Download

1 / 34

350 likes | 402 Views

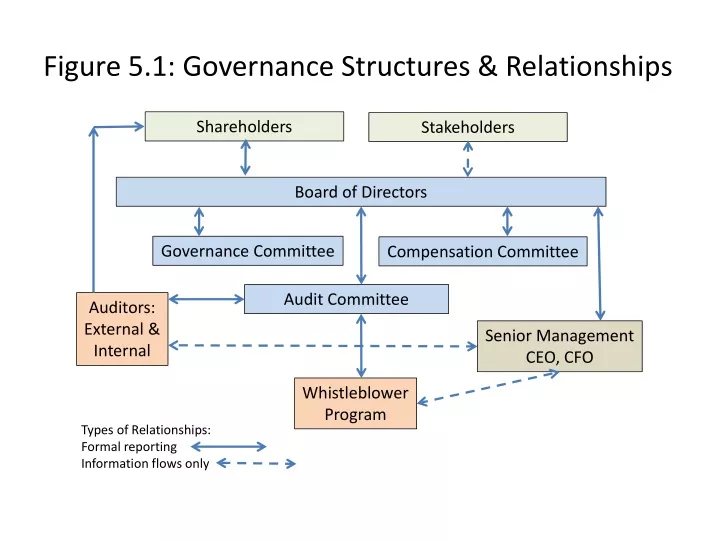

Figure 5.1: Governance Structures & Relationships. Shareholders. Stakeholders. Board of Directors. Governance Committee. Compensation Committee. Audit Committee. Auditors: External & Internal. Senior Management CEO, CFO. Whistleblower Program. Types of Relationships:

E N D

Figure 5.1: Governance Structures & Relationships Shareholders Stakeholders Board of Directors Governance Committee Compensation Committee Audit Committee Auditors: External & Internal Senior Management CEO, CFO Whistleblower Program Types of Relationships: Formal reporting Information flows only

Table 5.1: Directors’ Functional Responsibilities • Safeguard the interests of the company’s shareholders • Review overall business strategy, and in some jurisdictions take stakeholder interests into account • Select and compensate the company’s senior executives • Evaluate internal controls and external auditor, and recommend the company’s outside auditor for election by the shareholders • Oversee the company’s financial statements, and recommend them to the board for transmission to the shareholders • Monitor overall company performance Adapted from the Report on The Role of The Board of Directors in the Collapse of Enron, U.S. Senate Permanent Subcommittee on Investigations, July 8, 2002 • Ensure: • An effective system of internal controls and internal audit • An effective whistleblower system reporting to the audit committee • Effectiveness of the company’s risk management program • Efficacy of the company’s ethical corporate culture SOX and Recent Governance Expectations Legal accountability to shareholders; strategic accountability also to stakeholders

Table 5.2: Directors’ Behavioral Expectations Fiduciary Duties • Acting in the best interest of the company (shareholders & stakeholders) • Loyalty to be demonstrated by independent judgment. • Actions to be in good faith, obedient to the interests of all • Actions demonstrate due care, diligence, and skill (i.e. financial literacy) Adapted from Statement of Corporate Governance, The Business Roundtable (September 1997) Conflicts • Require disclosure, and actions to manage effectively Liability Issues • Business Judgment Rule • Oppression remedy • Personal liability for Tort Claims Responsibilities of Directors in Canada, Torys LLP, 2009

FIGURE 5.2 MAP OF CORPORATE STAKEHOLDER ACCOUNTABILITY Shareholders Activists Employees Governments Customers Corporation Lenders & Creditors Suppliers Others, including the Media, who can be affected by or who can affect the achievement of the corporation’s objectives Competitors

Accountability = Financial & StrategicincludingEthical & Legal Whistle- Blowers Professional Accountants Including Internal Auditors Ethics Officer FIGURE 5.3STAKEHOLDER ACCOUNTABILITY ORIENTED GOVERNANCE PROCESS SHAREHOLDERS + OTHER STAKEHOLDERS PUBLICINTEREST All Interests Sets Vision, Mission, Strategy, Policies, Codes, Compliance, Feedback, Compensation Appoints CEO, CFO BOARD OF DIRECTORS External Auditors Lawyers Guidance Feedback CORPORATE CULTURE Created by Management Leads to Corporate Actions Financial Reports

SHAREHOLDERS + OTHER STAKEHOLDERS PUBLICINTEREST CORPORATE CULTURE Created by Management Leads to Corporate Actions Actions Motivation Beliefs Values FIGURE 5.4STAKEHOLDER INTERESTS RANKING, RISK ASSESSMENT, & USAGE Accountability = Financial & Strategic including Ethical & Legal All Interests Sets Vision, Mission, Strategy, Policies, Codes, Compliance, Feedback, Compensation Appoints CEO, CFO CORPORATE RISK ASSESSMENT BOARD OF DIRECTORS Integrate Into Corporate Value System & Actions Identify All Stakeholders Assess & Rank All Interests Prepared by management for Board review and approval Guidance Feedback

