Download

1 / 2

30 likes | 367 Views

Example Exchange Arbitrage. You have access to the following three spot exchange rates: $0.01/yen, $0.20/krone, 25yen/krone. You start with dollars and want to end up with dollars.

E N D

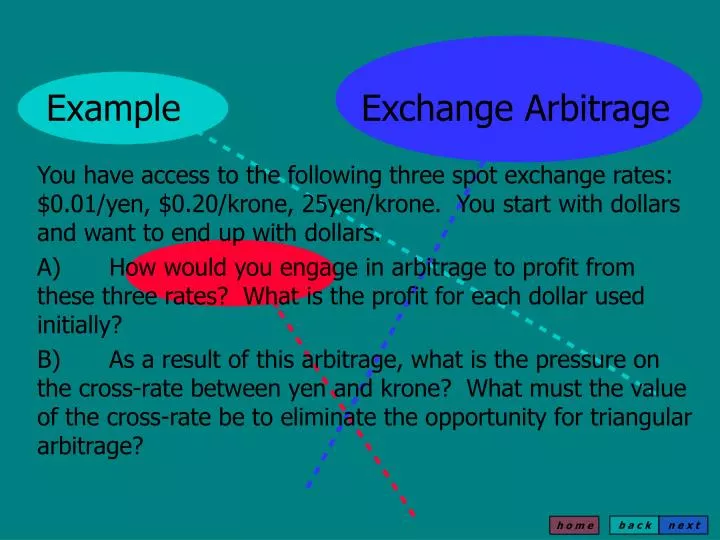

Example Exchange Arbitrage You have access to the following three spot exchange rates: $0.01/yen, $0.20/krone, 25yen/krone. You start with dollars and want to end up with dollars. A) How would you engage in arbitrage to profit from these three rates? What is the profit for each dollar used initially? B) As a result of this arbitrage, what is the pressure on the cross-rate between yen and krone? What must the value of the cross-rate be to eliminate the opportunity for triangular arbitrage?

Solution A) dollars ----> krone ----> yen ----> dollars $1 / 0.2 * 25 * 0.01 = $1.25 Profit = $0.25 B) Selling krone to buy yen puts downward pressure on the cross rate (the yen price of krone). The value of the cross rate must fall to 20yen/krone to eliminate the opportunity for triangular arbitrage.