Download

1 / 14

140 likes | 291 Views

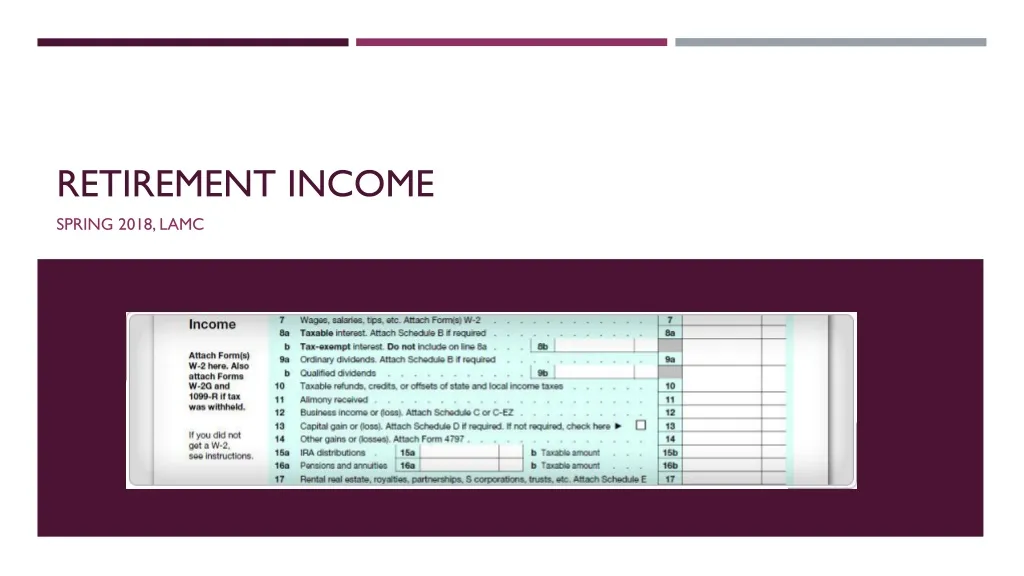

Retirement income. Spring 2018, lamc. Introduction. Retirement Income can be: Social Security benefits Annuity benefits Retirement or profit sharing plans Insurance contracts IRA May be fully or partially taxable. Refer to Publication 4012, Tab D (D-33 et al.) Forms 1099-R Series

E N D

Retirement income Spring 2018, lamc

Introduction • Retirement Income can be: • Social Security benefits • Annuity benefits • Retirement or profit sharing plans • Insurance contracts • IRA • May be fully or partially taxable. • Refer to Publication 4012, Tab D (D-33 et al.) • Forms 1099-R Series • Form 1099-R, Distributions from Pensions, Annuities, Retirement or Profit Sharing Plans, IRAs, Insurance Contracts, etc. • Form CSA 1099R, Statement of Annuity Paid (civil service retirement payments) • Form CSF 1099-R, Statement of Survivor Annuity Paid, and • Form RRB 1099-R, Annuities or Pensions by the Railroad • Retirement Board

Introduction • Our VITA site can only complete the return if the taxable amount is indicated on the Form. If it not indicated, we will need to refer to a VITA site with Advanced certification. • Taxpayers with Form RRB-1099-R can only be helped by Advanced certified volunteers because the taxable portion is not shown on the return. • Retirement plans are funded by either before-tax or after-tax contributions. • Before-tax definition: • Employee did not pay taxes on the money at the time it was contributed (no cost basis in plan). • After-tax definition: • Employee paid taxes on the money when it was contributed (has cost basis in the plan). • If taxpayer made all contributions to a plan with before-tax dollars, the entire distribution will be fully taxable. The funds are taxed at the time of the distribution. • This is a common 401(k) and Thrift Savings Plan.

Introduction • If taxpayer made contributions with after-tax dollars, then distributions are partially taxable. • The portion of the distribution that is considered a return of the after-tax dollars will not be taxed (cost basis) • Only the earnings/investment gains will be taxed. • The chart below explains the taxation of retirement income.

Individual retirement arrangements (IRA) income • IRA distributions are reported on Form 1099-R. • Four types of IRAs: • Traditional IRA • Roth IRA • Savings Incentive Match Plans for Employees (SIMPLE) IRA • Simplified Employee Pension (SEP) IRA • Traditional IRA • Fully taxable unless nondeductible contributions have been made. • Refer taxpayers with nondeductible contributions to a professional tax preparer. • Roth IRA • Distributions from a Roth IRA are tax free and may be excluded from income if certain requirements are met. • Refer to Publication 4012, Tab D (D-40) to determine if distribution is a qualified distribution.

