Download

1 / 25

250 likes | 384 Views

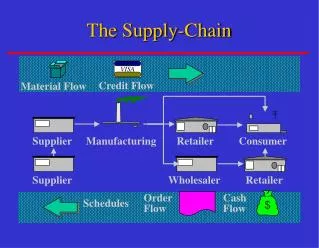

Supply Chain Changes A manufacturer’s perspective. Mike Isles Andy Carr. MPI Associates Limited. Andrew Carr Associates Ltd. Two high level supply chain models. DTP. Reduced wholesaler. More accurately DTC ie “Direct to Customer” channel Retail Pharmacists Hospitals Dispensing Doctors

E N D

Supply Chain ChangesA manufacturer’s perspective Mike Isles Andy Carr

Two high level supply chain models DTP Reduced wholesaler • More accurately DTC • ie “Direct to Customer” channel • Retail Pharmacists • Hospitals • Dispensing Doctors • Selling to: • 14,000 customers (from eg 14) • Using “partners” to perform a range of distribution services • Sell product to a small number of wholesalers • Ownership of stock is still with wholesalers • Risks and rewards still owned by wholesalers • Commercial relationship with “customers” not owned by manufacturer • Downstream discounts determined by wholesalers There are benefits of both to manufacturers

Supply Chain – Traditional method Manufacturer Control Outside Manufacturer Control ? % 12.5% disc ?% Manufacturer pre-wholesaler / own warehouse ~14 Wholesalers Patient Pharmacy ?% margin clawback Department of Health

Supply Chain – Reduced wholesaling Manufacturer Control Outside Manufacturer Control ? % ?% disc ?% Manufacturer pre-wholesaler / own warehouse 2-3 Wholesalers Patient Pharmacy ?% margin clawback Department of Health

Supply Chain – DTP Manufacturer Control Outside Manufacturer Control ? % Man. terms Manufacturer pre-wholesaler / own warehouse Agents/LSP Patient Pharmacy clawback Control & ownership move further down the Supply Chain Department of Health

Manufacturers’ supply chain activity DTP Reduced Wholesalers • Pfizer (03/07) (U) • Astellas*(11/07) (U) • AstraZeneca (02/08) (A,U) • GSK (11/08) (A,U) • Lilly(07/09)(A,P) • Napp(10/07) (A,P,U) • sanofi aventis (11/07) (A,P,U) • Novartis (08/08) (A,U) • Roche (01/09) (A,U) • Janssen-Cilag(01/09) (A,P,U) • Novo Nordisk (03/09) (P,U) • UCB* (11/09)(A,P,U) • S & N (06/09) (A,P,U) • Bayer Schering(07/09)(A,P,U) • BMS(08/09) (A,U) • MSD (10/09) (A,P,U) • LEO Pharma (10/09) (A,P,U) A – AAH Pharmaceuticals Ltd P – Phoenix Healthcare Distribution U – Alliance Healthcare (Distribution) (Unichem) * Product specific arrangements

Manufacturers’ supply chain partners A & U A & P P & U A, P, U U • Pfizer (03/07) • Astellas*(11/07) • GSK (11/08) • AstraZeneca (02/08) • Novartis (08/08) • Roche (01/09) • BMS(08/09) • Lilly(07/09) • Novo Nordisk (03/09) • Napp(10/07) • sanofi aventis (11/07) • Janssen-Cilag(01/09) • S & N (06/09) • Bayer Schering(07/09) • MSD(10/09) • LEO Pharma (10/09) • UCB (11/09) A – AAH Pharmaceuticals Ltd P – Phoenix Healthcare Distribution U – Alliance Healthcare (Distribution) (Unichem) DTP programs * Product specific arrangements

PPRS – direct impact on prices PPRS price reductions 1993 – 2.5% 1999 – 4.5% 2005 – 7.5% 2009 – 3.9% 2010 – 1.9% Manufacturers have seen an 18% reduction in the price of their medicines over 18 years, with a large patent expiry cliff-edge approaching in forthcoming years

PPRS – impact of price cuts Pharma Manufacturers are exploring all avenues to mitigate the impact of price cuts

Partnership approach Simplification, focus, opportunities Opportunities Opportunities Supply partners Supply partners

Increased visibility • Getting closer to the point of medicine delivery brings the following benefits for manufacturers: • End–to-end supply chain visibility • Reduction of product wastage • Commercial relationships with end contractors (pharmacists/D Doctors) • Reliable information on who is buying product • Management of increased demand

Supply Chain ChangesA manufacturer’s perspective Mike Isles Andy Carr