Download

1 / 10

0 likes | 10 Views

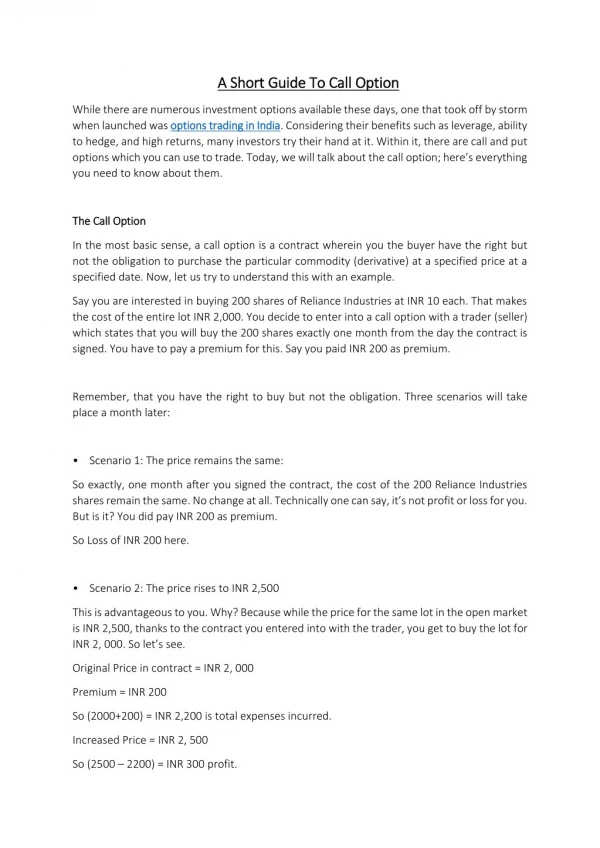

Option trading is a popular way of speculating on the movements of the stock market. Options are contracts that give the buyer the right, but not the obligation, to buy or sell an underlying asset at a specified price and time. Options can be used for various purposes, such as hedging, income generation, or speculation.<br><br>One of the most common option strategies is the straddle, which involves buying or selling both a call and a put option of the same strike price and expiry. A straddle can be either long or short, depending on whether the trader buys or sells the options.

E N D

SAMCODIKHAYE AAPHIKE TAJURBEKA #ANDEKHASACH Takiaapbanebehtartrader

Content Introduction Delta Gamma Theta Vega

The Greeks are the parameters that measure the sensitivity of the option price to various factors, such as the price of the underlying asset, the volatility of the underlying asset, the time to expiry, and the interest rate. The main Greeks that affect the bearish straddle strategy are delta, gamma, theta, and vega. Introduction

Delta measures the change in the option price with respect to the change in the underlying asset price. A positive delta means the option price will increase when the underlying asset price increases, and vice versa. A negative delta means the option price will decrease when the underlying asset price increases, and vice versa. Delta

Gamma measures the change in the delta with respect to the change in the underlying asset price. Gamma

Theta measures the change in the option price with respect to the change in the time to expiry. A negative theta means the option price will decrease as the time to expiry decreases, and vice versa. Theta

Vega measures the change in the option price with respect to the change in the volatility of the underlying asset. A positive vega means the option price will increase when the volatility of the underlying asset increases, and vice versa. Vega

ThankYou SamcoSecuritiesLimited-1004 – AWing,10thFloor,NamanMidtown, Senapati BapatMarg,Prabhadevi,Mumbai-400 013. Calluson: 9122227777/ 02245030450 Visitusat: www.Samco.in