Download

1 / 51

510 likes | 636 Views

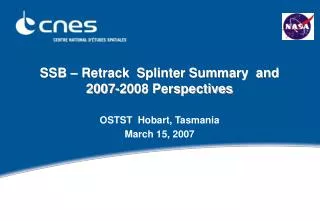

Banorte Investor Day. Strategy and Perspectives for 2008. November 15, 2007. Contents. Results Overview for 2007 Asset Quality Industry Trends Outlook for 2008 Final Remarks. 1. Results Overview for 2007. 11%. 24%. 23%. YTD Financial Recap. CONSTANT MILLION PESOS. 9M 06. 9M 07.

E N D

Banorte Investor Day Strategy and Perspectives for 2008 November 15, 2007

Contents • Results Overview for 2007 • Asset Quality • Industry Trends • Outlook for 2008 • Final Remarks

11% 24% 23% YTD Financial Recap CONSTANT MILLION PESOS 9M06 9M07 4,548 5,044 Net Income 11% 25% 23% ROE Tax Rate 38% 34% Net Interest Margin 7.8% 7.4% Performing Loan Growth 29% 23% Past Due Loan Ratio 1.5% 1.6% Stock Price 42.92 34.66 Book Value 15.71 12.78 P/BV 2.71 2.73

Comparable Results CONSTANT MILLION PESOS 9M06 2007 accounting standards 9M07 Net Interest Income 10,547 12,301 17% Non Interest Income 5,198 5,887 13% Total Income 15,745 18,188 16% Non Operating Expense 9,521 10,422 9%

Efficiency is moving towards our medium term target of low 50’s. Efficiency Ratio 76% 59% 57% 57% Accounting + Investments 55% 53% Sep‘07 2006 2004 2005 2003

Net Income CONSTANT MILLION PESOS • Recurrent profits continue to improve on a yearly basis. Non Recurring 5,044 4,838 4,548 Recurring 4,748 4,122 1,871 CAGR 39% 9M07 9M06 9M04 9M05

Net Interest Margin vs CETES PERCENTAGE • Average NIM for 2007 and 2008 should be close to 7.5%. Average CETE: 9M05: 9.39% 9M06: 7.25% 9M07: 7.13% CETES 9.5 8.6 87% 8.0 7.9 NIM 8.5 7.7 7.7 7.6 8.3 7.5 7.1 107% 7.5 7.1 7.2 7.1 7.0 7.0 7.0 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07

Evolution of Loans & Deposits • The current Loans to Total Deposits ratio is less than 85%. Performing Loan Portfolio (YoY) Core Deposits (YoY) 29% 23% 22% 20% 17% 12% 8% 3% 3Q04 3Q05 3Q06 3Q07 3Q04 3Q05 3Q06 3Q07

18% 16% 28% 16% 17% 20% 10% 11% 7% Core Deposits CONSTANT BILLION PESOS YoY Change w/o INB 3Q05 3Q06 3Q07 Deposits Demand 70 82 95 42 48 61 Time Total 112 130 156 Mix 63% 63% 61% Demand Time 37% 37% 39% 100% 100% 100%

25% 23% Performing Loan Portfolio CONSTANT BILLION PESOS 173 165 134 3Q06 2Q07 3Q07 Change YoY w/o Extras 3Q06 2Q07 3Q07 QoQ YoY Consumer 50 55 58 6% 17% 48 63 67 5% 39% Commercial 23 30 30 (1%) 32% Corporate 13 17 18 4% 32% Government Total 134 165 173 5% 29%

23% 25% Performing Consumer Loan Portfolio CONSTANT BILLION PESOS 58 55 50 3Q06 2Q07 3Q07 YoY Change w/o Extras Change 3Q06 2Q07 3Q07 QoQ YoY 30 31 33 6% 10% Mortgage 6 7 7 1% 6% Car Loans 9 12 13 7% 45% Credit Card Payroll Loans 5 6 6 6% 24% 50 55 58 6% 17% Consumer

