Download

1 / 27

270 likes | 420 Views

Trade-off between the exchange rate and inflation. Supervisor: Professor Moisa Altar MSc Student: Razvan Pascalau. Abstract.

E N D

Trade-off between the exchange rate and inflation Supervisor: Professor Moisa Altar MSc Student: Razvan Pascalau

Abstract Focus: the dynamics of the convergence of both the exchange rate and inflation to the optimum pre-accession requirements revealing the trade-off existing between those two macroeconomic variables both in the short and the long term. On the short-run: analysis of the instruments to fight-off inflationary pressures in an Inflation Targeting framework On the long run: PPP hypothesis vs. Balassa-Samuelson effect

Contents: 1.Introduction………………………………………………..…………..4 2.Technical aspects of IT in Romania…..…………………..…………...5 3.Econometric estimation (I)………………...…………………………..6 3.1. VAR methodology…………………………………….…..6 3.2. Data……………………………………………………..…6 3.3. Estimation and specification issues……………………..…8 4.Interpreting the effects of Monetary Policy from the data……………..8 5.Purchasing Power Parity versus the Balassa-Samuelson hypothesis.13 6.Econometric estimation (II)………………………………………...…15 6.1. Methodology……………………………………………...15 6.2. Data……………………………………………………….15 6.3. Unit Roots and Co-Integration……………...…………….15 6.4. Error Correction equations…………………………..……17 7.Conclusion………………………………………………………...…..17 8.Bibliography…………………………………………………………..33

Appendix: Appendix 1…………………………………………………………………..18 1.1. Unit Root tests…………………………………………………18 1.1. Johansen Co-Integration test…………………………………..22 1.1. Error terms analysis…………………………………………..26 1.4. Stability coefficient tests………………………………………28 1.5. Granger causality tests……………………………………..…30 Appendix 2..…………………………………………………………………30 2.1. Johansen Co-Integration test (I)…...……………………….….30 2.2. Pairwise Granger causality/Block exogeneity Wald test……...31 2.3.ECM………...……...………………………………………….31 2.4. Engle-Granger stationarity test………………...……………...32 2.5. Johansen Co-Integration test (II).……………………………...32

Three-step approach to the European monetary integration Adoption in the near future of the IT policy regime as Romania faces the integration challenge Specify and estimate several vector-autoregressive models: interest rate policy shocks and interventions on the foreign exchange market lead to puzzling effects ( trade-off between the exchange rate and inflation) Balassa-Samuelson effect: Romania’s case Co-Integration analysis under PPP theory: the real appreciation of ROL can be explained as the correction of an undervalued currency, with no evidence of an appreciation in the equilibrium exchange rate so far as the forecast of year 2000 1. Introduction

“The economic program of pre-accession” (2001) - the Romanian government stated IT as the first option of the NBR for years 2003-2004 The literature on IT can be separated in two categories The analysis of IT in emerging economies should consider the higher-pass through from the exchange rate into inflation pressure The transactions of the NBR on the foreign exchange market - frequent, exceeding what we can normally see as specific to a managed float regime The interest rate policy instrument so far played an insignificant role due to the monetary and non-monetary adverse conditions: fiscal dominance, position of net-debtor of the NBR towards the banking system, thin Treasury bonds market etc. 2. Technical aspects of IT in Romania

3. Econometric estimation (I)3.1.VAR Methodology • VAR modelsfocus on the analysis of the “innovations” on the variables under study • yt = b10 - b12* zt + 11*yt-1 + 12*zt-1 + yt (3.1) • zt = b20 – b21* yt + 21*yt-1 + 22*zt-1 + zt (3.2) Using matrix algebra we have: • Bxt = 0 + 1xt-1 + t where • Premultiplication by B-1 allows us to obtain the VAR in standard form xt = A0 + A1xt-1 + et (3.3) where A0 = B-10, A1 = B-11, et = B-1t • Using the new notation the following system of equations results: • yt = a10+ a11*yt-1 + a12*zt-1 + e1t (3.4) • zt = a20+ a21*yt-1 + a22*zt-1 + e2t (3.5)

3. Econometric estimation (I)3.2.Data • lniprodi_sa as the logarithm of the industrial production index (Y) • lnpretprodi as the logarithm of the industrial price index (PPI) • lncpi as the logarithm of the consumers price index (CPI) • m2nom_sa as the logarithm of the monetary aggregate, seasonally adjusted (M2) • dobref reference interest rate used by the NBR • dobdep asthe percentage of the sterilization (“deposit taking”) interest rate (D2) • lncursnom as the nominal exchange rate between the US dollar and ROL (Exc) • expnet_sa as the net export calculated as the difference between export (fob) and import (fob) (Exp) • ygrowth as the output growth, approximated through the growth of the industrial production index (Ygr)

3. Econometric estimation (I)3.2.Data Two dummy variables are included in each VAR: dumf97 and dumm97. The first dummy picks up the rapid nominal depreciation at the start of 1997 following the ending of foreign currency rationing. The second dummy is required for the inflationary effect of heavy capital inflows following the resumption of the stabilization program at the start of 1997. Altogether there are five models I have estimated, as follows: M(1) : CPI, PPI, Exc M(2) : CPI, Ygr, Exp, Exc M(3) : CPI, M2, Exc M(4) : Y, CPI, D1, M2, Exc M(5): Y, CPI, D2, M2, Exc