IRA Income • Nonqualified Distributions • If the requirements of the Roth IRA are not met, the distribution is nonqualified and additional taxes may apply. • Taxpayers should be referred to professional tax preparer. • Qualified Distributions • The IRA trustee will indicate distribution is qualified by using Code Q in box 7. • Entire distribution is not taxable. • SIMPLE IRA • Employers that offer employees chance to contribute part of their pay to IRA as part of SIMPLE plan. • Generally, contributions are not included in an employee’s income when paid into an IRA and distributions are fully taxable. • SEP IRA • Employers that offer employees chance to contribute part of their pay to IRA as part of SEP plan. • Generally, SEP contributions are not included in an employee’s income when paid into an IRA. • Distributions are generally fully taxable. • What is the difference between distributions from a Roth IRA and a traditional IRA? • Roth IRA distributions are generally tax-free, because the contributions were after-tax. • Traditional IRA distributions may be fully or partially taxable, because the contributions may have been deductible or non-deductible. • You can identify ROTH IRAs from the distribution code used on Form 1099-R. Only Code Q is in the scope for the VITA programs.

Examples Refer to Publication 4012, Tab D (D-40) • Lily opened a Roth IRA 4 years ago. This year, she took the full amount of her Roth IRA as a distribution to help her purchase her first home. The entire distribution is excluded from her income. • True • False • Anna contributed to a Roth IRA for 5 years. In year 6 (at age 60) she took a distribution from her IRA. The entire distribution is excluded from her taxable income. • True • False

rollovers • Generally, a rollover is a tax-free distribution to the taxpayer from one retirement account that rolls over into another qualified retirement account within 60 days. • If the distribution was a direct rollover by one institution to another institution, the distribution code is G. • A ROTH IRA account rollover is distribution code H.

Fully Taxable pension and annuities • Reported on Form 1099-R (distribution box is unchecked), Form CSA 1099-R and Form RRB 1099-R. • Generally, pension or annuity payments are fully taxable if: • Taxpayers did not pay any part of the cost of their pensions or annuities • Employers did not withhold part of the cost from the taxpayers’ pay while they worked • Employers withheld part of the cost from the taxpayer’s before-tax pay while they worked. • Ex.: Nancy worked for a company for 20 years. She retired and began receiving pension income the same year. She never contributed to the pension plan while she was working. Her employer made all the contributions. Her pension is fully taxable.

Partially taxable pensions and annuities • Two methods are used: • General Rule (this is out of scope and we must refer to professional tax preparer) • Simplified Method • Information needed to calculate taxable portion using the Simplified Method: • The cost in the plan (total employee contribution on Form 1099-R) • Taxpayer’s age on the date the annuity began (and spouse’s age if joint/survivor annuity is selected) • Total of tax-free amounts from previous years, available from the taxpayer’s prior year worksheet. • Simplified Method Formula • Taxpayer’s cost basis / Number of monthly payments = monthly Tax-Free Portion

Example • Derek worked for the local hardware company for 30 years. He retired in June and receives a monthly pension of $1,679 (He received six payments from July through December). Derek never contributed to the pension plan; his employer made all the contributions. How much of his pension is taxable? • $12,074 • $11,074 • $10,074 • $1,679

Disability pension income • Generally, taxpayers who retire on disability must include of their disability payments in income. • Disability payments are taxed as wages until the taxpayer reaches the minimum retirement age (age set by employer). • After the minimum retirement age, the disability payments are treated as pension income to determine taxability. • Employers may report disability income on following forms: • Form W-2: if taxpayer has not reached minimum retirement age • Form 1099-R: if taxpayer has reached minimum retirement age.

Other retirement income issues • Premature Distributions • Early withdrawal from a retirement account for purposes other than retirement by a taxpayer who is under 59 ½ • Early distributions are subject to an additional 10% tax. • Minimum Distributions • To avoid an additional tax, participants in retirement plans must begin making a Required Minimum Distribution (RMD) by a specific date. • That date is April 1 of the calendar year following the year in which the taxpayer either reached 70 1/2 , or retired whichever is later. • For IRAs it does not matter whether the taxpayer has retired. • These rules do not apply to Roth IRAs. • After the starting year for the RMDs, taxpayers must receive the minimum distribution for each year by December 31 of that year.

Example • Martha turned 70 ½ on March 18, 2015. She retired in 2004. She has never taken any distribution from her traditional IRA accounts. The bank told her that she needs to take a minimum distribution of $1,479 per year. Martha is required to: • Take a distribution of $1,479 by December 31, 2015. • Take a distribution of $1,479 by April 1, 2015, and another $1,479 by December 31, 2015. • Take a distribution of $2,958 by December 31, 2015. • Take a distribution of $1,479 by April 1, 2016, and another $1,479 by December 31, 2016.