Download

1 / 43

1.21k likes | 3.78k Views

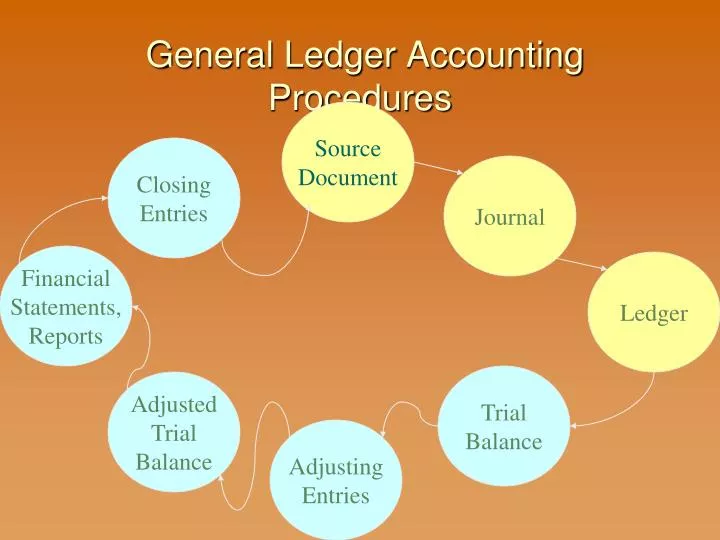

General Ledger Accounting Procedures. Source Document. Closing Entries. Journal. Financial Statements, Reports. Ledger. Trial Balance. Adjusted Trial Balance. Adjusting Entries. Source Documents. Examples: sales order, Bill of Lading (shipping notice), sales invoice

E N D

General Ledger Accounting Procedures Source Document Closing Entries Journal Financial Statements, Reports Ledger Trial Balance Adjusted Trial Balance Adjusting Entries

Source Documents • Examples: • sales order, Bill of Lading (shipping notice), sales invoice • Purchase requisition, purchase order, receiving report, vendor invoice, check • Contract, time card, check

Source Document Journal • Journal: Book of original entry • Transaction analysis (debit, credit what?) • General journal vs. Special journals • Efficiency • Typical Special Journals: • Sales • Cash Receipts • Cash Payments • Purchases • Payroll

General Journal SAMPLE

Sales journal: Credit Sales & credit Returns Cash Receipts journal: any cash receipt (Sales, AR, Other) Source Document ________________________ Purchase journal: Credit purchases or credit Purchase Returns of inventory, supplies, PPE POST Source Document to ONE AND ONLY ONE Journal!!! Cash Payments journal: any Cash Payment except for Payroll Payroll journal: any paycheck General journal

Source Document Journals General Ledger • Ledger: Separate record for each account • Cash, Accounts Receivable, …Sales, Cost of Goods Sold • Balance Sheet/ Income Statement Order • Posting: transferring data from journal to ledger • Total journal at end of month and post total to Ledger account

Sample Ledger Cards SAMPLE Note that totals are posted from journals

Posting: Journal to Ledger SAMPLE At EOM, Foot and cross-foot journals, post totals to ledgers General Ledger

Posting: Journal to Ledger SAMPLE Post to GL account 30200 General Ledger

Post from General Journal to General Ledger SAMPLE Note that line entries are posted from the GENERAL JOURNAL

General Ledger : Subsidiary and Control • Control Accounts =GL ACCOUNT • Aggregate • Column total posting from journals • Subsidiary Ledger • Detail • AR, AP, Employee, Fixed Assets • Line item posting from journals • Sum of the subsidiary (all records) = Control

Post Journal Lines to Subsidiary At the time of the transaction

Posting: Journal to Ledger SAMPLE At EOM, Foot and cross-foot journals, post totals to ledgers General Ledger

General Ledger Trial Balance Trial Balance: sum of each account in the ledger Assures Debits = Credit Assures Accounts summed correctly But could have offsetting errors

Trial Balance due for each SUA Assignment SAMPLE SAMPLE

SUA Assignments • “S” Transactions: due for SUA #1 • SALES Journal transactions • But may have exceptions • “CR” Transactions: Due for SUA #2 • Cash Receipts Journal transactions • But may have exceptions • “P” Transactions: DUE for SUA #3 • Purchase Journal • Exceptions

SUA Assignments • ‘CD” Transactions: due for SUA #4 • Cash Disbursements (Cash Payments) Journal • But may have exceptions • “PR” Transactions: Due for SUA #5 • Payroll Journal • But may have exceptions • SUA #6 Year end, adjustments, closing, financials

Process Record transaction on source document Copy key data elements from source document to Journal at time of transaction. Copy data elements from journal to Sudsidiary Ledger At EOM, total journal columns and crossfoot. Copy totals to appropriate General Ledger Account

General Ledger Trial Balance Trial Balance: sum of each account in the ledger Debits = Credit Accounts summed correctly Could have offsetting errors Pull a trial balance every time you post from a journal

General Ledger Accounting Procedures Source Document Journal Ledger Subsidiary Ledger Trial Balance ACG 306

Transaction List (Green) • Document Symbol: • Complete the appropriate documents and record in Journal • No documents are used for this type of transaction; record in the appropriate journal • Documents are not required by you. Record in the appropriate journal. • Mark each transaction as S (#1), CR (#2), P (#3) ,CD (#4), PR (#5), YE (#6) YES NO NO

Received customer PO#ST3107 (document #4) in the mail from Clayburn University, approved their credit and shipped the goods. All goods ordered were shipped, except that only 45 shoulder pad sets were available for shipment. 45

Sales Journal xx xx

AR Subsidiary Ledger XXX XXX