Download

1 / 48

500 likes | 613 Views

Basics of Fraud. Northern Arizona University December, 2010. Quotes from the Field. “All the internal auditors I have talked to in large organizations have told me that employee frauds increased substantially during the recessionary years of 2008 and 2009.” - Tony Bishop, Director

E N D

Basics of Fraud Northern Arizona University December, 2010

Quotes from the Field “All the internal auditors I have talked to in large organizations have told me that employee frauds increased substantially during the recessionary years of 2008 and 2009.” - Tony Bishop, Director Deloitte Forensic Center

Quotes from the Field “The percentage of allegations of fraudulent activity has more than doubled over the past four years.” -The Network Corporate Governance and Compliance Hotline Benchmarking Report

Quotes from the Field “Many organizations seem to have moved into firefighting mode, where people do only what they consider essential. The risk is skimping on fraud prevention and detection activities today may create opportunities for catastrophic frauds tomorrow.” - Tony Bishop, Director Deloitte Forensic Center

What Will We Cover? What is fraud? Fraud triangle/diamond Who commits fraud? Fraud facts Types of fraud Detection Red flags How organizations encourages fraud Lowering the risk of fraud Roles in fraud prevention and detection What to do if you suspect fraud

What is Fraud? The Association of Certified Fraud Examiners (ACFE) defines the term “occupational fraud” as: The use of one’s occupation for personal enrichment through the deliberate misuse or misapplication of the employing organization’s resources or assets.

What is Fraud? • What does that really mean? The intentional and wrongful obtainment of a benefit through: • Theft or embezzlement • False statements (documents, grants, applications) • Corruption, kickback, conspiracies, collusion, bribes • Misappropriation of assets (travel expenses, payroll, equipment)

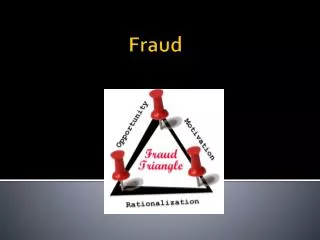

Fraud Triangle Opportunity Rationalization Pressure

Fraud Triangle - Pressure • Pressure is the motive for committing fraud. • Lifestyle • Personal debt (debt, financial losses, gambling, drugs) • Illness • Job dissatisfaction

Fraud Triangle - Rationalization • Rationalization is the justification to make their actions consistent with their personal code of conduct. • “I’m only borrowing the money – I’ll pay it back.” • “Everyone does it.” • “I’m not hurting anyone.” • “It’s for a good purpose.” • “It’s not that big of a deal.” • “They owe me. I should be paid more.”

Fraud Triangle - Opportunity • Opportunity is the situation that allows fraud to occur in the first place. • A lack of or inadequate internal controls • Separation of duties • Supervision and review • Management approval • Technology controls • Inability to judge the quality of the work of others • Form over function • Management ignorance or apathy • Focus on “higher priorities”

Fraud Diamond Opportunity Rationalization Capability Pressure

Fraud Diamond • Capability is the knowledge to commit the fraud. • Confidence to execute the fraud without getting caught. • Will know the weaknesses in “the system.” • Recognizes the opportunity and can turn it into reality. • Thrill or risk seeking behavior.

Who Commits Fraud? • How many employees… • Will? • Might? • Won’t?

Who Commits Fraud? WILL 30% WON’T 40% MIGHT 30% Source: EideBailly/ACFE

Who Commits Fraud? “The vast majority of people who end up stealing from an organization had no intention of doing so when they went to work or began contracting relationships there but loyalty diminishes in tough times, especially after widespread layoffs and contracting cutbacks, thereby creating a ‘high-fraud environment.’” - James Ratley, President Assoc. Certified Fraud Examiners

Who Commits Fraud? Compared to other property offenders, fraudsters… • Have better psychological health • Exhibit more: Source: Fraud Examination by W. Steve Albrecht

Who Commits Fraud? • How often? How much? • Male or Female? • Employee, manager or executive? • Age? • Length of service? • Criminal background? • Employment background?

Who Commits Fraud? NOTE: Percentages equal at “employee” level but more predominantly male in “manager” and “owner/exec” levels.

Who Commits Fraud? $80K $200K $723K

Who Commits Fraud? $124K $268K $44K $359K $974K

Who Commits Fraud? $114K $289K $231K $47K

Facts about Fraud Typical organization loses 5% of revenue. Median duration is 18 months before detection. Asset misappropriation is most common at 90% but least costly with median loss of 21% of total dollars lost or $135,000. Occupational fraud usually detected by tip. Small organizations have a higher rate of victimization.

