Download

1 / 18

180 likes | 267 Views

Chronology of Satyam Fraud. Was it accounting jugglery or Fraud.

E N D

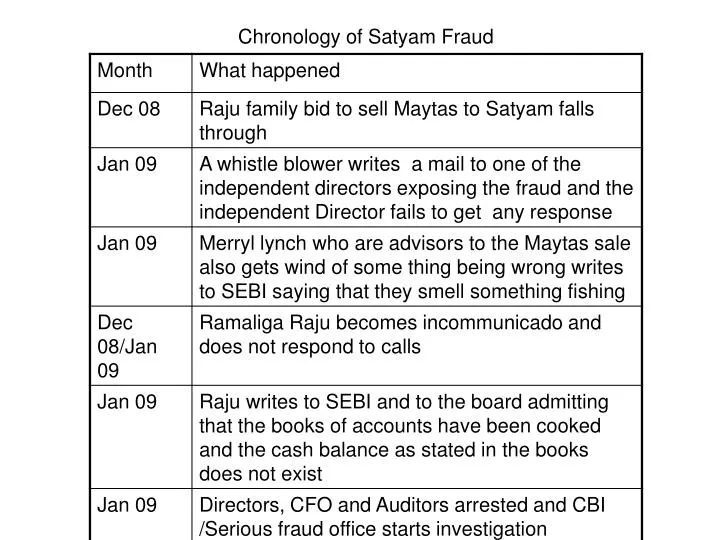

Was it accounting jugglery or Fraud • Raju admits that he along with his brother have cooked the books by inflating revenue, receivables and also by artificial head counts and inflation of expenditure cash and have falsified accounts by submitting fake documents to all people including Auditors who certified the books of accounts • Is this fraud or mere window dressing of accounts for share price or even assuming that it was accounting manipulation does it amount to fraud on investors • What is fraud • false representation of a matter of fact—whether by words or by conduct, by false or misleading allegations, or by concealment of what should have been disclosed—that deceives and is intended to deceive another so that the individual will act upon it to her or his legal injury. • Fraud must be proved by showing that the defendant's actions involved five separate elements: (1) a false statement of a material fact,(2) knowledge on the part of the defendant that the statement is untrue, (3) intent on the part of the defendant to deceive the alleged victim, (4) justifiable reliance by the alleged victim on the statement, and (5) injury to the alleged victim as a result • So what happened in Satyam can not be called accounting jugglery and it is a fraud on the investorseven if it is accounting fraud

Theories on what actually happened in Satyam … The most plausible explanation • The theory as confessed by Raju in the letter may be only partially true • What has been stated is not entirely true , the invoicing part was partially true and the part about diversion of salaries into artificial accounts also appears only to be partially true since the SFO / CBI are yet to trace the identity of all the fake employees • Raju and family borrowed heavily from money lenders to buy land in the family members names as well as benami names . The benami names and borrowing from secondary market made it extremely difficult to trace the funds • The theory is that the company deposit was used as a collateral for security for the borrowed money and the family also pledged the shares with the lenders. • The lenders were the tobacco mafia of Guntur and were possibly issuing threats for immediate repayment

Theories on what actually happened in Satyam … The most plausible explanation • He created main accounts along with sub accounts and only the sub accounts were considered for the audit purposes and only he and his brother knew about the main account • There was pressure building on him for repayment of the borrowings and since the real estate market was going down and was not liquid enough , Also due to the stock market fall the security against shares was inadequate and hence the pressure on the Satyam deposits which was than used for repayment through borrowing in benami names from the banks and repaid the original lenders • Subsequent pressure from the banks on the family to repay the bank loans brought things to head and consequent confession • How were the Bank documents fudged • Theory no one – The documents were falsified in the MD’s room • Theory two since these related to year ending numbers temp money was arranged in these accounts in the last days and immediately withdrawn after the year closing and partially forged documents were arranged for auditors

