Download

1 / 9

90 likes | 179 Views

CDM Portfolio update. Jane Ellis (OECD). AIXG seminar, 21 March 2005. Outline. Institutional developments Update on proposed CDM project activities Status of proposed CDM project activities Funding for CDM/JI Common sticking points. Institutional developments.

E N D

CDM Portfolio update Jane Ellis (OECD) AIXG seminar, 21 March 2005

Outline • Institutional developments • Update on proposed CDM project activities • Status of proposed CDM project activities • Funding for CDM/JI • Common sticking points

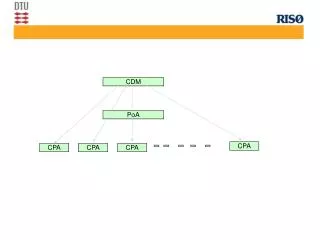

Institutional developments • Growth in Designated National Authorities continuing • 75 DNAs established to date (59 in Non-Annex I Parties, 16 in Annex I Parties/EC) • More baseline/monitoring methodologies approved: • 21 EB-approved methodologies in highly diverse areas • 2 “consolidated” methods: renewable electricity, landfills • 14 small-scale methodologies • … and lots more in the pipeline: • 19 new submissions, 9 submissions not yet examined, 5 in “feedback loop”, a few awaiting input from MP or others • “Unilateral” projects eligible to generate CERs

Proposed CDM project activities • Data based on 284 • proposed projects • in 51 countries (up • from 201 in Nov 04) • Expected mitigation • 69.7 Mt CO2-eq/y • in 2008-2012 and • 119Mt pre-2008 • Does not include • projects withdrawn

Rapidly changing portfolio… • Portfolio (incl. proposed projects) dominated by projects reducing high-GWP waste gases • Some of these projects are very large • (1-10 million credits/year) • Declining importance of • renewables • (21%) • Energy eff. • small • Sinks 4% • Small CCS • project Mar 05, 70 Mt/y Feb 04, 27 Mt/y

Geographical spread uneven • Early dominance by L. America, then Asia • Africa (7%) and AOSIS (3%) small • Handful of countries dominate proposed CDM portfolio: • Korea, 17% of credits (2 projects) • India, 16% of credits (43 projects) • Brazil, 12% of credits (38 projects) • Mexico, 12% of credits (21 projects) • China, 7% of credits (13 projects) • Indonesia, 5% of credits (12 projects) • These countries also received half of FDI flows in 2002

Status of proposed CDM projects • 4 CDM projects registered • (1 landfill gas, 1 small hydro, 2 HFC23 reduction) • 3 further requests for registration under review • 91 projects requesting validation could generate 13.5 Mt CO2-eq/y in 2008-2012 • 53 more projects have submitted their baseline methodology to CDM EB • Approved methods could generate a further 13.5 Mt CO2-eq/y in 2008-2012 (when applied to projects that have not yet requested validation)

Funding available for CDM/JI • US$1.7bn available from several different sources, e.g.: • private, national and international carbon funds, • national JI/CDM programmes, • other government programmes • …mainly public sector, focused on buying credits (rather than funding projects), not all disbursed yet • Does not include investment needed to implement actual projects • Total investment much larger …. but difficult to quantify • World Bank largest player in credit market: >$850m

Common sticking points • Low C price => limited push for CO2 reducing projects • Transaction costs: very variable, but significant, and reduce interest in “smaller” (<50,000 CER/year) projects • No market signal post-2012 • Lead-time for project development much lower for “brownfield projects” • Additionality: difficult to put into practice • Methodology approval can be time-consuming (3 months at best, but can be 6-9 months or longer)