Download

1 / 153

1.56k likes | 2.38k Views

Chapter 12 Bond Prices and the Importance of Duration. Outline. Introduction Review of bond principles Bond pricing and returns Bond risk The meaning of bond diversification Choosing bonds Example: monthly retirement income. Introduction.

E N D

Outline • Introduction • Review of bond principles • Bond pricing and returns • Bond risk • The meaning of bond diversification • Choosing bonds • Example: monthly retirement income

Introduction • The investment characteristics of bonds range completely across the risk/return spectrum • As part of a portfolio, bonds provide both stability and income • Capital appreciation is not usually a motive for acquiring bonds

Review of Bond Principles • Identification of bonds • Classification of bonds • Terms of repayment • Bond cash flows • Convertible bonds • Registration

Identification of Bonds • A bond is identified by: • The issuer • The coupon • The maturity • For example, five IBM “eights of 10” means $5,000 par IBM bonds with an 8% coupon rate and maturing in 2010

Classification of Bonds • Introduction • Issuer • Security • Term

Introduction • The bond indenture describes the details of a bond issue: • Description of the loan • Terms of repayment • Collateral • Protective covenants • Default provisions

Issuer • Bonds can be classified by the nature of the organizations initially selling them: • Corporation • Federal, state, and local governments • Government agencies • Foreign corporations or governments

Definition • The security of a bond refers to what backs the bond (what collateral reduces the risk of the loan)

Unsecured Debt • Governments: • Full faith and credit issues (general obligation issues) is government debt without specific assets pledged against it • E.g., U.S. Treasury bills, notes, and bonds

Unsecured Debt (cont’d) • Corporations: • Debentures are signature loans backed by the good name of the company • Subordinated debentures are paid off after original debentures

Secured Debt • Municipalities issue: • Revenue bonds • Interest and principal are repaid from revenue generated by the project financed by the bond • Assessment bonds • Benefit a specific group of people, who pay an assessment to help pay principal and interest

Secured Debt (cont’d) • Corporations issue: • Mortgages • Well-known securities that use land and buildings as collateral • Collateral trust bonds • Backed by other securities • Equipment trust certificates • Backed by physical assets

Term • The term is the original life of the debt security • Short-term securities have a term of one year or less • Intermediate-term securities have terms ranging from one year to ten years • Long-term securities have terms longer than ten years

Terms of Repayment • Interest only • Sinking fund • Balloon • Income bonds

Interest Only • Periodic payments are entirely interest • The principal amount of the loan is repaid at maturity

Sinking Fund • A sinking fund requires the establishment of a cash reserve for the ultimate repayment of the bond principal • The borrower can: • Set aside a potion of the principal amount of the debt each year • Call a certain number of bonds each year

Balloon • Balloon loans partially amortize the debt with each payment but repay the bulk of the principal at the end of the life of the debt • Most balloon loans are not marketable

Income Bonds • Income bonds pay interest only if the firm earns it • For example, an income bond may be issued to finance an income-producing project

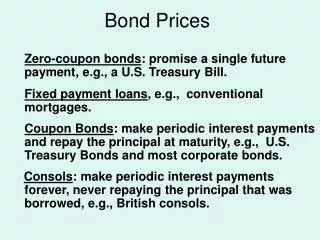

Bond Cash Flows • Annuities • Zero coupon bonds • Variable rate bonds • Consols

Annuities • An annuity promises a fixed amount on a regular periodic schedule for a finite length of time • Most bonds are annuities plus an ultimate repayment of principal

Zero Coupon Bonds • A zero coupon bond has a specific maturity date when it returns the bond principal • A zero coupon bond pays no periodic income • The only cash inflow is the par value at maturity

Variable Rate Bonds • Variable rate bonds allow the rate to fluctuate in accordance with a market index • For example, U.S. Series EE savings bonds

Consols • Consols pay a level rate of interest perpetually: • The bond never matures • The income stream lasts forever • Consols are not very prevalent in the U.S.

Definition • A convertible bond gives the bondholder the right to exchange them for another security or for some physical asset • Once conversion occurs, the holder cannot elect to reconvert and regain the original debt security

Security-Backed Bonds • Security-backed convertible bonds are convertible into other securities • Typically common stock of the company that issued the bonds • Occasionally preferred stock of the issuing firm, common stock of another firm, or shares in a subsidiary company

Commodity-Backed Bonds • Commodity-backed bonds are convertible into a tangible asset • For example, silver or gold

Bearer Bonds • Bearer bonds: • Do not have the name of the bondholder printed on them • Belong to whoever legally holds them • Are also called coupon bonds • The bond contains coupons that must be clipped • Are no longer issued in the U.S.

Registered Bonds • Registered bonds show the bondholder’s name • Registered bondholders receive interest checks in the mail from the issuer

Book Entry Bonds • The U.S. Treasury and some corporation issue bonds in book entry form only • Holders do not take actual delivery of the bond • Potential holders can: • Open an account through the Treasury Direct System at a Federal Reserve Bank • Purchase a bond through a broker

Bond Pricing and Returns • Introduction • Valuation equations • Yield to maturity • Realized compound yield • Current yield • Term structure of interest rates • Spot rates

Bond Pricing and Returns (cont’d) • The conversion feature • The matter of accrued interest

Introduction • The current price of a bond is the market’s estimation of what the expected cash flows are worth in today’s dollars • There is a relationship between: • The current bond price • The bond’s promised future cash flows • The riskiness of the cash flows

Valuation equations • Annuities • Zero coupon bonds • Variable rate bonds • Consols

Annuities • For a semiannual bond:

Annuities (cont’d) • Separating interest and principal components:

Annuities (cont’d) Example A bond currently sells for $870, pays $70 per year (Paid semiannually), and has a par value of $1,000. The bond has a term to maturity of ten years. What is the yield to maturity?

Annuities (cont’d) Example (cont’d) Solution: Using a financial calculator and the following input provides the solution: N = 20 PV = $870 PMT = $35 FV = $1,000 CPT I = 4.50 This bond’s yield to maturity is 4.50% x 2 = 9.00%.

Zero Coupon Bonds • For a zero-coupon bond (annual and semiannual compounding):

Zero Coupon Bonds (cont’d) Example A zero coupon bond has a par value of $1,000 and currently sells for $400. The term to maturity is twenty years. What is the yield to maturity (assume semiannual compounding)?

Zero Coupon Bonds (cont’d) Example (cont’d) Solution:

Variable Rate Bonds • The valuation equation must allow for variable cash flows • You cannot determine the precise present value of the cash flows because they are unknown:

Consols • Consols are perpetuities:

Consols (cont’d) Example A consol is selling for $900 and pays $60 annually in perpetuity. What is this consol’s rate of return?

Consols (cont’d) Example (cont’d) Solution:

Yield to Maturity • Yield to maturity captures the total return from an investment • Includes income • Includes capital gains/losses • The yield to maturity is equivalent to the internal rate of return in corporate finance

Realized Compound Yield • The effective annual yield is useful to compare bonds to investments generating income on a different time schedule