Download

1 / 30

420 likes | 1.38k Views

Variance Analysis. Variance analysis. Variance analysis is the evaluation of performance by means of variances, whose timely reporting increase the opportunity for remedial action Variance analysis involves an investigation of the difference between Actual costs and standard costs or

E N D

Variance analysis • Variance analysis is the evaluation of performance by means of variances, whose timely reporting increase the opportunity for remedial action • Variance analysis involves an investigation of the difference between • Actual costs and standard costs or • Between actual costs/revenue and budget costs/revenue • It enables mangers to identify problems which need further investigation with a view to implementing remedial action • The value of variance analysis lies in managers being able to isolate where increased costs are actually occurring and take remedial action in that specific area

Standards and budgets • Standard costing and budgeting share one thing in common - they are both concerned with the future rather than what has happened • But there is an important difference - budgets relate to aggregates (e.g. sales revenue and total costs) whereas standards refer to per unit figures • Variances can be calculated against both standards and variance but for the sake of simplicity we will focus on variances against budget figures • Instead of using terms like standard costs or standard price we will use the terms budget price per unit or budget quantity

Variance • A variance is the difference between the budgeted level of costs and revenue and the actual levels of costs and revenues • Positive/favourable variance • A better than expected result • Costs lower or revenue higher than expected • Should led to higher than expected profits • Negative/adverse/unfavourable variance • A worse than expected result • Costs higher or revenue lower than expected • Should led to lower than expected profits

Steps to be taken • Construct a budget • Monitor results against the budget • Identify the variance • Calculate the variance • Analyse and explain the variance • Evaluate the significance of the variance both in absolute terms and in proportionate terms • Attribute responsibility for the variance • Take action to correct the problem

Basic variances • Actual Budgets • Sales revenue £9.7m £10m • Total costs £9.5m £9m • Profits £0.2m £1m • Sales revenue was £300k down on the budget figure- this was an adverse variance of £300k • Costs were £500k up on the budget figure- again adverse variance but this time of £500k • Add the two together and there is £800k variance on profits

Types of variance • Sales variance - sales revenue different from expected • Cost variance - total costs different from expected • Materials variance - cost of direct materials different from expected • Labour variance - cost of direct labour different from expected • Overhead variance - overhead costs different from expected • Profit variance - profits different from expected • These are the broad headings for variances but within each category there are sub variances

Quantity or price? • In all cases variances are caused by either • A price which is different from that planned • Volume which is different from that planned • Alternatively it is possible that a variance might be caused by a combination of the two • The purpose of variance analysis is to separate out the two elements

Sales revenue variance • This is where sales revenue is different from expected. • It is the result of • Sales volume variance - caused by the actual volume quantity sold being different from the planned volume • A volume variance measures the impact on revenue of the difference between actual and expected quantity sold And/or • Sales price variance – caused by a difference in the price actually paid compared to that in the budget • A price variance measures the difference between the planned price and the actual selling price

Sales revenue variance • Actual Budget • Quantity sold 9m 10m • Price per unit £3.5 £3.6 • Sales revenue £31.5m £36m • There was an variance on sales revenue of £4.5m.This was caused by a combination of a lower than planned level of sales and a price charged which was lower than planned • We can disaggregate the £4.5m by separating out the quantity/volume variance from the price variance

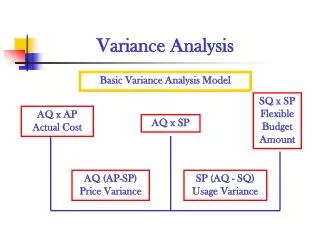

Formulae • Sales revenue variance = (AQ X AP) minus (BQ X BP) • Price variance = (AP- BP) x AQ • Volume/ quantity variance = (AQ –BQ) x BP • Where AP is actual price per unit and AQ is actual quantity sold • and BP is budget price per unit and BQ is budget quantity sold

Sales revenue variance • The overall variance is (9m x £3.5) minus (10m x 3.6) = £31.5m minus £36m. This is an variance of - £4.5m • It can broken down into price and volume variances • Price variance = (£3.5-£3.6) x 9m = - £0.9m • Volume variance =(9m - 10m) x £3.6 = - £3.6m • Notice that the price and volume variances sum to -£3.4.5m • Both variance are adverse although the volume variance was of greater significance than the price variance

