Download

1 / 20

200 likes | 375 Views

The inflation appreciation trade-off revisited. The monetary management of the Zambian copper boom by Elva Bova PhD candidate SOAS, University of London, NCCR Trade Regulation, WTI, Berne Email: eb29@soas.ac.uk. Introduction. Presentation outline. Theoretical framework:

E N D

The inflation appreciation trade-off revisited The monetary management of the Zambian copper boom by Elva Bova PhD candidate SOAS, University of London, NCCR Trade Regulation, WTI, Berne Email: eb29@soas.ac.uk

Presentation outline Theoretical framework: exchange rate management and the RER The nominal appreciation of the Kwacha: impact on non traditional exports Inflation, food and non food: Cointegrated VAR for exchange and money channel Results and policy implications

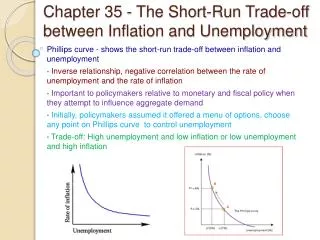

Theoretical framework: the trade off Further to a commodity boom the economy is exposed to the risk of a RER appreciation: Dutch disease (Pt/Pnt) Money inflation link resource switching effect (e Pt/Pnt) spending effect flexible fixed nominal appreciation inflation (money-exchange channels)

Theor.framework: the trade-off revisited Neutrality argument: the real exchange rate (Pt/Pnt) appreciates under the two regimes Hypothesis: RER not neutral to the exchange rate regime. -food component in CPI -economy operates not at full employment, yet absorptive capacity is limited How to maintain export competitiveness in an inflation stabilising monetary framework?

The copper boom in Zambia The copper boom The increase in export receipts, Debt relief at the end of 2005 and a surge in foreign capital put pressure on the Zambian Kwacha. Monetary framework: Monetary targeting (M3, reserve money) with price stability as the main objective for monetary policy. Flexible exchange rate (IMF managed float) with interventions mainly aimed at smoothing volatility. The Kwacha appreciation

The nominal appreciation Non Traditional Exports (NTEs) Source: Export board of Zambia

The nominal appreciation Source: Export board of Zambia

Inflation Source: Bank of Zambia Two main channels from exchange rate management to inflation: Money supply channel Exchange rate channel

The model The unrestricted VAR: Xt = ΠXt-1 + Φ1 Dtt + μ1 t + μ0 + εt εt ~ Np (0, Σ), t=1,….., T Variables:M3 = log M3sea – log CPIz, Ex = log CPIz – log CPIus –NEus-z CPI f, CPI nf Exog.:real copper price, real oil price* Residual Analysis Identification of the cointegrated VAR Long run: Short run

Results and interpretations Food inflation: not significantly related to money supply (or copper price); long run relationship with the exchange rate; in the short run adjusts more to its previous values (0.52) than with respect to deviations from its equilibrium with exchange rate (0.17). Non food inflation: significant long run relationship with money supply, not with the exchange rate; it adjusts rapidly to deviations from its equilibrium with money supply; The exchange rate: related in the long run with money supply and the price of copper (commodity currency hypothesis);

Conclusions Under the flexible exchange rate regime with a monetary target and price stability as overriding objective, the Zambian Kwacha has appreciated in nominal terms (2005, 2007). The nominal appreciation (2005) has fed into a real appreciation with deterioration of some non traditional exports: tobacco, cotton, coffee and horticulture, with increase in unemployment and possible rural-urban bias. Had Bank of Zambia managed more the exchange rate, inflation would have increased but not that muchmore likely through the exchange rate channel, since the money channel is only valid for non food prices, which comprise 30% of total headline CPI.

Conclusions Thank you very much

The copper boom Source: IMF-IFS, Bank of Zambia

The Kwacha Source: IMF-IFS, Bank of Zambia

Headline CPI composition Composite Index Weights Food and Beverage Index 57% Transport and Communication 9.60% Rent, Fuel and Lighting 8.50% Furniture and Household Goods 8.20% Medical care 8% Clothing and Footwear 6.80% Recreation and Education 4.90% All other goods and services 4.10%

Residual analysis Multivariate tests • Tests for Autocorrelation • Ljung-Box(37): ChiSqr(560) = 674.636 [0.000] • LM(1): ChiSqr(16) = 39.811 [0.001] • LM(2): ChiSqr(16) = 18.501 [0.295] • Test for Normality: ChiSqr(8) = 14.927 [0.061] Univariate Tests • Std.Dev Skew. Kurtosis ARCH(2) Normality R-Squared M3 0.021 -0.097 3.111 2.727 [0.256] 0.721 [0.697] 0.510 CPI f 0.009 0.241 2.823 0.735 [0.692] 1.684 [0.431] 0.755 CPInf 0.006 0.434 2.853 3.735 [0.155] 6.306 [0.043] 0.735 Ex 0.024 -0.101 3.720 5.131 [0.077] 4.872 [0.088] 0.612

Trace test for number of cointegrating relations p-r r Eig.Value Trace Trace* Frac95 P-Value P-Value* 4 0 0.506 191.011 181.954 63.659 0.000 0.000 3 1 0.279 90.130 86.714 42.770 0.000 0.000 2 2 0.204 43.341 41.043 25.731 0.000 0.000 1 3 0.072 10.671 10.052 12.448 0.101 0.127 Source: RATS estimation

Long run identification M3 CPI-f Ex CPI-nf COP T(2005:12) TREND Beta(1)0.225 0.000 1.000 0.000 -0.377 0.000 -0.007 (2.107) (.NA) (.NA) (.NA) (-12.009) (.NA) (-8.803) Beta(2) 0.000 1.000 0.195 0.000 0.000 0.009 -0.016 (.NA) (.NA) (6.010) (.NA) (.NA) (9.418) (-119.363) Beta(3)0.020 0.000 0.000 1.000 0.000 0.000 0.000 (4.632) (.NA) (.NA) (.NA) (.NA) (.NA) (.NA) TEST OF RESTRICTED MODEL: CHISQR(7) = 3.748[0.879] Source: RATS estimation

Short run identification M3 Ex CPIf CPInf Ex-1 0.1550 0.2492 -0.0514 (0.0218) (0.0004) (0.0069) CPIf-1 -0.5693 0.5172 0.1163 (0.0003) (0.0000) (0.0082) M3-1 -0.2938 (0.0001) ECM1-1 -0.0670 -0.1688 (0.0543) (0.0000) ECM2-1 -0.1696 (0.0000) ECM3-1 -0.7982 (0.0000) Dcop 0.1469 (0.0000) LR test of over-ident. restrictions:Chi^2(43)=61.645 [0.0613] Source: RATS estimation