Transformation of the Loan Book 2001 2007 Consumer 2% Government 10% Mortgage 6% Consumer 15% Commercial & Corporate 23% Mortgage 19% Commercial & Corporate 56% Government & Fobaproa 69%

Evolution of Savings in Mexico 2001 2007 Brokerage 21% Brokerage 20% Deposits 42% Deposits 54% AFORE + Insurance 28% AFORE + Insurance 21% Mutual Funds 8% Mutual Funds 12% Source: Banco de México, CNBV and SHCP

Evolution of Credit in Mexico 2007 2001 Consumer 29% Consumer 12% Government 9% Government 18% Mortgage 12% Mortgage 14% Corporate 67% Corporate 39% Source: Banco de México, CNBV and SHCP

Infrastructure 9M06 9M07 Distribution network Branches 978 1,023 5% ATM’s 3,033 3,513 16% 40% POS’s 19,050 26,627 Employees 15,410 12% 17,218

Footprint Expansion (Branches) 1,023 960 459 456 1998 2001 2004 Sep‘07

Assets under Management CONSTANT BILLION PESOS 581 550 55 53 430 Long Term Savings 183 37 171 130 Brokerage 343 326 263 Bank 2004 Sep‘07 2006

Customers MILLIONS 12.2 12.2 10.3 2.4 2.4 3.4 3.7 Insurance 2.7 3.2 3.4 3.2 Afore 5.6 5.1 4 4 Bank 4.4 2004 Sep‘07 2006

Asset Quality CONSTANT BILLION PESOS 3Q06 2Q07 3Q07 Total Loan Portfolio 137 169 176 Past Due Loans 2.2 2.5 2.7 Loan Loss Reserves 3.7 3.6 3.6 PAST DUE LOAN RATIO RESERVE COVERAGE 1.6% 172% 1.5% 1.5% 141% 132% 3Q06 2Q07 3Q07 3Q06 2Q07 3Q07

Past Due Loan Ratio 5.8% 5.4% 2.0% 1.5% 1998 2001 2004 2007

Credit Cards PDL Ratio vs. Industry Sep’06 Sep’07 6.3% 5.1% 4.6% 3.7% Banorte Other Major Banks Banorte Other Major Banks Source: Asociación de Bancos de México (ABM)

Mortgage Loans PDL Ratio vs. Industry Sep’06 Sep’07 3.3% 2.9% 2.5% 2.4% Banorte Other Major Banks Banorte Other Major Banks Source: Asociación de Bancos de México (ABM)

Mortgage Loans • Conservative origination policies • Formal economy • Low LTV of loan book 52% • House value > 300,000 pesos • Adequate payment mechanisms • Transparency in terms and conditions

Sep’07 Sep’06 Branch Network Industry growth: +7% 1,801 1,730 1,541 +4% 1,451 1,359 1,347 +6% 1,022 +1% 977 960 914 +5% +5% 504 425 +18% Bancomer Banamex HSBC Banorte Santander Scotiabank • Banorte 2007e = 1,046. Source: Asociación de Bancos de México (ABM)

Sep’07 Sep’06 ATM Network Industry growth: +11% 5,947 5,161 5,542 4,731 +7% 5,618 +9% 5,353 +5% 3,837 3,513 3,321 +16% 3,036 +16% 1,257 1,122 +12% Bancomer Banamex HSBC Santander Banorte Scotiabank • Banorte 2007e = 3,669. Source: Asociación de Bancos de México (ABM)

Cost-Weighted Core Deposits Market share BBVA 32% 29% 25% Banamex 24% HSBC 17% 16% 12% Banorte Santander 12% 12% 10% Scotiabank 6% 5% Source: Internal calculations with data from Asociación de Bancos de México (ABM)

Cost-Weighted Core Deposits Growth Sep‘06 – Sep‘07 16% 6% Market Banorte Source: Internal calculations with data from Asociación de Bancos de México (ABM)

