Download

1 / 33

330 likes | 342 Views

Demand, Supply & Equilibrium. Demand & its Determinants Wants Vs. Demand A general example: The demand for Soda Demand Schedule & Demand Curve Quantity Demanded Vs. Demand The Law of Demand Reasoning behind the law of Demand Substitution Effect Income effect

E N D

Demand, Supply & Equilibrium • Demand & its Determinants • Wants Vs. Demand A general example: The demand for Soda Demand Schedule & Demand Curve Quantity Demanded Vs. Demand • The Law of Demand • Reasoning behind the law of Demand • Substitution Effect Income effect • Movement along Vs. a shift of the Demand Curve • Demand Shifters

Demand & its Determinants • Wants Vs. Demand • Wants are the unlimited desires or wishes people have for goods and services. EX: I want a Volvo • Demand is a want backed by an ability an a willingness to pay. EX: I can demand a Pepsi

Demand Schedule & Demand Curve Demand Schedule : A demand schedule lists the quantities demanded at each price ceteris paribus Demand Curve: A demand curve shows the relationship between the quantity demanded of a good and its price, ceteris paribus.

Quantity Demanded Vs. Demand • Quantity Demanded The quantity demanded of a good or service is the amount that consumers plan to buy during a given time period at a particular price. • Demand The entire demand schedule or demand curve. The list of prices & their corresponding quantities.

The Law of Demand A basic economic hypothesis is that the price of a commodity and the quantity that will be demanded are related negatively, ceteris paribus. In other words, other things remaining the same, the lower the price the higher the quantity demanded and the higher the price the lower the quantity demanded.

Reasoning Behind the Law of Demand • Substitution Effect Price Opportunity cost Substitute away from the good As Price then quantity • Income Effect As Price increases given that income is fixed the number of units purchased decreases because real income has decreased

Movement Along Vs. Shift The change in price is the change in an exogenous variable that is represented on the graph thus it amounts to a movement along the demand curve and not a shift of the curve. A change in any other exogenous variable besides price results in a shift of the demand curve.

Increase in Demand • Increase in Demand More (quantity) is demanded at the same price or the same quantity is demanded at a higher price. (Demand curve shifts North East)

Decrease in Demand • Decrease in Demand Less (quantity) is demanded at the same price or the same quantity is demanded at a lower price (Demand curve shifts South West)

Demand Shifters • Prices of related goods Substitutes As the price of a substitute decreases, the demand for the good decreases (the demand curve shifts to the southwest). As the price of a substitute increases, the demand for the good increases (the demand curve shifts to the northeast).

Demand Shifters • Prices of related goods Complements As the price of a complement decreases, the demand for the good increases (the demand curve shifts to the northeast). As the price of a complement increases, the demand for the good decreases (the demand curve shifts to the southwest).

Demand Shifters • Expected Future Prices If future prices are expected to rise people will stock up on the good now thus leading to a rise in demand (the demand curve shifts to the northeast). If future prices are expected to fall, people will wait to purchase the good, thus leading to a fall in demand (the demand curve shifts to the southwest).

Demand Shifters • Population A rise in population leads to more potential buyers and thus an increase in demand (the demand curve shifts to the northeast).

Demand Shifters • Income As income rises people buy more of most goods Normal Goods: These are goods that people buy more of as income rises EX: Steak. Inferior Goods: These are goods that people buy less of as income rises. EX: Hot dogs

Supply & Its Determinants Supply Schedule: A supply schedule lists the quantities supplied at each price, ceteris paribus. Supply Curve: A supply curve shows the relationship between the quantity supplied and the price of a good ceteris paribus.

Quantity Supplied & Supply • Quantity Supplied The quantity supplied is the amount of a good that producers plan to sell during a given period at a given price • Supply Supply refers to the entire supply schedule or supply curve.

Law of Supply Ceteris paribus, the price of the commodity and the quantity supplied are related positively. Other things remaining the same, the higher the commodity’s price, the more its producers will supply. The lower its price, the less they will supply.

Reasoning Behind the Supply Curve The supply curve shows the least amount of money that a supplier will accept for a given unit. The supply curve slopes upward because the per unit cost of production (marginal cost) of the firm rises with the quantity produced.

Increase in Supply • Increase in Supply More (quantity) is supplied at the same price or the same quantity is supplied at a lower price. (Supply curve shifts South East)

Decrease in Supply • Decrease in Supply Less (quantity) is supplied at the same price or the same quantity is supplied at a higher price. (Supply curve shifts North West)

Supply Shifters • Cost of Production As cost of production increases supply shifts NW otherwise producers will make a loss. As cost of production decreases supply shifts SE.

Supply Shifters • Prices of Other Goods Produced Substitutes in production Two goods are said to be substitutes in production when by producing more of one good you produce less of the other. As the price of a substitute in production rises the supply curve of the good in question shifts NW. As the price of a substitute in production falls the supply curve of the good in question shifts SE.

Supply Shifters • Prices of Other Goods Produced Complements in production Two goods are said to be complements in production when producing one good automatically yields the other as a by product. As the price of a complement rises supply shifts SE. As the price of a complement falls supply shifts NW

Supply Shifters • Expected Future Prices If prices in the future are expected to rise suppliers hoard quantities to sell at the higher price thus resulting in a decline in supply. If prices in the future are expected to fall suppliers sell all they can now before prices drop resulting in an increase in supply.

Supply Shifters • Number of Suppliers In general supply increases with the number of suppliers and decreases with a decline in the number of suppliers. • Technology New and improved technology reduces the cost of production thereby increasing supply at a given price.

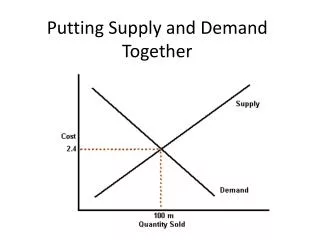

Market Equilibrium • Surplus: At any given price when the quantity supplied exceeds the quantity demanded at that price, there is said to be a surplus. A surplus usually results in sellers cutting prices in an effort to sell their product. The impact of a surplus in a market is to drive prices down and to increase the quantity traded.

Market Equilibrium • Shortage: At any given price if the quantity demanded exceeds the quantity supplied at that price there is said to be a shortage. A shortage usually results in buyers trying to outbid each other for the few scarce remaining units. The impact of a shortage in a market is to drive prices up and to increase the quantity traded.

Equilibrium Price: It is the price at which the quantity demanded equals the quantity supplied. There is no shortage or surplus at this price. • Equilibrium Quantity: It is the quantity bought & sold at the equilibrium price.