Download

1 / 20

200 likes | 325 Views

Banca CR Firenze Lino Moscatelli Managing Director. Setting the Agenda for 2010. Merrill Lynch Banking & Insurance CEO Conference 2005 London, 4 - 6 October 2005. Table of Contents. Where we are at the end of the 2003-2005 Plan Future Opportunities. Banca CR Firenze Group Structure.

E N D

Banca CR FirenzeLino MoscatelliManaging Director Setting the Agenda for 2010 Merrill Lynch Banking & Insurance CEO Conference 2005 London, 4 - 6 October 2005

Table of Contents • Where we are at the end of the 2003-2005 Plan • Future Opportunities

Banca CR Firenze Group Structure Retail Banking Assets Management Tax Collection IT Services Consumer credit & Financial Services Full perimeter of consolidation Banca CR Firenze Findomestic 50% 100% 60% 51% Infogroup CR Pistoia Centrovita 51% 80% 100% CRF Gestion Int Citylife CR Civitavecchia 37,5% Centro Leasing 73,6% 100% Cerit CR Orvieto 47,7% Centro Factoring 68,1% 68,1% SRT CR Spezia 99,9% CR Mirandola

Consolidated Key Figures for 1994-2004 (*) Total financial assets Net loans to customers 33.847 21.812 12.491 Total Income Net income (*) 2004 data on a proforma basis and including Findomestic consolidated at equity

EPS Cost/Income Actual Business Plan Actual Business Plan 2004 Resuls vs Targets • Achieved growth in overall profitability • EPS at 9 cents/Euro, ahead of target • Cost / Income at 66%, ahead of target. Ample room for further improvement

The Italian macroeconomic scenario • Italian growth prospects remain uncertain • Banks P&Ls remain sound, but may be affected by: • Growing indebtedness of small enterprises • Non banking players competing in funding and treasury management • Families tending to reduce the number of bank accounts • Banks’ approach too focused on selling rather than on clients’ expectations

Our Strategic Guidelines • Internal network expansion • Service quality • Improvement of customer satisfaction • Development of new businesses • Further efficiency improvement • Group integration Multi-channel architecture Growth Quality of relation Cost control

Expected results New branches New customers Growth Profit increase

As at 30/6/2005 Network & Percentage of Territorial Coverage 518 branches in all Verona 1 Mantova 8 Reggio Emilia 1 Parma 2 Bologna 8 Modena 18 La Spezia 51 Pistoia 53 Prato 15 Massa-Carrara 18 Florence 137 Lucca 22 Pisa 13 Leghorn 9 Perugia19 Arezzo 35 Siena 19 Terni 23 Grosseto 16 Financial advisors Number of branches per 100,000 inhabitants Viterbo14 Region Branches % < 1 Tuscany 337 65% Liguria 51 10% Rome 36 1 < = 5 Latium 50 10% Umbria 42 8% 5 <= 15 Emilia Romagna 29 6% Lombardy 8 2% > 15 Veneto 1 0% Total 518 100%

Expected results New branches New customers Profit increase New procedures Better management of current customers Profit increase Quality of relations

Commercial Position: IndividualsBusiness Areas High growth potential Pension schemes Only potential for selective investments to improve service quality and maintain market shares Consumer credit Business Growth Mortgages Personal insurances Investments Potential for further investments to improve the bank’s position and exploit good growth ratios Cash - payments Bank’s Positioning Note: The dimension of the bubble shows the current importance of the Business Area in terms of margins

Commercial Position: “SMEs & Corporates” (≥2.5 M€ Turnover)Business Areas Corporate = 2% of customers and 6% of total loans Selective investments to follow the opportunities offered by our market Internationalization serv. Structured finance Ind.& Spec. credit Financial risk coverage Bank guarantees Maintain market shares Foreign payables/ receivables Investments to exploit the expected growth of high margin products Business Growth Factoring1 Agriculture Financing Leasing1 Domestic payables/ receivables Currencies Bank’s Positioning The dimension of the bubbles shows the current importance of the Business Area in terms of margins 1) Seeking to increase commercial consistency with the product companies

Expected results New branches New customers New procedures Better management of current customers Profit increase Streamlining Efficiency improvement Profit increase Cost control

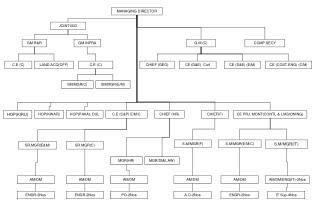

Current Organization Model Network/Total Employees Current Target 3,464 employees (3,387 net, excludes intercompany staff) CRF XX,X% CENTRALIZED SERVICES 69,8% XX,X% CRP CRO CRC CRM CRS 621 employees 170 employees 218 employees 189 employees 518 employees 83,7% 77,1% 83,0% 73,0% 76,3% 90,0% 85,0% 85,0% 85,0% 90,0%

Expected results New branches New customers Multi-channel architecture New procedures Better management of current customers Streamlining Efficiency improvement Profit increase IT investments New services Low prices New organization Branch staff reduction Profit increase

ATM - Internet - GSM PDA - Digital TV Common interface Common services Bank 1 Bank 2 Bank n Teller SW Teller SW Teller SW Bank SW Bank SW Bank SW Group SW Group SW Group SW Management & Regulatory reporting Management & Regulatory reporting Management & Regulatory reporting IT SystemCurrent applications architecture

ATM - Internet GSM - PDA Digital TV Common Interface Bank 1 SW Bank 2 SW Bank n SW Data Integration Middleware Group SW Management & Regulatory Reporting Costs control - ICT Management streamlining Teller SW Common Services

ATM - Internet GSM - PDA Digital TV Common Interface Multi-channel architecture Teller SW Cost reduction Better service to customers Branches freed from low value activities

Expected retirement • A large number of employees will reach the minimal age for retirement and may leave the company between 2006-2008 150 Parent Company’s Headquarters 25 Other Banks’ Headquarters 250 Parent Company’sNetwork 25 Other Banks’ Network

Expected retirement Retirement Replacement Replacement Technology Headcount reduction Organization