Material variances • Variance on the cost of materials used as inputs can be attributed to: • Materials price variance • Difference between planned cost and the actual cost per unit of materials used. • and/or • Materials usage variance • The difference between the planned quantity of materials used and the actual quantity used

Materials variance • Actual Budget • Cost per unit £5 £4 • Quantity in units 500 550 • Total costs £2500 £2200 • There is an adverse variance of £300 on direct materials used in production • Notice that there was an adverse variance on price per unit but a favourable variance on quantity of materials used. Clearly the adverse variance more than cancelled out the favourable one

Formulae • Direct materials cost variance = (AQ x AC) minus (BQ x BC) • Direct materials price variance = (AC – BC) x AQ • Direct materials usage variance = (AQ – BQ) x BC • Where AQ is actual quantity used and AC is actual cost per unit • And BQ is budget quantity and BC is budget cost per unit

Materials variance • The total variance is (£5 x 500) minus (£4 x 550) = £2500- £2200 = £300 (adverse) • The variance on cost per unit of materials was (£5-£4) x 500 = £500 (adverse) • The variance on materials usage was (500-550) x £4 = £200 (favourable) • The adverse cost variance was greater than the favourable usage variance leading to an adverse variance overall

Labour variance • This type of variance is related to the cost of labour employed – both price of labour and/or its efficiency • Total labour cost variance - this is the difference between what it cost to employ direct labour and what it was expected to cost for the actual level of production • Labour rate (price) variance - labour available at a price different from expected. The variance is the difference between the wage rate that was expected to be paid and the wage rate actually paid • Labour efficiency variance - production required more (or less) labour than expected or planned. It is caused by labour being more (or less) efficient than was expected

Labour variance • Actual Budget • Rate per hour £9 £8 • Hours of labour required 50,000 40,000 • Total cost of labour £450,000 £320,000 • There was an adverse variance on direct labour of £130,000 • It was caused by a combination higher than planned wage rate and higher than planned quantity of labour to complete the work • But which of the two was more important?

Formulae • Total labour cost variance= (AR x AH) minus (BR x BH) • Labour rate variance = (AR- BR) x AH • Labour efficiency variance = (AH – BH) x BR • Where AR is actual wage rate per hour and AH is actual number of hours needed to complete the job • And BR is budget wage rate per hour and BH is budget hours to complete the job

Labour variances • The overall labour cost variance is = (£9 x 50k) minus (£8 x 40k) = £450k - £320k = £130k • The labour rate variance is (£9 - £8) x 50k = £50k • The labour efficiency variance is (50k-40k) x £8 = £80k • The high variance on labour costs was caused by a rise in the rate paid per hour and an increase in labour required over the quantity planned in the budget. Of the two variances the efficiency variances producer the greater impact

Fixed overhead expenditure variance • Formula: budgeted fixed overheads minus actual fixed overheads • Caused by a change in price of fixed overheads e.g. rent, standing charges • If expenditure is higher than expected it could mean the full costs of overheads is not being absorbed (covered) in the price • Over absorption occurs if actual overhead costs are less than standard

Variable overhead variances • Overall variance = budget cost of variable overheads minus actual costs of variable overheads • or (actual production x budget variable overhead rate per unit) -actual variable overhead cost • Caused by • Changes in overhead costs e.g. changes in the cost of water, gas, electricity • Or changes in activity levels linked to labour or machine hours worked

Overhead volume variance • This is cause by changes in activity levels linked to labour or machine hours worked • Formula: (budget quantity of input hours for actual production-actual input hours) x variable overhead rate • If actual output is less than planned this will cause a variance because overheads will not be fully absorbed • Output/sales in excess of plans will lead to over-absorption

Interdependence of variances (1) • The cause of a particular variance may affect another variance in a corresponding or opposite way • Workers trying to improve productivity (favourable labour efficiency variance) might become careless and waste more material (adverse material usage variance)

Interdependence of variances (2) • A new improved machine becomes available which causes • An adverse fixed overhead expenditure variance (because this machine is more expensive and depreciation is higher) • Favourable wage efficiency and fixed overhead volume variances (higher productivity)

Interdependence of variances (3) • If supplies of a specified material are not available, this may lead to • A favourable price variance (cheaper material used) • An adverse usage variance (cheaper material caused more wastage) • An adverse fixed overhead volume variance (production delayed while material was unavailable) • An adverse sales volume variance (unable to meet demand due to production difficulties)