy to self correct? • Were nominal wages rigid and did real wages fluctuate procyclically or countercyclically?

Data • Year MS Real MS Real Y Real I Y/YN PI UR r Avg Hourly Avg Real Hr • ($, b) ($, b, 1929 prices) % % % Earnings ($) Earnings ($) • 26.0 26.0 103.7 14.9 102.8 100 3.2 3.6 0.563 0.563 • 25.2 26.1 94.8 11.4 90.8 96.3 8.9 3.3 0.560 0.581 • 23.5 26.7 88.7 8.0 82.1 86.3 16.3 3.3 0.532 0.605 • 20.6 25.5 77.2 4.5 69.0 76.2 24.1 3.7 0.485 0.600 • 19.4 24.4 76.1 3.9 65.7 74.1 25.2 3.3 0.457 0.575 • 21.4 26.0 84.3 5.2 70.4 78.3 22.0 3.1 0.512 0.623 • 25.3 30.4 91.9 6.7 74.1 79.8 20.3 2.8 0.524 0.630 • 28.8 34.4 103.7 8.9 80.8 80.7 17.0 2.7 0.534 0.637 • 30.2 35.0 109.2 11.0 82.2 84.2 14.3 2.7 0.566 0.656 • 29.8 35.3 105.4 9.1 76.7 81.7 19.1 2.6 0.576 0.681 • 33.4 39.8 114.0 10.9 80.1 80.7 17.2 2.4 0.583 0.695 • 38.8 45.8 123.7 13.2 84.0 81.9 14.6 2.2 0.597 0.705 • 45.4 51.1 144.9 15.5 95.0 87.4 9.9 2.0 0.655 0.737

Weak Aggregate Demand • According to the data, the primary initial cause of the Great Depression was a decrease in investment spending. • Real fixed investment fell by 74% from $14.9 billion in 1929 prices in 1929 to $3.9 billion in 1933. • By 1939, real fixed investment was still 27% below the 1929 level despite a 53% increase in the money supply.

Weak Aggregate Demand • According to the IS/LM interpretation of events in the 1930s, the IS curve shifted to the left while the LM curve shifted to the right. • The failure of investment to recover is consistent with either a vertical IS curve or a horizontal LM curve. • Which is right?

IS/LM Model IS r r LM1 LM2 LM LM3 r4 LM4 r3 r2 r1 r1 IS 0 0 Y1 YN Y Y1 YN Y Vertical IS Curve Horizontal LM Curve

Vertical IS? Horizontal LM? • The IS curve is vertical (or nearly vertical) when a decline in interest rates fails to stimulate new investment spending. • From 1934 to 1940, the interest rate declined from 3.1% to 2.2% while investment spending increased from $5.2 billion to $13.2 billion. • Apparently, the IS curve was not vertical.

Vertical IS? Horizontal LM? • The LM curve is horizontal when an increase in the money supply fails to reduce interest rates. • From 1934 to 1940, the real money supply increased from $26.0 billion to $45.8 billion while interest rates fell from 3.1% to 2.2%. • Apparently, the LM curve was not horizontal.

Monetary vs. Non-monetary Factors • Gordon and Wilcox determined that both monetary and non-monetary factors contributed to the depression, but at different times. • From 1929 to 1931, the drop in the money supply was not sufficient to cause the collapse of GDP. • The collapse must be explained by the loss of wealth in the stock market and the overbuilding that occurred during the 1920s. • But after 1931, the contraction was caused mainly by monetary factors, particularly the failure of the banking system.

Prices and the Output Ratio • Does the behavior of output and the price level support the Keynesian assumption of rigid nominal wages or the classical interpretation of a self-correcting economy? • If the classical story is correct, then decreases in the price level should cause the economy to return to full employment. • If the Keynesian story is correct, then the failure of nominal wages to fall should hamper the recovery.

Self Correction? • The story of the Great Depression appears to lie in shifts of the aggregate demand curve to the left and then over time to the right. • There is no evidence of a shift in the aggregate supply curve to the right as the price level fell. • Between 1936 and 1940, there was no deflation despite the fact that Y/YN was at or below 86%.

The Price Level and Y/YN LAS P 1929 100 1930 1931 1937 1941 1938 1940 1934 1939 1932 1933 75 Y/YN P 0 50 60 70 80 90 100 110 P 100 AD1929 AD1941 75 AD1933 LAS Y/YN Gordon, p. 222 0 50 60 70 80 90 100 110

Behavior of Nominal Wage Rates • Why did the aggregate supply curve fail to shift? • A fixed AS curve requires a rigid nominal wage. • Between 1929 and 1930 when real GDP fell by 9%, nominal wages did not decline at all. • Nominal wages fell between 1931 and 1933, but rose again by 12% in 1934 when unemployment was 22%. • By 1937, nominal wages equaled those of 1929 despite an unemployment rate of 14%. • Nominal wages were not rigid, but they did not fall continuously after 1933 so were not part of a self correction mechanism.

Behavior of Real Wage Rates • The real wage rose after 1933 despite high levels of unemployment. • This is attributed to government intervention. • During 1934 and 1935, the National Industrial Recovery Act (NIRA) attempted to raise wages and prices by instituting industry-specific codes that required employers to raise wage rates. • The NIRA was declared unconstitutional in 1935, and was succeeded by the Wagner Act, which encouraged union membership.

Data • Year MS Real MS Real Y Real I Y/YN PI UR r Avg Hr Earn Avg Real Hr • ($, b) ($, b, 1929 prices) % % % Earnings ($) Earnings ($) • 26.0 26.0 103.7 14.9 102.8 100 3.2 3.6 0.563 0.563 • 25.2 26.1 94.8 11.4 90.8 96.3 8.9 3.3 0.560 0.581 • 23.5 26.7 88.7 8.0 82.1 86.3 16.3 3.3 0.532 0.605 • 20.6 25.5 77.2 4.5 69.0 76.2 24.1 3.7 0.485 0.600 • 19.4 24.4 76.1 3.9 65.7 74.1 25.2 3.3 0.457 0.575 • 21.4 26.0 84.3 5.2 70.4 78.3 22.0 3.1 0.512 0.623 • 25.3 30.4 91.9 6.7 74.1 79.8 20.3 2.8 0.524 0.630 • 28.8 34.4 103.7 8.9 80.8 80.7 17.0 2.7 0.534 0.637 • 30.2 35.0 109.2 11.0 82.2 84.2 14.3 2.7 0.566 0.656 • 29.8 35.3 105.4 9.1 76.7 81.7 19.1 2.6 0.576 0.681 • 33.4 39.8 114.0 10.9 80.1 80.7 17.2 2.4 0.583 0.695 • 38.8 45.8 123.7 13.2 84.0 81.9 14.6 2.2 0.597 0.705 • 45.4 51.1 144.9 15.5 95.0 87.4 9.9 2.0 0.655 0.737