Download

1 / 5

50 likes | 209 Views

Variance Analysis. Overhead Variances. When working through this PowerPoint slide show, make sure you have a copy of the Budget Worked Example Question and Answer to refer to. These were handed out in class and can also be found on the unit web site. The overhead variances on the example are:

E N D

Variance Analysis Overhead Variances

When working through this PowerPoint slide show, make sure you have a copy of the Budget Worked Example Question and Answer to refer to. These were handed out in class and can also be found on the unit web site.

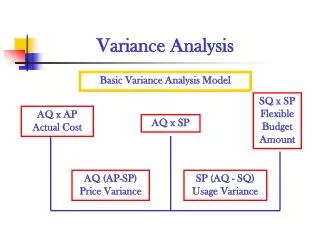

The overhead variances on the example are: • Production overheads - £1000 Adverse • Supervision costs - £25 Adverse • Rent and rates – 0 • Administration costs - £50 Adverse • Depreciation - £100 Favourable • We could comment on each of these variances individually, but in this unit we are only required to comment on the Total Overhead Variances. • There is no requirement to split these down. The variance is calculated by: Total budgeted (flexed) overheads – Total actual overheads

Total Overhead Variance Total budgeted overheads: 32000+750+1000+500+400 = 34650 Total actual overheads: 33000+775+1000+550+300 = 35625 Budget – actual = 975 Adverse This can be cross checked by adding together all the individual overhead variances: 1000A+25A+50A+100F = 975 Adverse

Practice Calculate total overhead variances for all exercises completed so far, making sure that they cross check to the total of the individual overhead variances.