Download

1 / 59

590 likes | 1.34k Views

Employee Plans Compliance Resolution System (EPCRS). Presented by: Gary Blachman November 17, 2009. Agenda. EPCRS overview Review of significant changes Sample compliance problems. Tax-Qualified Retirement Plans. Failure to comply with IRC 401(a) income taxation for all open tax years

E N D

Employee Plans Compliance Resolution System (EPCRS) Presented by: Gary Blachman November 17, 2009

Agenda • EPCRS overview • Review of significant changes • Sample compliance problems

Tax-Qualified Retirement Plans • Failure to comply with IRC 401(a) • income taxation for all open tax years • employer loses deductions for contributions made to plan during open tax years

Tax-Qualified Retirement Plans • Failure to comply with IRC 401(a) • plan participants are immediately taxed on vested contributions • plan participants lose right to roll over distributions tax-free to IRAs or other retirement plans

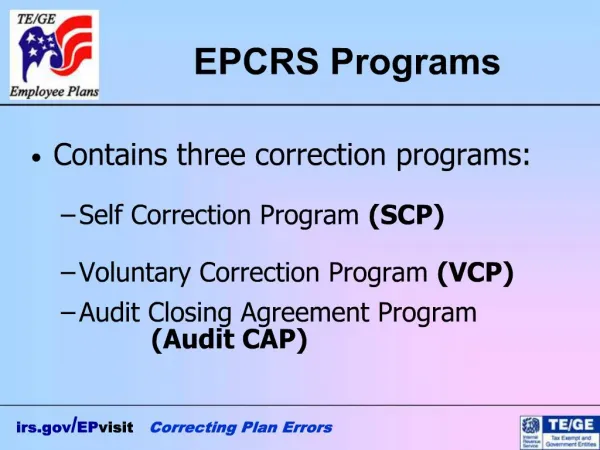

EPCRS Programs • Self-Correction Program (SCP) • Voluntary Correction Program (VCP) • Audit Closing Agreement Program (Audit CAP)

Scope of EPCRS • Qualified Plans – 401(a) • Tax-Sheltered Annuity Plans – 403(b) • Governmental Plans - 457(b) • SEPs, SARSEPs – 408(k) • SIMPLE IRAs – 408(p)

Objectives of EPCRS • Continued qualification of plan • IRS will not pursue FICA and FUTA taxes

Qualification Failures – four categories • Plan Document Failure • Plan provision that violates the Code • Operational Failure • Plan document complies with the Code but plan does not operate in accordance with its provisions or qualification requirements

Qualification Failures – four categories • Demographic Failure • Failure to satisfy requirements of: • Minimum participation – 401(a)(26) • Coverage – 410(b) • Nondiscrimination testing – 401(a)(4) • Employer Eligibility Failure

Principles and Correction Methods • Full correction required for all taxable years • Reasonable and appropriate correction methods • Model correction methods – Appendices A & B • Exceptions to full correction • Consistency

New – Exclusion of Eligible Employees • Failure to implement elections • Use elected deferral percentage instead of ADP • Failure to permit catch-up • Assume participant made catch-up equal to 50% of limit • Exclusion of employee from plan with Roth Contribution • QNEC = 50% x ADP correction

Exclusion of Eligible Employees • Example • 401(k) Plan year ends on December 31 • Employee eligible to participate May 1 • Employee provided an opportunity to elect deferrals July 1 • Employee elects to defer 5% of compensation

Exclusion of Eligible Employees • Question 1. • Can we assume employee would have elected to defer 5% of compensation for May 1 to June 30? • Response • No. Must look to elections after the period of exclusion to estimate deferrals during period of exclusion. Use ADP to estimate deferrals.

Exclusion of Eligible Employees • Question 1. • Can we assume no correction required, since exclusion is similar to brief period exclusion in App. B, 2.02(1)(a)(ii)(F)? • Response • No, since employee does not have at least 9 months remaining in plan year to make up deferrals.

