Download

1 / 28

280 likes | 313 Views

Explore the crucial concepts of risk and return, time value of money, and decision-making areas in corporate finance. Understand the importance of shareholder wealth maximization, agency problems, and optimal contracts to mitigate risks and enhance financial performance.

E N D

Chapter 1 The Finance Function

Two key concepts • Relationship between risk and return • Time value of money

Risk and return • Risk refers to the possibility that actual outcome may differ from expected outcome. • Risk can be measured by standard deviation. • Investors require increasing compensation (return) for taking on increasing risk. • Return on an investment can be measured over a standard period, such as one year.

Risk and return • Shareholder return is annual dividend (D1) plus share price increase (P1 – P0). • Relative return in percentage terms is 100 x [(P1 – P0) + D1]/P0 • This is called total shareholder return.

Future values: compounding • Invest £100 now at 5% interest per year. After 1 year: £105.00 (100 x 1.05) After 2 years: £110.25 (105 x 1.05) • These are future values of £100 after 1 and 2 years. • Future values are found by compounding interest forward through time.

Present values: discounting • What sum of money invested now at 5% will give £120 in 2 years’ time? • This will be £120/1.052 = £108.84. • This is the present value of £120 receivedin two years if your required rate of returnis 5%. • Dividing by 1.052 to find a present value is called discounting.

Present values: discounting • A rational investor will prefer £108.84 to £100 at the current time. • Discounting allows us to compare £120 in two years’ time with £100 now. • Note that 1/1.052 = 0.907. • 0.907 is the present value factor or discount factor of 5% over 2 years (see tables). • Hence £120 x 0.907 = £108.84.

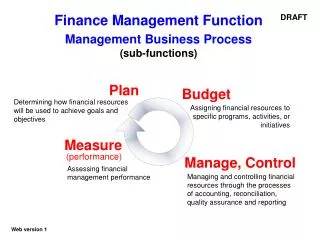

Decision-making areas A financial manager’s tasks can be divided into 3 areas: • Financing decisions • Dividend decisions • Investment decisions Key point: appreciate the interrelationship of these 3 decision areas

The financial manager Who is the financial manager in reality? • Finance Director (strategic decision making) • Corporate Treasurer (day-to-day cash management)

Possible corporate objectives • Shareholder wealth maximisation (SHWM) • Maximisation of profit • Maximisation of sales • Survival • Social responsibility Which one should we follow?

Shareholder wealth maximisation • Shareholders want dividends and capital gains • Capital gains reflect future dividends • Current and future dividends depend on future cash flows: • their magnitude or size • their timing • their associated risk.

NPV A 1 Linking NPV to SHWM CORPORATE NET PRESENT VALUE NPV B NPV C 2 NPV D SHARE PRICE 1: NPV is additive 2: Link relies on market efficiency 3: Share price taken as surrogate of SHW 3 SHWM

The agency problem Why does it arise? • Divergence of ownership and control • Managers’ goals differ from shareholders’ • Asymmetry of information What are the consequences? • Shareholder wealth is no longer maximised.

Consequences of agency problem • Managers will follow their own objectives i.e. increasing their.... • power • job security • pay and rewards. • Shareholders need to ensure that their own wealth is maximised.

Signs of an agency problem • Managers finance company predominantly with equity finance. • Managers accept low risk, short payback investment projects. • Managers diversify operations. • Managers follow ‘pet projects’. • Management gets reward for ‘below average’ performance.

Optimal contracts and agency • Best solution to the agency problem is to design managerial contracts that minimise the sum of the following costs: • financial contracting costs • monitoring costs • divergent behaviour costs.

Option 1: do nothing Leaving managers to their own devices is problematic: • Given human nature, managers will engage in sub-optimal behaviour. • Shareholders are satisficed rather than satisfied. • No action is not really an option.

Option 2: monitoring Problems associated with monitoring: • Costly in terms of both time and money • Who will pay? Large shareholders? What about ‘free-riding’ smaller investors? • Some managerial actions are hard to follow • May drive ‘bad managers’ underground

Option 3: reward good behaviour What do we link managerial rewards to? • Most commonly linked to: • profits • share price (e.g. via share options). • Rewarding is more common than monitoring. • But...tying rewards to profits may encourage short-termism and creative accounting.

Option 3: reward good behaviour • There are also problems using share options: • How many options should managers be awarded? • At what share price should managers be able to exercise their options? • Managers can get rewarded for poor performance if there is a ‘bull’ stock market.

Other areas of agency Companies are made up of a series of agency relationships: Shareholders Creditors i.e.banks, suppliers, bond holders Managers The Company Employees Customers N.B. Arrows go from ‘principal’ to ‘agent’ and show capital flows

Other areas of agency • Debt holders (principals) and shareholders (agents) • Solutions: security, restrictive covenants • Management (principles) and employees (agents) • Solutions: executive share option plans (ESOPs), monitoring, performance-related pay (PRP)

Corporate governance ‘ Corporate governance is about promoting corporate fairness, transparency and accountability’ J. Wolfensohn, President (World Bank), Financial Times, June 21, 1999. • Can be seen as attempt to solve agency problem using externally imposed regulation. • In the UK it is administered through a series of self-regulatory codes.

Cadbury Committee (1992) Recommended: • A voluntary code of practice • 3 non-executive directors at board level • Maximum 3-year duration contracts • Posts of Chairman and C.E.O. should be separate • Improved information flow to shareholders • Increasing independence of auditors

Greenbury Report (1995) Recommended: • One-year rolling contracts • More sensitivity by remuneration committees • PRP and share options to be phased out and replaced by ‘challenging’ long-term incentive plans (LTIPs) A 1996 PIRC report indicated widespread abuse of above.

Hampel Report (1998) and the Combined Code: • Stressed importance of a ‘balanced board’, non-executive directors and the role of institutional shareholders Combined code overseen by the London Stock Exchange: • Embodies Hampel, Cadbury and Greenbury recommendations • Compliance is an LSE listing requirement

Turnbull, Higgs and Smith • Turnbull (1999): detailed how boards could maintain sound systems of internal control (significant risk/systems required). • Higgs (2003): report designed to enhance the independence, and hence effectiveness, of non-executive directors. • Smith (2003): gave authoritative guidance on how audit committees should operate and be structured.

Is there an agency or corporate governance problem in UK today? • Agency still remains a problem in the UK: • legislation is only voluntary • human nature has not changed. • Managers still receive ‘excessive’ rewards • The future: • US style shareholders coalitions? e.g. CalPers • statutory legislation?