FIGURE 5.5ALIGNING VALUESFOR ETHICAL MOTIVATION & ACTION IdentificationAssessmentRank StakeholderInterests CorporateValue System CorporateValue System ReportsObservations StakeholderEvaluation ValuesTransmission Policies, CodesReinforcement CORPORATE CULTURE Created by Management Leads to Corporate Actions OtherInfluences Actions Motivation Beliefs Values

TABLE 5.3 CULTURAL VALUES AND HYPERNORMS

TABLE 5.4 AREAS OF CORPORATE RISK ASSESSMENT

TABLE 5.5 ETHICS RISK MANAGEMENT PRINCIPLES

FIGURE 5.6 CONFLICT OF INTEREST FOR A DECISION MAKER A decision maker (D) “has a conflict of interest if, and only if, (1) D is in a relationship with another (P) requiring D to exercise judgement in P’s behalf and (2) D has a special interest tending to interfere with the proper exercise of judgement in that relationship. Special Non-P Interests Decision Maker (D) has a duty to act/judge in P’s best interest P’s Satisfaction based on Fulfillment of P’s Interests

FIGURE 5.7 TYPES OF CONFLICT OF INTEREST & ACTIONS REQUIRED No Conflicts or Sufficient Safeguards Apparent No Harm Not Apparent Insufficient Safeguards Action to Avoid, Prevent and/or Mediate Harm Action to Ensure Ethical Appearance

Figure 5.8Governance determines Extent of Compliance or Deviance • Governance – guidance, monitoring and enforcement – determines decisions & actions • 20/60/20 Rule provides key to risk reduction • Portion of employees who will attempt to steal or commit a fraudulent act (deviate) will be greatly reduced by good governance and ethics Governance determines extent Will try to deviate if they think they won’t get caught Will always deviate Will never deviate

TABLE 5.6 CONFLICTING INTERESTS – CAUSES OF JUDGEMENT BIAS

TABLE 5.7 MANAGEMENT OF CONFLICTING INTERESTS

TABLE 5.8 GUIDELINES FOR ACCEPTANCE OF GIFTS OR PREFERENTIAL TREATMENT

FIGURE 5.9ORGANIZATIONAL CULTURE, INDIVIDUAL/TEAM OUTCOMES, & ORGANIZATIONAL EFFECTIVENESS Organizational Effectiveness First Level • Attendance • Turnover • Productivity • Work Quality • Recruiting Success Second Level • Creativity/ Innovation • Problem Solving • Team Cohesiveness & Communication Third Level • Market Share • Profitability • Achievement of Formal Org. Goals Elements of Organizational Culture • Assumptions • Values • Narratives • Symbols • Heroes • Rites, Ceremonies,Rituals Individual/Team Outcomes • Job/Career Satisfaction • Organizational Identification • Job Involvement • Commitment • Discretionary Effort • Job Performance Reinforcers of Organizational Culture • Mission/Vision • Leadership skills • Growth/Development Opportunities • Team Development • Communication • Performance Management Systems • Incentives and Rewards • Human Resource Systems A Model of the Impact of Organizational Culture on Individual/Team Outcomes and Organizational Effectiveness, The Business Case for Culture Change, W. Reschke & R. Aldag, Center for Organizational Effectiveness, August 2000.

TABLE 5.9 ETHICS PROGRAM ORIENTATION TYPES

TABLE 5.10 ETHICAL CULTURE: IMPORTANT ASPECTS

TABLE 5.11 ETHICAL PROGRAMS’ USUAL DIMENSIONS

Table 5.12 Presence of Ethics & Compliance Program Elements per KPMG Forensic Integrity Survey 2013

TABLE 5.14 DEVELOPMENT AND MAINTENANCE OF AN ETHICAL CORPORATE CULTURE

TABLE 5.15 DEPTHS OF CODE COVERAGE

TABLE 5.16 DOMINANT RATIONALES FOR CODES BY REGION14

TABLE 5.17 CODE GUIDANCE ALTERNATIVES AND THE CONTROL/MOTIVATION SIGNALED

TABLE 5.18 SUBJECTS FOUND IN CODES

TABLE 5.19 EXTERNAL SHOCKS AND INFLUENCES TRIGGERING CODE MODIFICATION

TABLE 5.20 ESSENTIAL FEATURES TO DEMONSTRATE A DUE DILIGENCE DEFENCE IN RESPECT OF ENVIRONMENTAL MATTERS

TABLE 5.21 MECHANISMS FOR COMMPLIANCE ENCOURAGEMENT, MONITORING, & REPORTING WRONGDOING

FIGURE 5.10 EXECUTIVE REPUTATION & ETHICAL LEADERSHIP MORAL PERSON MORAL MANAGER Source: “Moral Person and Moral Manager: How Executives Develop a Reputation for Ethical Leadership”, L.K. Treviño et al, California Management Review, Vol. 42, No. 4, Summer 2000. Reprinted with permission.

TABLE 5.22U.S. SENTENCING GUIDELINESETHICS CRITERIA per KPMG INTEGRITY SURVEY 2005-2006

TABLE 5.23 EMERGING PUBLIC ACCOUNTABILITY STANDARDS AND INITIATIVES Information on these is downloadable from www.cengage.com/accounting/brooks

TABLE 5.24 COMPARISON OF AGENCY THEORY & STEWARDSHIP THEORY