Failure to Implement Employee’s Election in 401(k) Plan • Example • NHCE compensation = $30K • NHCE ADP = 5% • NHCE election = 10% • Plan match equals 50% of first 4% of compensation • Correction • Missed deferral = $3,000 ($30,000 x 10%) • QNEC for missed deferral opportunity = $1,500 (missed deferral x 50%) • QNEC for match = $600 ($30,000 x 4% x 50%) • Include lost earnings

Excluded Employees • Participant experienced a “missed opportunity to defer” • 401(k) - 50% of class ADP rate • 401(k) (safe harbor using nonelective contributions - 50% of 3% (instead of ADP rate) • 401(k) (safe harbor match) - 50% of “greater of 3% or deferral rate providing for at least 100% match” (instead of ADP rate) • After-tax - 40% of the average after-tax rate

Excluded Employee with Match Contribution • Matching Contribution correction • Based on match that would have been received had employee made deferral • Based on full amount of missed deferral, not missed opportunity cost

Failure to Include Employee in 401(k) Plan (Catch-up Contribution) • Example • NHCE has comp of $50K and was mistakenly prevented from making catch-up ($5,500 for 2009) • Correction • Missed deferral = $2,750 ($5,500 x 50%) • QNEC for missed deferral opportunity = $1,375 (missed deferral x 50%) • Adjusted for lost earnings

Failure to Include Employee in 401(k) Plan (Designated Roth Contribution) • Example • NHCE has comp of $50K • Match equals 100% of first 3% of comp, 50% of the next 2% of comp • NHCE ADP = 5% • Correction • Missed deferral - $2,500 ($50,000 x 5%) • QNEC for missed opportunity cost of deferral = $1,250 ($50,000 x 5% x 50%)

Failure to Include Employee in 401(k) Plan (Designated Roth Contribution) • Corrective QNEC for match is equal to the match that would apply based on the full amount of missed deferral • QNEC for match is $2,000 ($50,000 x first 3% of comp) + ($50,000 x 2% x 50% of comp)

Failure to Include Employee in 401(k) Plan (Designated Roth Contribution) • Question: Would the corrections in the examples above change, if the plan also provides employees with the ability to designate all or a portion of their elective deferrals as Roth contributions?

Failure to Include Employee in 401(k) Plan (Designated Roth Contribution) • Answer: • No change to the corrective QNEC • The corrective QNEC cannot be contributed or allocated to a Roth account • A corrective QNEC is taxed upon distribution

New - Participant Loans • Under VCP, the IRS will allow correction if plan loans violated the – • Limit on loans under IRC 72(p)(2)(A) • Plan term requirements IRC 72(p)(2)(B) or (C ) • Plan repayment terms, resulting in default of loan • Correction permitted when original term of loan has not expired – may be re-amortized over remaining term

New - Participant Loans • Correction permitted even if plan does not contain specific reference to IRC 72(p)

Employer Payment of Loans When is employer payment required? • Participant’s responsibility to make loan repayments of principal and interest. • Employer payments required if – • employer action caused failure • ROR on plan investments exceeded loan rate

Defaulted Loan – Reamortization correction Question: Is it permissible to use an interest rate different from original interest rate? Answer: If original interest rate complied with plan terms, IRS expected correction will use same interest rate.

New - Participant Loans • 50% Reduction in fee schedule • Plan loan failure is the only failure submitted • Affected participants are less than 25% of total participants in any plan year • Error resulted from failure to follow IRC 72(p)

New - Correction of IRC 415 Failures • Revised guidance • If excess annual additions are due to nonelective employer contributions, then – • must be reallocated to other participants’ accounts if plan provides rule for allocation • if no reallocation rules, must be removed from participant’s account and applied to future employer contributions • If excess is due to elective deferrals or after-tax contributions, must return to participant (including earnings)

Failure to Suspend Deferrals Example: A 401(k) plan provides hardship distributions. After a hardship distribution, elective deferrals suspended for 6 months. Question: What is the correction if the plan fails to suspend deferrals?

Failure to Suspend Deferrals Option 1: Can plan return improper elective deferrals (adjusted for earnings)? Answer: Yes, places participant in same position if failure had not occurred.