Facts about Fraud Government/public administration one of the most commonly victimized sectors. Anti-fraud controls reduce the cost and duration of schemes. 85% of fraudsters had no previous charge or conviction for fraud related offense. Perpetrators often display warning signs including living beyond means (43%) and experiencing financial difficulties (36%).

Types of Fraud Corruption Asset Misappropriation Fraudulent Statements Conflict of interest Cash Financial Bribery Inventory & other assets Nonfinancial Illegal gratuities Economic extortion

Asset Misappropriation Cash Larceny Skimming Cash on hand Sales AR Refunds & other From deposit Un-recorded Write-offs Other Under-stated Lapping Fraudulent Disbursements Un-conceal

Asset Misappropriation Fraudulent Disbursements Billing Payroll Expense Reimb Check Tampering Cash Register shell company ghost employees mis- characterized forged maker false voids vendor commissions overstated forged endorser false refunds personal purchases workers comp fictitious altered payee falsified wages multiple reimb concealed checks authorized maker

Asset Misappropriation Inventory & other assets Misuse Larceny requisition & transfers false sales & shipping purchasing & receiving unconceal

Red Flags of Fraud - Employee Lifestyle changes: expensive car, jewelry, home, clothes Significant personal debt and credit problems Behavioral changes: physical appearance, absenteeism, creative “explanations”, inconsistent or illogical behavior, forgetfulness. Refusal to take sick or vacation leave. Tips or complains from employees. Overworked employee who will not let others help.

Red Flags of Fraud - Management Reluctance to provide information to auditors Weakness in internal control environment Decentralization without monitoring High employee turnover Other priorities

Red Flags of Fraud - Transactions Odd timing – days of week, month, year, season Frequency – too many, too few Amount – too high, too low, too alike, too different Use of common names and street addresses Excess number of exceptions

Red Flags of Fraud - Documents Source / backup documents cannot be located Unexplained items on reconciliations Only photocopied document is available Alterations on documents Questionable handwriting on documents

Wendy’s Top Ten “Can’t find” documentation Excessive missing documentation Form over function Management override of control “The rules don’t apply to me” attitude Lacking of segregation of duties Protecting an employee by bending the rules Secretive employees Turnover “Clustered” approvals

Risky Transactions PCard personal purchases PCard/travel double dip Cash receipting/depositing process Computer purchases Accounts receivable

How Organizations Encourage Fraud Hiding incidents of fraud Poor hiring choices Not listening to employees concerns Treatment of whistleblowers Weak enforcement policy Hoping for resignation Management override of controls Over-reliance on audits

How Organizations Encourage Fraud • Responsibility, accountability and authority not established or documented • Goals and objectives neither established or monitored for success • Lack of proper policies or procedures • Low priority for internal controls • Lack of separation of duties • Inadequate documentation • Form over function for controls

Creating a Low Fraud Environment Setting the tone Proper separation of duties Physical safeguards over assets Proper documentation Proper approvals Adequate supervision Physical inventories Reconciliations Honest, knowledgeable employees

Roles in Fraud Prevention and Detection It is management’s responsibility to institute, establish, and monitor controls and uncover fraudsters. • ABOR 6-711 “Internal Control Responsibilities” • President • Chief financial or business officer • Provosts, vice presidents, deans and other management • Chief audit executive • All employee

Roles in Fraud Prevention and Detection • Management • Sets the tone • Takes responsibility to institute proper controls • Segregates task responsibilities appropriately • Grants employees access only to appropriate resources • Is engaged and interested • Business role in department • Distributes policies and ensures understanding • Compares actual to budget or other system of record • Raises questions and concerns • Performs reconciliations in a timely manner

Roles in Fraud Prevention and Detection • Initiator • Understands policy • Gathers required documentation • Provides adequate business purpose • Preparer • Reviews and verifies that all documentation is complete and attached • Reviews transaction for reasonableness • Reviews transaction for compliance with policy

Roles in Fraud Prevention and Detection • Approver • Understands policy • Reviews transactions for compliance with policy, proper business purpose, timeliness, adequate documentation, etc. • Rejects transactions that are not sufficiently supported • Raises questions and concerns

Roles in Fraud Prevention and Detection • Comptroller’s Office • Educate the university community • Answer questions and address concerns • Monitor transactions for compliance and fraud • Suggest improvements to processes and controls • Internal Audit • Perform internal audits on a risk basis • Suggest improvements to processes and controls • Provide reasonable assurance that controls are working as intended

What to do if you Suspect Fraud • Report the concern to • Your supervisor • Financial Controls • Internal Audit • NAUPD online reports (anonymous)

Thank You! • Wendy.Swartz@NAU.edu • Sources • EideBailly • Association of Certified Fraud Examiners • State University of New York at New Paltz • Texas Tech University System • The Institute of Internal Auditors