Download

1 / 24

240 likes | 252 Views

Learn about corporation tax regulations in Ireland, including tax charges, permanent establishment criteria, company residence tests, and exemptions, covering worldwide profits, capital gains, and more.

E N D

Corporation Tax Corporation Tax • A company pays corporation tax on total profits. • Total profits include all taxable income earned by the company and capital gains arising on the disposal of capital assets.

Corporation Tax The Charge to Corporation Tax • A company resident in Ireland is subject to corporation tax on its worldwide profits • A non-resident company operating in Ireland through a permanent establishment is subject to corporation tax on income earned by the PE and gains arising from assets situated in Ireland or used for the purposes of carrying on a trade through an Irish PE.

Corporation Tax The Charge to Corporation Tax • A non-resident company that does not have a PE in Ireland will be subject to income tax (not CT) on Irish source income, and subject to CGT (not CT) on gains arising on specified assets. • A non-resident company with an Irish PE, disposing of assets unrelated to the trade of the PE, will be subject to CGT on the disposal

Corporation Tax A permanent establishment • Ireland – UK Double Tax Treaty • ‘a fixed place of business in which the business of the enterprise is wholly or partly carried on’

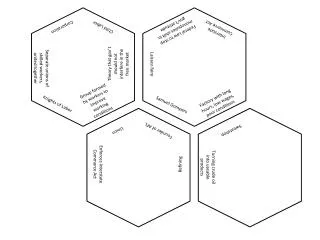

Corporation Tax A permanent establishment • A permanent establishment includes: • ‘a place of management; • a branch; • an office; • a factory; • a workshop;

Corporation Tax A permanent establishment • A permanent establishment includes: • a mine, oil well, quarry or other place of extraction of natural resources; • an installation or structure used for the exploration of natural resources; • a building site or construction or installation project which lasts for more than six months.’

Corporation Tax A permanent establishment • A permanent establishment does not include: • the use of facilities solely for the purpose of storage, display or delivery of goods or merchandise belonging to the enterprise; • the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of storage, display or delivery;

Corporation Tax A permanent establishment • A permanent establishment does not include: • the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of processing by another enterprise; • the maintenance of a fixed place of business solely for the purpose of purchasing goods or merchandise, or for collecting information, for the enterprise;

Corporation Tax A permanent establishment • A permanent establishment does not include: • the maintenance of a fixed place of business solely for the purpose of advertising, for the supply of information, for scientific research or for similar activities which have a preparatory or auxiliary character, for the enterprise.

Corporation Tax A permanent establishment • A person who has the power to conclude contracts (other than the purchase of goods and merchandised) on behalf of the non-resident company is a PE • Offshore exploration or exploitation is deemed to be a PE • Carrying on business through an independent broker or agent does not constitute a PE

Corporation Tax A permanent establishment • A company controlled by a non-resident company does not constitute a PE of the non-resident company

Corporation Tax Company Residence • Two tests are applied to determine the residence status of a company: • The statutory test, and • The central management and control test

Corporation Tax Company Residence – the statutory test • A company is resident in Ireland if it is incorporated in Ireland. • There are two exceptions to this rule: • The Trading Exemption • The Treaty Exemption

Corporation Tax Company Residence – the statutory test • The Trading Exemption applies to a company carrying on a trade in Ireland, and • Is ultimately controlled by person(s) resident in an EU member state or in a country that Ireland has a Double Tax Treaty with, or • The company or a related company is a quoted company

Corporation Tax Company Residence – the statutory test • Generally, a company is controlled by person(s) owning more than 50% of the share capital/voting rights or entitled to more than 50% of the distribution of income/assets on winding up.

Corporation Tax Company Residence – the statutory test • The Treaty exemption applies to a company that is not regarded as resident in the State under the provisions of a Double Tax Treaty. • Double Tax Treaties set out the rules to determine the main country in which a company will be liable to pay tax and aims to reduce the effect of double taxation.

Corporation Tax Company Residence • If a company is not resident in Ireland by virtue of the statutory test, it can still be resident under the central management and control test

Corporation Tax Company Residence – the central management and control test • Not in legislation but developed through case law. • Relates to the strategic control of the company • Factors to be considered: • Where are directors’ meetings held? • Where do the majority of directors reside?

Corporation Tax Company Residence – the central management and control test • Factors to be considered: • Where are the shareholders’ meetings held? • Where is the negotiation of major contracts undertaken? • Where are the questions of important policy determined? • Where is the head office of the company?

Corporation Tax Company Residence – the central management and control test • Factors to be considered: • Where are the books of account kept? • Where are the accounts prepared and examined? • Where are the accounts audited? • Where are the minute books kept? • Where is the company seal kept?

Corporation Tax Company Residence – the central management and control test • Factors to be considered: • Where is the share register kept? • From where are dividends declared? • Where are the profits realised? • Where are the company’s bank accounts?

Corporation Tax Company Residence – For Companies Incorporated on or after 1 January 2015 • Two tests are applied to determine the residence status of a company: • The statutory test, and • The central management and control test

Corporation Tax Company Residence – the statutory test • A company is resident in Ireland if it is incorporated in Ireland. • There is one exception to this rule: • The Treaty Exemption • The trading exemption does not apply for companies incorporated after 31 December 2014

Corporation Tax Company Residence – For all Irish Incorporated Companies from 1 January 2021 • All Irish incorporated companies will be tax resident in Ireland