Failure to Suspend Deferrals Option 2: Can plan suspend elective deferrals for 6 months going forward? Answer: Maybe. May not place participant in same position. i.e., if match levels differ or participant terminates before 6 months.

Failure to Suspend Deferrals Option 3: Can plan take no action at all and merely revise administrative procedures going forward? Answer: No. This does not correct the failure.

Forfeitures as corrective QNECs Question: Can plan use forfeitures to make QNECs and correct failed ADP test? Answer: No. QNEC must be nonelective contributions that are 100% vested and satisfy distribution requirements when contributed to plan. Forfeitures were not fully vested when made and do not correct the failure.

Forfeitures as corrective QNECs Question: Can plan use forfeitures as employer contribution to correct improperly excluded employees? Answer: Yes. If employee is 100% vested and 401(k) distribution restrictions apply when contribution is made to correct the failure.

Failure to provide 401(k) safe harbor notice Question: What is the correction for failure to provide safe harbor notice? Answer: It depends. If employees informed and able to elect deferrals, sponsor may revise procedures going forward. If employees unable to make elections, then an exclusion of eligible employees. Corrective contributions required.

Correction by Plan Amendment Question: What type of failures can be corrected by plan amendment? Answer: Operational and demographic failures. Specifically, interim and certain discretionary amendment, EGTRRA good faith amendments, failure to amend by RAP or RAC deadlines.

Correction by Plan Amendment Question: What type of relief is available? Answer: • Amendment treated as adopted timely • Extended RAC available • $375 fee • Streamlined Application (Appdx F, Sch 1) • No DL submission under VCP

Failure to file on-cycle Determination Letter Question: Is VCP available to fix a failure to file on-cycle DL? Answer: No. IRS does not consider a failure to file an on-cycle DL as a qualification failure eligible for VCP.

Relief from Additional Excise Taxes • IRS will not pursue excise tax penalties • Minimum distribution failures – limited circumstances • Nondeductible employer contributions – certain circumstances • Excess 401(k) contributions not distributed in timely manner – certain circumstances

Expanded Excise Tax Relief • IRS will not pursue excise tax on certain excess contributions made to IRAs • participant must remove the overpayment (plus earnings) from IRA and return to plan; or • participant must withdraw overpayment from IRA and report as taxable distribution in tax year of withdrawal; or • if overpayment due to improper in-service distribution, plan sponsor shows good cause why relief should be granted

Income Tax Relief • IRS will not pursue part or all of the 10% additional income tax under 72(t) in certain circumstances • participant repays premature distribution to plan • plan sponsor may need to pay additional VCP fee equal to part or all of applicable tax

New De Minimis Threshold • Exception to full correction • if corrective contribution is less than $75 • overpayments and excess amounts of $100 or less may be left uncorrected (SCP, VCP and Audit CAP)

SCP – Self Correction Program • No disclosure to IRS, no fee, no sanctions • Only applies to operational failures • Must have a prior determination letter for relief • Must have established practices and procedures to assure ongoing compliance

SCP versus VCP • Distinction between insignificant and significant errors • List of factors • whether failure occurred during period of exam • percentage of assets/contributions involved • number of years involved • percentage of participants affected • percentage of participants who could have been affected • correction made within reasonable period • reason for the failure • Uncertainty for plan sponsor

When is a determination letter required in VCP? • DL submission required • correction of qualification failure through plan amendment during on-cycle year • non-amender failure • DL submission NOT required • Interim/discretionary amendments • operational or demographic failure in off-cycle year

When is a determination letter required in VCP? • DL submission optional • Certain new individually designed plans • Urgent business need

VCP – Voluntary Compliance Program • Submission procedures • Ends with a compliance statement • Determination letter – if plan on-cycle

VCP Application • Description of failures • Plan sponsor’s proposed method of correction • Calculation of any corrective contributions • Relevant pages of plan documents related to operational failures • Signed amendments or plan documents for plan document failures

New Rules for Earnings Calculations • Earnings must reflect actual earnings based on participant elections • Reasonable estimates permitted • U.S. Department of Labor’s Voluntary Fiduciary Correction Program Online Calculator as proxy for reasonable interest rate