Download

1 / 14

160 likes | 338 Views

Balanced Scorecard Fundamentals. Measuring Strategic Performance Dr. Shayne Tracy. Why Use the Balanced Scorecard?.

E N D

Balanced Scorecard Fundamentals Measuring Strategic Performance Dr. Shayne Tracy

Why Use the Balanced Scorecard? • To maintain sustainable competitive advantage in the information age, strategic business units must broaden their base of intangible assets and the means by which performance is measured and continuously improved. • The balanced scorecard provides a comprehensive framework for implementing strategic plans by translating an organization’s strategy into a set of key performance indicators.

Performance Measures Yesterday • Traditional measures of performance only included financial statistics based on the financial accounting model. External FOCUS Non Financial MEASURES Internal Financial Historical Future TIMEFRAME

Performance Indicators Today • The balanced scorecard focuses on an integrated system of key performance indicators for critical success factors. Non Financial MEASURES External Financial FOCUS Internal Historical Future TIMEFRAME

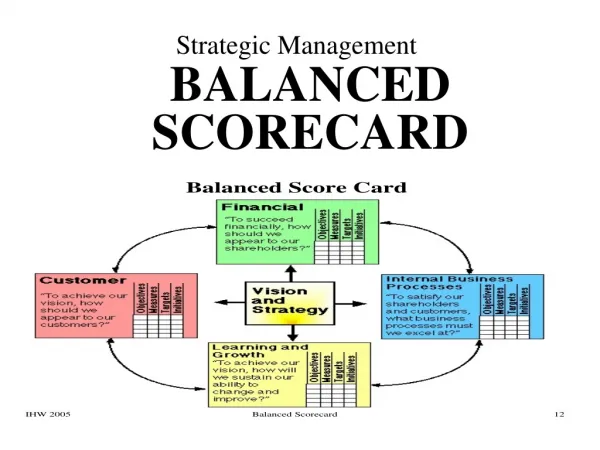

The Balanced Scorecard Dimensions Financial Perspective Customer Perspective Internal Processes Vision, Values Mission, Strategy Learning & Growth

The Financial Perspective • To succeed financially, what level of financial performance do our investors expect? Examples: • ROI, EVA • Return on capital employed (ROCE) • Revenue growth • Self-financiable growth rate • Cash flow return on assets • Market/customer/product profitability growth

The Customer Perspective • To achieve our strategy, how must we appear to our customers? Examples: • Market share growth • Customer acquisition rate • Customer retention rate • Customer satisfaction scores • Number of new products/services • Product return rate • Defect rate • On-time delivery rate

Internal Business Processes • At what business processes must we excel to satisfy our clients/customers? Examples: • Product-development cycle time • Order-to-delivery response time • Six sigma (PPM) quality rate • Revenue per employee • Cash conversion cycle time • New product/service introduction rate • New product/service breakeven time

Learning & Growth Perspective • What people and systems do we need to sustain our ability to change and improve? Examples: • Employee retention/turnover rate • Salaries/wage index • Training/development hours per employee • Strategic competency index • Value-added per employee dollar • Sustainable growth analysis • Knowledge productivity rate

Economy is concerned with inputs only Effectiveness refers to the achievement of objectives Productivity is the ratio of outputs to inputs Performance is the quality of tasks and activities total number of labour hours worked during the period total number of good units of output for the period number of good units of output per labour hour of input Number of “0” defects per unit of output per labour hour Economy, Effectiveness, Productivity and Performance

Balanced Scorecard Workflow • Strategic Plan • Gap Analysis • Implementation of Action Plans • Recalibration Annually

Balanced Scorecard Planning and Implementation Workflow ENSURE SENIOR MANAGEMENT COMMITMENT Identify strategic business units to be measured Identify and prioritize BSC perspectives Identify customers of BSC and their requirements Articulate strategy and mission Define critical success factors Determine data gathering methods Determine source of benchmark / target data Eliminate redundant indicators Define relevant performance indicators w/CAR Gather benchmark and actual data Estimate future attainable performance Identify causes of current and future gaps Determine current performance gap Align incentives and compensation with BSC performance indicators Gain constituency acceptance of conclusions Establish performance goals and objectives Implement initiatives Assess progress toward goals Revise goals, if necessary Validate/update benchmarks Periodic Reappraisal Communication and consensus at each is critical

Communication Tools • Check sheets/lists • Goal/Objective Action Plans • Project/Process Plans • Cause and effect diagrams • Histograms, Pareto diagrams • Control charts • Scatter diagrams, Bar charts

Resources • Frigo, Mark L., & Krumwiede, Kip R. (2000, January). "The Balanced Scorecard: A Winning Performance Measurement System," Strategic Finance. 50-54. • The Society of Management Accountants of Canada. Applying the Balanced Scorecard, Strategic Management Series, Management Accounting Guideline. (1999). Mississauga, ON Canada: Author. • Institute of Management Accountants. Statements on Management Accounting 4DD, Tools and Techniques for Implementing Integrated Performance Management Systems. 1998. Montvale, NJ: Author. • Harvard Business School Press. Harvard Business Review on Measuring Corporate Performance. 1998. Boston, MA: Author. • Chee W. Chow, Kamal M. Haddad, & James E. Williamson. (1997, August). “Applying the Balanced Scorecard to Small Companies”, Management Accounting. 21 – 27. • Robert S. Kaplan, David P. Norton. 1996. The Balanced Scorecard Boston, MA: Harvard Business School Press. • Institute of Management Accountants. Statements on Management Accounting 4U, Developing Comprehensive Performance Indicators. 1995. Montvale, NJ: Author.