Who were involved and who were implicated- other than Raju and Raju

Who were involved and who were implicated- other than Raju and Raju……..contd

What are the questions that this scam raises • Questions on Control process – • Were there adequate controls in place in the company for revenue recognition in the company and were standard recognition policies followed ? • Was there internal controls in place to reconcile head count with salary pay out ? • Was there a process for bank account verification and reconciliation at the company level or a process of cash flow planning considering the number of bank accounts that a company is required to have – more than 500 accounts ? • Was the process of board resolutions related to bank accounts done seriously at board meeting or were simply added as minutes in the BM ? • Was an MIS in place which is based on project wise profitability and was the manpower utilization linked to the MIS ? • Were the internal control process reviewed by the internal auditors • Were the Internal controls and accounting policies reviewed by Statutory auditors as is legally required? • Some specific examples in the following slides where manipulations or simply not following processes could lead to problems

Questions that the scam raises • Were there adequate controls in place in the company for revenue recognition in the company and accounting processes followed ? • Normally there are defined process and policies for revenue recognition based on defined revenue recognition rules especially in service industry and can be easily manipulated ( Few illustrations) • Manufacturing – book sales directly through dealers / direct sales and reverse later –especially dealer sales can be difficult to verify • Cash business – effectively can be used for lowering or increasing income as the case may be • Service income for a manufacturing company – Xerox copy volume income on an accrual basis – Any volume can be assumed and reversed in subsequent year

Questions that this scam raises • Income from software contracts on completion method can be manipulated easily . The revenue is based on certification from prject managers and verification is difficult – Normally there is a process of regular certification o work done and invoicing – Further fake revenue can be done to parties overesas and remittance can also be managed by body shopping professionals taking travel advance and remitting from overseas – advantage all round? • Education services – can be accounted on due basis /cash basis rather than accrual basis • Real estate companies using contract accounting can manipulate based on certification of work done –billed /unbilled • The issue is there are defined controls and processes but get accrual system of accounting can be easily manipulated in service industry and can not be easily verifiable

Questions that this scam raises • What are the possible ways in which payroll can be manipulated • False head counts – Easy especially when there are huge head counts located across the globe where employees regularly are interchanged between holding companies and their subsidiaries and between projects and continued payments to resigned employees • ERP Vs physical count difference – This is a serious issue inspite of the same system running both packages • Manipulation of resigned employees by HR department • False names introduced in the salary sheets • False totaling of Bank credit sheets • Excess shown as payment through cash – higher receipts for lower payments –very common amongst manufacturing companies • Huge manipulation of payroll is possible and exists amongst companies across sectors

Questions---contd • Was there a process for bank account verification and reconciliation at the company level considering the number of bank accounts that a company is required to have – more than 500 accounts ?- Various possible reasons leading to lack of controls • There are large number of bank accounts created for various purposes in companies and monitoring could be very difficult • Possibility of promoters borrowing against company deposits in their personal names /sister companies without informing the company and marking lien • Guarantees against company bank accounts for promoters to borrow • Software companies opening overseas accounts on the basis of one account for one project and can manipulate these accounts for money transfers / laundering / also sub accounts is a major issue when not represented properly • Special purpose vehicles created for real estate projects and some may have direct cash deposits without the company being informed . This is used for land payments • Using remittance in transit /cheques in hand is another tool for manipulation • The presence of large numbers results in non conformance of rules related to verification of these accounts, Regular verification of BRS and regular confirmations from the banks which is a normal process

What does the CFO do – Problems and Solutions • Some problems and possible solutions –Detailed in the next few slides • Revenue Recognition policies and processes • Reliance on teams Vs Self Check –Given the time constraints and multiple role of the CFO • Role of Automation • Importance of MIS • Internal Audits and CFO approach to the internal audit process • Balancing prudence with pressure from top management –where to draw the line • Expected role of statutory auditor –expected role of CFO

Prevention of Frauds /Role of CFO- Revenue Recognition Important requirement is that defined processes need to be followed and the process must be regularly audited

Detection and Prevention of Frauds – CFO Vs Senior Management