Download

1 / 12

120 likes | 295 Views

Rating Contingent Credit Default Swap Internal Trade Review. Stanley Securities September 23, 2010 David Lin Shengbao Luo Casey Wang George Wang Peilin Zhang. Agenda. Valuation & Calibration Market Risk Hedging Model Risk P&L. Valuation Overview. Discount factors

E N D

Rating Contingent Credit Default SwapInternal Trade Review Stanley Securities September 23, 2010 David Lin ShengbaoLuo Casey Wang George Wang Peilin Zhang

Agenda • Valuation & Calibration • Market Risk • Hedging • Model Risk • P&L

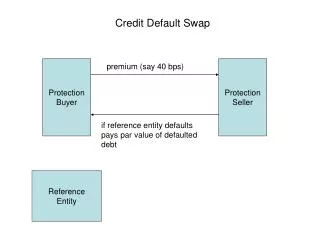

Valuation Overview • Discount factors • Pricing default contingent cash flows with hazard rate process • Hazard rate model calibration and parameter selection • Spot FX modeling and FX Forward payoff valuation • Downgrade threshold determination

Pricing Default Contingent Cash Flows PV at time t: And continue backwards, or:

Hazard Rate Process Calibration Calculation parameters • Calibrated parameters: h0, θ • Fixed parameters: α, v(ht,t) Simulation Parameters • Time step • Number of paths

Hazard Rate Calibration Cont. Model Parameters:

Downgrade threshold 0.012

Hedging Dynamic delta hedging as part of the credit hybrids portfolio • UJB credit risk • FX delta • IR PV01 • Cross partials

Model Risk • Reduce-form model • OU hazard rate process: • rate can be negative, and can be different from the real process • Model assumptions: • alpha, sigma, ratings downgrade hazard rate • Coarseness of time steps • Knock in knock out between steps

How much $ will we make? • Fair market value: $1.34MM • Offer market value: $1.60MM • Day one hedging cost: $32K • Day one P&L: $228K