Performing Loans Market share 34% BBVA 31% Banamex 23% 20% Santander 15% 14% Banorte 13% 13% 12% 10% Scotiabank 9% HSBC 7% Source: Asociación de Bancos de México (ABM)

Performing Loans Growth Sep‘06 – Sep‘07 29% 28% Market Banorte Source: Asociación de Bancos de México (ABM)

Mortgages Market share 45% BBVA 34% 25% Banamex Banorte 14% 14% 12% 11% Scotiabank 10% HSBC 9% 9% Santander 8% 8% Source: Asociación de Bancos de México (ABM)

Consumer Loans Market share 34% 31% BBVA Banamex 26% 25% 17% 15% Santander HSBC 13% 11% 9% Banorte 8% 7% Scotiabank 5% Source: Asociación de Bancos de México (ABM)

Credit Card Outstandings Growth Sep‘06 – Sep‘07 46% 31% Market Banorte Source: Asociación de Bancos de México (ABM)

Government + Corporate Loans Market share BBVA 31% 30% Banamex 21% 21% Santander 17% 17% Banorte 15% 13% HSBC 12% 10% Scotiabank 7% 5% Source: Asociación de Bancos de México (ABM)

Government Loans Growth Sep‘06 – Sep‘07 40% Market Banorte (3%) Source: Asociación de Bancos de México (ABM)

Sep‘07 Sep‘06 Past Due Loan Ratio Industry Average: 2.4% 3.4% 2.8% 2.6% 2.6% 2.5% 2.5% 2.2% 2.1% 1.6% 1.5% 1.5% 0.9% HSBC Scotiabank Banamex Bancomer Banorte Santander Source: Asociación de Bancos de México (ABM)

Sep‘07 Sep‘06 Reserve Coverage Ratio 204 199 184 181 172 163 153 153 148 145 132 -24 124 Bancomer Santander Banamex Banorte HSBC Scotiabank Source: Asociación de Bancos de México (ABM)

Progress of 2007 Initiatives Expansion of Distribution Network • Plan: 29 new and 41 renovations • Actual: 52 new and 18 renovations • From 172,000 to 1.5 million cards in the last 3 years • Annual growth of 50% in outstandings Ramp-up of Credit Card Platform Re-focus Long Term Savings business • New fees in AFORE: Growth • Change in management Bancarization of lower income segments • Entry level deposit products • Remittances • Offshore deposits • Cross-border mortgages Integration of Banorte USA

Challenges 2008 • Low correlation between banking sector and economic growth • Balance between growth, asset quality and profitability • Execution of infrastructure expansion program • Greater focus on deposits and fee income • Explore alternate channels

2008 Initiatives • 50 new branches + 50 renovations • 600 ATM’s • Investment: US $45 million Distribution Network • Heavily under-banked • Next secular growth story Emphasis on SME’s • Emphasis on asset quality • Overhaul of business model Micro-lending business • Alternate channels • Broaden customer base Deepen Bancarization • New markets / products • Organic growth Banorte USA

Outlook for 2008 • Loan growth: +22% - 24% • Average NIM: 7.5% • Efficiency ratio: below 55% • Net income: Ps $8.0 billion • EPS growth: +18% - 19% • ROE: +/- 22%

Medium Term Strategies • Take the fullest advantage of growth opportunities in the Mexican Financial Sector: • Innovating • Developing competitive products • Penetrating new markets • Investing intelligently In talent In infrastructure

Medium Term Strategies • Alert to a more dynamic & competitive environment: • Old and new forces • Client loyalty and retention • New income segments • Alternate distribution channels

Medium Term Strategies • Maintain 20/20 vision: • Focus on core earnings • Efficiency • Emphasis on asset quality • Balanced funding • Robust capitalization Positive operating leverage Cost containment

Certain statements in this document are “forward-looking statements”. These statements are based on management’s current expectations and are subject to uncertainty and changes in circumstances. Actual results may differ materially from those included in these statements due to a variety of factors.