Download

1 / 16

320 likes | 1.03k Views

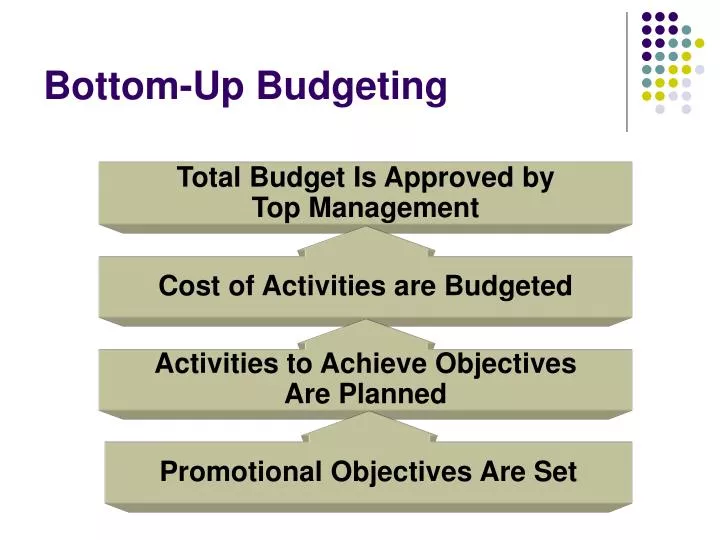

Total Budget Is Approved by Top Management. Cost of Activities are Budgeted. Activities to Achieve Objectives Are Planned. Promotional Objectives Are Set. Bottom-Up Budgeting. Bottom-Up Budgeting. Objective and Task Method Payout Planning Quantitative Models. Objective and Task Method.

E N D

Total Budget Is Approved by Top Management Cost of Activities are Budgeted Activities to Achieve Objectives Are Planned Promotional Objectives Are Set Bottom-Up Budgeting

Bottom-Up Budgeting • Objective and Task Method • Payout Planning • Quantitative Models

Objective and Task Method • It looks at the objectives for each activity and determines the cost of accomplishing each objectives. • Three steps: • Defining the communications objectives to be accomplished • Determining the specific strategies and tasks need to attain them • Estimating the cost associated with performance of these strategies and tasks

Establish Objectives (create awareness of new product among 20 percent of target market) Determine Specific Tasks (advertise on market area television and radio and local newspapers) Estimate Costs Associated with Tasks (television, $575,000; radio, $225,000; newspaper, $175,000) Objective and Task Method

Objective and Task Method • The major of advantage of this method is that the budget is driven by the objectives to be attained. • The major disadvantage of this method is the difficulty of determining which tasks will be requires and the costs associated with each. • This method is not as easy to perform or as stable as some of the methods discussed earlier. • It is especially difficult for new product introduction (There is no past experience to use as a guide).

Payout Planning • The first months of a new product’s introduction typically require heavier-than-normal advertising and promotion appropriations to stimulate higher levels of awareness and subsequent trial. • The average share of advertising to sales ratio necessary to launch a new product successfully is approximately 1.5~2.0. • This means that a new entry should be spending at approximately twice the desired market share. • Figure 7-20

Payout Planning • The basic idea is to project the revenues the product will generate, as well as the costs it will incur, over 2 to 3 years. • Based on an expected rate of return, the payout plan will assist in determining how much advertising and promotions expenditure will be necessary when return might be expected.

To determine how much to spend, marketers develop a payoutplan that determines the investment value of the advertising and promotion appropriation Example of a three-year payout plan ($ millions) Year 1 Year 2 Year 3 Product sales 15.0 35.50 60.75 Profit contribution (@$.50 per case) 7.5 17.75 30.38 Advertising/promotions 15.0 10.50 8.50 Profit (loss) (7.5) 7.25 21.88 Cumulative profit (loss) (7.5) (0.25) 21.63 Payout Planning

Quantitative Models • For the most part, these methods employ computer simulation models involving statistical techniques such as multiple regression analysis to determine the relative contribution of the advertising budget to sales. • Attempts to apply quantitative models to budgeting have met with limited success. • Such methods do have merit but may need more refinement before achieving widespread success.

Allocating the Budget • Allocating to IMC elements • Client/agency policies • Market size • Market potential • Market share goals • Economics of scale in advertising • Organizational characteristics

Decrease–find a defensible niche Increase to defend High Competitor’s Share of Voice Attack with large SOV premium Maintain modest spending premium Low Low High Your Share of Market Share of Voice Effect