Download

1 / 11

470 likes | 1.16k Views

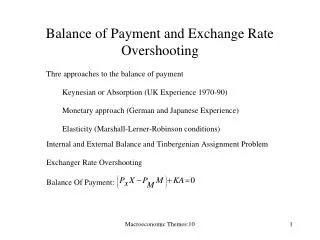

Supplementary slides in International Macroeconomics & Finance. Exchange Rate Overshooting Dornbusch (1976) JPE. Jarir Ajluni - July 2005. Time. Meaning of Overshooting.

E N D

Supplementary slides in International Macroeconomics & Finance Exchange Rate Overshooting Dornbusch (1976) JPE Jarir Ajluni - July 2005

Time Meaning of Overshooting Traditional and monetarists views suggest that after a monetary expansion, prices rise, interest rates falls and consequently the exchange rate is to depreciate (increase), Dornbusch Keynesian sticky-price model show that of the exchange rate would depreciate and ‘Overshoot’ in depreciation then appreciate slowly back to the new equilibrium. b c a In Dornbusch model, due to expectations and price rigidity the adjustment would take the form of excessive depreciation far beyond the equilibrium level, the exchange rate ‘jumps’ from a to point b Then the exchange rate does not jump from a to c directly, instead it first ‘overshoots’ to b then slowly appreciates to the new equilibrium level in the Long Run.

Expected rate of depreciation The Expected rate of depreciation is proportional to discrepancy between Long-Run and current exchange rate e, the adjustment is measured by theta : • Consistent with Rational Expectations Hypothesis REH. • Model development based on expectations, sticky prices & capital mobility. • Model is drawn on the different speeds of adjustments of the goods and asset (financial) markets that adjust more rapidly. • Assumes perfect asset substitution between domestic and foreign markets. Basic Facts of the Model I. Capital Mobility and Expectations

II. The Money Market Typical money market equilibrium is given in the log transformation: combining (1),(2),(3) with manipulation, an expression linking the spot exchange rate as a function of current price level and the equilibrium price level, equation (4) is a key equation in the model. III. The Goods Market Domestic Output demanded (D) is given by:

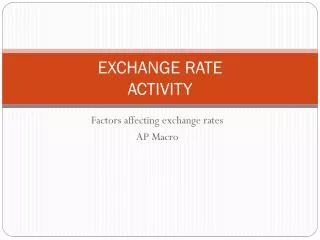

p Q Q 45° e IV. The Equilibrium Exchange Rate Negative relationship between prices and spot exchange rate, for any given price level, exchange rate adjust to maintain equilibrium; hence the QQ curve. a The positively sloped line show a set of combinations of p, e where both goods & markets are in equilibrium. b At initial point b prices are lower than equilibrium & exchange rate is in excess of the Long Run equilibrium, the path of rising prices is accompanied by exchange rate appreciation to its equilibrium @ a

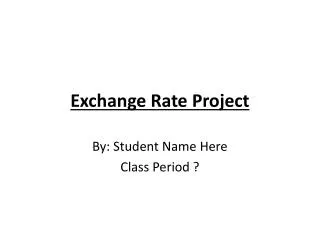

Q' p Q Q' Q 45° e Effects of monetary expansion An increase in nominal quantity of money would cause disequilibrium, this should be matched with either increased prices or with exchange rate depreciation. c Since Prices are sticky, and the asset market adjust rapidly comparing with the goods market, the exchange rate would depreciate (increase) to point b and QQ shifts –proportionately- to the right. a b Exchange rate depreciate until the Short-Run equilibrium b where this depreciation is enough to anticipate appreciation to compensate the reduction in interest rate after “overshooting” to b,The exchange rate appreciates to the new Long-Run equilibrium at point c. e' e''

P M Time Time Time Time R e Effects of monetary expansion

Concluding Remarks • Exchange rates exhibit Overshooting in depreciation before appreciating to equilibrium. • The extent of overshooting depends on Expectations and the response of the interest rate.

Dornbusch, Rudiger (1976), “Expectations and Exchange Rate Dynamics”, Journal of Political Economy, 84(6) pp 1161-77 • Hallwood, P and MacDonald, R. (2000) “ International Money and Finance”, 3rd edition References