Download

1 / 7

70 likes | 83 Views

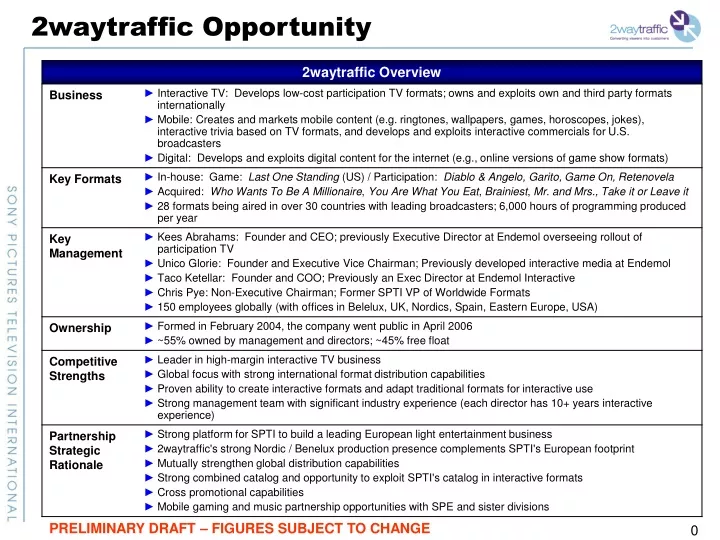

2waytraffic Opportunity. PRELIMINARY DRAFT – FIGURES SUBJECT TO CHANGE. The 2waytraffic Opportunity. SPE is proposing to acquire the Dutch light entertainment company 2waytraffic. 2waytraffic is comprised of three main business lines:

E N D

2waytraffic Opportunity PRELIMINARY DRAFT – FIGURES SUBJECT TO CHANGE

The 2waytraffic Opportunity SPE is proposing to acquire the Dutch light entertainment company 2waytraffic • 2waytraffic is comprised of three main business lines: • TV Format Licensing and Production (incl. worldwide rights to the hit format Who Wants To Be A Millionaire?); Millionaire comprises approximately 60% of the deal value and would be a driver property for Light Entertainment distribution • Participation TV: traditional Call TV and new business model Participation Advertising • Mobile content production and distribution • Founded in 2004, the company is listed on London’s AIM stock exchange with public/institutional investors holding 42% (excludes management and Directors) • An acquisition would establish SPE immediately as one of the top players in the lucrative, high-margin global light entertainment business • 2007 Revenue of approx. $104MM and recurring EBITDA of $31MM (30% EBITDA margin) • We recommend to acquire 2waytraffic at a total consideration of $353MM ($225MM upfront payment + $31MM earn-out based on Sony base case + $96MM debt) • Expected post-tax NPV of $103MM (at a 10% cost of capital) and a 20% IRR (Sony base case)

Strategic Rationale for Investment • 2waytraffic’s strong game show formats combined with SPE’s own format catalogue would provide significant leverage in the market • Capitalize on Millionaire format and other attractive assets • Leverage experienced production talent in 2waytraffic • 2waytraffic’s strong formats sales group is a well fitting complement to SPE’s global production infrastructure • Proven sales executives from Celador and Endemol, very well respected in the market • Sales presence geographically complementary (2waytraffic has strong presence in key growth markets including China, Turkey, Russia, India) • Proven capability to provide interactive features to their own and SPE’s light entertainment shows • Strong track record in establishing innovative new business models with high margins • Pioneers in Call TV business in Europe, now exploring new concept of Participation Advertising in the US and other markets (but regulatory concerns may negatively impact business) • Mobile content and mobile advertising, as well as digital games • Sony United Opportunities: possibilities for multi-platform exploitation with Playstation, Sony Electronics and Sony Ericsson

Strategic Complement 2waytraffic is very powerful addition to SPE’s production value chain Worldwide format distribution Production for local broadcaster Interactive Monetization Creative & Development Offline monetization • In-program applications • Mobile • Online • Leverage of Millionaire relationships • Global sales force • Leverage of Millionaire relationships • Merchandise • Leverage of Millionaire relationships Combined SPE and 2waytraffic creative and production pool U.S. - SPE U.K. - SPE & 2waytraffic Germany - SPE France - SPE Russia - SPE Italy - SPE Spain - SPE Netherlands - SPE & 2waytraffic Latin America - SPE

Sum-of-the-Parts Valuation The enterprise value of 2waytraffic is approx. $335MM, with 61% ascribed to the Millionaire franchise 29% premium to the current market value $185m • Implied sum-of-the-parts Equity Value per share is 91p • DCF Analysis valued the enterprise at approximately $370MM

2waytraffic Financial Overview Source: FY 06 from TWT Annual Report. Projections from Investec Securities, March 2007. EBIT excludes goodwill amortization and other one-time items. PRELIMINARY DRAFT – FIGURES SUBJECT TO CHANGE

Financial Analysis: Sony Case After first-stage of detailed due diligence, SPTI established a more conservative Sony Base case vs. the Management Case • Assumes flat performance of the TV format business and a significant reduction to Mobile and Participation Advertising businesses • Synergies assumption: no synergies in 2008; revenue enhancement of 10% of the TV business revenues from 2009 onwards at a margin of 30%; no cost synergies • Immediately accretive to Sony EBIT: expected to provide EBIT after PPA of $5.1MM in CY 08 and $9.6MM in CY 09