3. Econometric estimation (I)3.2.Estimation and Specification Issues • Testing the order of integration: All variables are I(1) integrated. (see Appendix 1.1) • The choice for the optimum lag length: 1 lag for models M(1) and M(2), 3 lags for M(3) and 3 for M(4) and M(5). • Johansen Cointegration test: rejects the existence of cointegration at both 5% and 1% significance levels for the first three models (see Appendix 1.2.). However for the last ones the VAR will not fulfill the stability condition anymore. Therefore I will estimate the models in first differences • The test for the VAR stability: proves successful for all models. • Error terms analysis: error terms are white-noise processes. That means they are normally distributed, have constant variance (i.e. homoskedasticity property) and have no autocorrelation. Without the display of a first lag autocorrelation, the above mentioned conditions look satisfactorily for all models. (see Appendix 1.3). • The test for the stability of the coefficients: was conducted in order to identify any regime changes in the period under study (see Appendix 1.4).

4. Interpreting the Effects of the Monetary Policy from the Data

4. Interpreting the Effects of the Monetary Policy from the Data

4. Interpreting the Effects of the Monetary Policy from the Data

4. Interpreting the Effects of the Monetary Policy from the Data

4. Interpreting the Effects of the Monetary Policy from the Data

4. Interpreting the Effects of the Monetary Policy from the Data

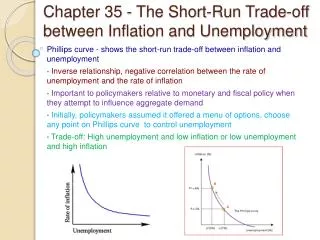

R e s p o n s e o f D ( L N C P I ) t o D ( D O B R E F ) R e s p o n s e o f D ( D O B R E F ) t o D ( D O B R E F ) .012 5 4 .008 3 2 .004 1 .000 0 -1 -.004 -2 -.008 -3 2 4 6 8 10 12 14 16 2 4 6 8 10 12 14 16 R e s p o n s e o f D ( M 2 N O M _ S A ) t o D ( D O B R E F ) .02 .004 .01 .000 .00 -.004 -.01 -.008 2 4 6 8 10 12 14 16 2 4 6 8 10 12 14 16 4. Interpreting the Effects of the Monetary Policy from the DataFigure 7. The impulse response R e s p o n s e t o C h o l e s k y O n e S . D . I n n o v a t i o n s ± 2 S . . E R e s p o n s e o f D ( L N C U R S N O M ) t o D ( D O B R E F )

4. Interpreting the Effects of the Monetary Policy from the Data

5.Purchasing Power Parity versus Balassa-Samuelson hypothesis PPP theory: nominal exchange rates should move in line with price differentials, at least in the long run (stationary real exchange rate) Balassa (1964) & Samuelson (1964) show that if productivity gains in the tradable sector exceed those in the non-tradable sector, then the equilibrium real exchange rate should appreciate Two possible explanations for the real appreciation of the exchange rate can be put forward: 1.Excessive undervaluation at the beginning of transition 2.Structural changes in demand and production ( Halpern & Wyplosz, 1997, 2001)

6. Econometric estimation (II)6.1.Methodology Cursscht = C(1) + C(2)*Inflromt - C(3)*Inflsuat + ut, (6.1) • Cursscht is the logarithm of the exchange rate, the domestic currency price of the dollar; • IInflromt is the logarithm of the industrial price index; • Inflsuat is the logarithm of the US industrial price index; • ut represents deviations from PPP. For the PPP theory to hold, it is required that C(2)= C(3)= 1 Furthermore, if the nominal exchange rate and the two price series are non-stationary, then the strong form of the PPP hypothesis requires that the nominal exchange rate and relative prices are co-integrated. Two sample periods are used: 1992:01-2000:08 & 1992:01-2003:01

6. Econometric estimation (II)6.3.Unit Roots and Co-Integration 1992:01-2000:08 Normalized cointegrating coefficients (std.err. in parentheses) CURSSCH INFLROM INFLSUA 1.000000 -0.963950 0.980738 (0.01677) (0.68234) (2=0.000582, p-value =0.980747 for restrictions C(2)=1 and C(3)=-1) 1992:08-2003:01 Normalized cointegrating coefficients (std.err. in parentheses) CURSNOM INFLROM INFLSUA 1.000000 -0.976765 0.086388 (0.02625) (0.87964) [-37.2079] [ 0.09821]

6. Econometric estimation (II)6.3.Error Correction Equations According to the Engle & Granger (1987) representation theorem,a valid error correction model implies co-integration. I specify two error correction equations, for which the dependent variables are the nominal depreciation and domestic inflation. Error Correction: D(CURSSCH) D(INFLROM) CointEq -0.039486 0.181091 (0.04405) (0.02959) [-0.89648] [ 6.11977] White Heteroskedasticity Test CHSQ(1):p=0.132248 Breusch-Godfrey Serial Correlation LM Test CHSQ(16):p=0.133201

7. Conclusion Efficiency of the monetary policy instruments in the light of a possible change to an inflation targeting framework Weak performance concerning appreciation of the real exchange rate through productivity gains The interventions on the foreign exchange market often lead to adverse effects (trade-off effect) The limitation of the interest rate channel (trade-off effect) Appreciation of the real exchange rate mainly due to the initial devaluation Year 2000 can be seen as a changing point in the evolution of the real appreciation process Possible trade-off effect on the long run as Romania accedes the EMU