Download

1 / 22

220 likes | 298 Views

Financial Literacy Programs and Minority Participation. Presented by: Torell T. Pernell Chicago State University. Minorities and Money. Minorities do not bank, buy insurance or invest in stocks in the same way as white Americans.

E N D

Financial Literacy Programs andMinority Participation Presented by: Torell T. Pernell Chicago State University

Minorities and Money • Minorities do not bank, buy insurance or invest in stocks in the same way as white Americans. • Less than half of all Hispanics have credit cards compared to 80 percent of the population. • Only 57 percent of middle-class African Americans have money invested in the stock market as opposed to 81 percent of whites. • About 58 percent of Hispanic households had savings or checking accounts compared with 71 percent of black families and 93 percent of white households. • Women continue to have less income in retirement than men do. Source: M. Lee, MBA , National Economic Council

The need for more minority financial literacy • African American adults were less likely than Caucasian adults to have learned personal finance information from school. • African American and Hispanic adults are significantly more likely than Caucasian adults to express concerns with assorted financial challenges • African American and Hispanic adults, significantly more than their white counterparts, strongly agree that they could use answers to everyday financial questions from a professional. Source: Consumer Financial Literacy Survey (2011).

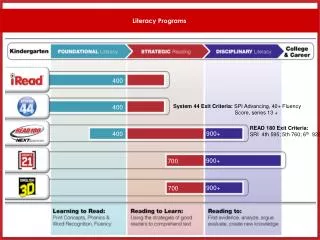

Participation by income and gender, 2012 Vanguard defined contribution plans permitting employee-elective deferrals. Annual IncomeFemale Male All <$30,000 51% 43% 46% $30,000–$49,999 70 58 63 $50,000–$74,999 78 62 67 $75,000–$99,999 85 74 77 $100,000+ 87 88 87 Source: Vanguard Capital, 2013.

Participation by income and gender, Vanguard Capital Management 2012

Average Account Balance by Salary (2007 Source: The Ariel / Hewitt Fund

Research objectives • Understand the concepts of financial education • Analyze the design of financial education programs • Discover current financial education initiatives • Analyze the effect and progress of such initiatives

Why is financial education important? • What is “financial education?” • What financial education initiatives are underway? • Are they working and how do we know?

Why is financial education important? ProsCons • More savings • More investments • Less debt • Homeownership • Bank accounts • 401(k), pension • Higher credit score • Less savings • Less investments • High debt • Low-income group • High prepaid cards fees • Lack of 401(k), pension • Lower credit score Source: Lerman and Bell, 2006.

What is “financial education?” • being knowledgeable, educated, and informed on the issues of managing money and assets, banking, investments, credit, insurance, and taxes • understanding the basic concepts underlying the management of money and assets (e.g., the time value of money in investments and the pooling of risks in insurance) • using that knowledge and understanding to plan, implement, and evaluate financial decisions. Source: J. Hogarth, Federal Reserve (2006).

What are financial literacy programs? • Intended to increase financial awareness and improve financial behaviors • Provides individuals with the knowledge, aptitude, and skills necessary to become questioning and informed consumers of financial services

Designing Effective Financial Literacy Programs • The topics • The audience • Learning styles • Behavior stage Source: J. Hogarth, Federal Reserve (2006).

Components of financial literacy programs • Budgeting • Credit / Fico scores • Credit cards • Saving and investing • Student loan repayment Source: Nelnet Loan Servicing

Are financial education programs working and how do we know? • Some have shown positive results • Some have shown minimal results • Some have shown no results • Evaluations are based on: • Current and past financial education knowledge • Current and past behaviors in managing personal finances • Knowledge and attitudes • Behaviors and outcomes • how much money has been saved? • how much debt has been reduced? • how much money has been invested? Source: Jump$tart Coalition

Determining success Effective programs need: • Measurable goals • Appropriate and realistic formatting • Information • Experience-based content • Student involvement • Financial literacy should be pervasive theme Source: Nelnet Loan Servicing

Potential contributors to financial education • Non-profits • Credit counseling services • Centers for economic and financial education • Local foundations • Financial services sector • Local/state/national government agencies • US Treasury

Does Financial Literacy Work? • Research shows that financial education does not necessarily lead to behavioral changes in personal money management • Skill-building and motivation are two other issues that must be considered when providing financial education • Automatic investment programs and governmental tax incentives also help to provide motivation and to contribute to behavioral changes • Cultural, economic, and environmental conditions play a significant role in shaping the everyday financial choices of individuals Source: Journal of Financial Counseling and Planning, 2009.

Financial Education Resources • Governmental agencies • U.S. Federal Reserve Board • Illinois Department of Labor • U.S. Treasury’s Office of Financial Education • U.S. Census Bureau • U.S. Department of Labor • Private financial institutions • Bank of America • American Bankers Association • Ariel Mutual Fund • The Institute on Assets and Social Policy • The Urban Institute

Looking Ahead • Our goal is to learn much more about the outcomes and impacts that financial education has on individuals and their communities • The Federal Reserve Board is beginning a project that consists of a longitudinal evaluation of their own financial education program • More financial institutions will develop and support financial literacy initiatives.

Existing programs • University of North Texas - Student Money Management Center • Web site, resources for students and parents • www.moneymanagement.unt.edu • Kansas State University - Power Cat Financial Counseling • Recognized by the White House as a model program • www.k-state.edu/pfc,https://www.facebook.com/kstatepfc • University of Texas - Bevonomics • short courses are conducted • www.bevonomics.org

References • Braunstein, Sandra and Welch, Carolyn. “Financial Literacy: An Overview of Practice, Research, and Policy.” Federal Reserve Bulletin, Nov 2006. • Gale, William G., Harris, Benjamin H., and Levine, Ruth. “Raising Household Saving.” Social Security Bulletin, Vol. 72, No. 2, 2012. • Harnisch, Thomas L. “Boosting Financial Literacy in America.” Perspectives, Fall 2010. • Hogarth, Jeanne M. “Financial Education and Economic Development. “ Federal Reserve Board, Nov 2006. • Lee, Michael D. “Minorities and Money.” • Lerman, Robert I. and Bell, Elizabeth. “Can Financial Literacy Enhance Asset Building?” The Urban Institute, Sep 2005. • Lerman, Robert I. and Bell, Elizabeth. “Financial Literacy Strategies: Where Do We Go From Here?” The Urban Institute, Aug 2006. • Lusardi, Annamaria. “Financial Education and the Saving Behavior of African-American and Hispanic Households.” Dartmouth College, Department of Economics, Sep 2005. • Mandell, Lewis Ph.D. “The Financial Literacy of Young Adults.” JumpStart Coalition, 2008. • Mandell, Lewis and Klein, Schmid Klein, Linda. “The Impact of Financial Literacy Education on Subsequent Financial Behavior.” Journal of Financial Counseling and Planning, Volume 20, Issue 1, 2009. • National Strategy 2011. “Promoting Financial Success in the United States.” Financial Literacy and Education Commission, 2011.

Thank you! Torell T. Pernell Chicago State University