Download

1 / 23

240 likes | 555 Views

Short-term Financing. FIN 340 Prof. David S. Allen Northern Arizona University. Introduction. The firm must decide the mix of short-term debt, long-term debt, and equity used to finance its assets. We will examine various sources of short-term financing, and their costs: Accruals

E N D

Short-term Financing FIN 340 Prof. David S. Allen Northern Arizona University

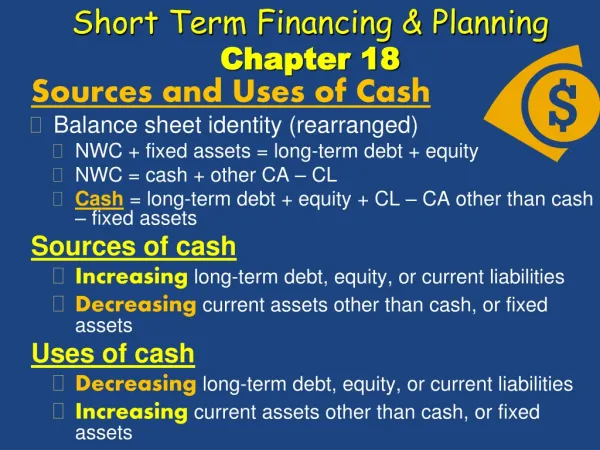

Introduction The firm must decide the mix of short-term debt, long-term debt, and equity used to finance its assets. We will examine various sources of short-term financing, and their costs: Accruals Accounts payable Banks loans Commercial paper

Accruals Arise from the fact that firms do not pay their employees on a daily basis. Typically paid weekly, biweekly, or semi-monthly. Also arise from accumulation of taxes payable. “Free” source of financing Arises spontaneously Firm has little control over the level of accruals: Pay schedule is usually determined by industry norms. Tax payment schedule is set by law.

Accounts payable (trade credit) Firms generally buy from other firms on credit. Spontaneous source of financing. Small firms often don’t qualify for other forms of financing, so trade credit becomes its largest source of non-equity capital. Accounts payable = (avg. payment period) x (avg. daily purchases)

Accounts payable (trade credit) Cost of Trade Credit If a firms buys on credit with discount terms, e.g. 2/10 net 30 For a $100 purchase “True” price = $98 For a finance charge of $2, the buyer can obtain another (30-10)=20 days of credit Cost of foregoing the discount

Accounts payable (trade credit) Cost of foregoing the discount Can be reduced by “stretching accounts payable” But, may cause problems with suppliers Decision Criteria If the firm has an alternative source of financing, such as a bank line of credit, that is less expensive than the supplier provided “cost of foregoing the discount”, it should borrow from the bank and take the discount by paying earlier.

Accounts payable (trade credit) Components of Trade Credit: Free versus Costly Free trade credit = credit received during the discount period Costly trade credit = credit beyond the discount period Firms should always use the free component, but should use the costly component only if it has a lower cost than other available alternatives.

Short-Term Bank Loans Non-spontaneous source of financing Second in importance, after trade credit, as a source of short-term financing for non-financial firms. Maturity Most are for a year or less Many are 90 day notes Bank may refuse to renew if the borrower’s financial condition has deteriorated.

Short-Term Bank Loans Promissory Note Specifies: Amount borrowed Interest rate Repayment schedule (lump sum or annuity) Collateral Others terms Proceeds are deposited in the borrowers checking account.

Short-Term Bank Loans Compensating Balances Banks sometimes require borrowers to maintain an average (or even minimum) checking account balance equal to 10% to 20% of the loan principal. The result is to increase the effective interest rate on the loan, since interest is paid on the full loan amount, but only a portion is usable.

Short-Term Bank Loans Informal Line of Credit An informal agreement between a firm and its bank indicating the maximum credit the bank will extend to the borrower. Revolving Credit Agreement A formal line of credit, and legal obligation of the bank. Firm must pay a commitment fee on the unused portion, usually in monthly installments. Interest is paid on the amount actually borrowed. Interest rate is usually pegged to the prime rate or some other short-term rate (e.g. t-bill rate). Clean-up clause: requires the borrower to reduce the loan balance to zero at least once per year (not permanent capital).

The Cost of Bank Loans Rates are higher for riskier borrowers, and for smaller loans, due to the fixed cost of making and servicing loans. Prime rate= 3.25% in November 2009. Available only to bank’s most creditworthy customers. Others pay “prime plus” some specified percentage points.

The Cost of Bank Loans Promissory note elements: Interest only Interest paid during life of loan Principal repaid at maturity Amortized Also known as an “installment loan.” Each payment is part interest, and part principal. Collateral May be inventory, or receivables. UCC-1 and Security Agreement filing with state to evidence collateral. Prevents borrower from using same collateral on a different loan. Specifies conditions under which collateral can be seized.

The Cost of Bank Loans Promissory note elements: Loan guarantees: for small corporations, the larger stockholders will have to personally guarantee the loan. Nominal (stated) interest rate: Fixed rate Floating rate: typical for most loans of more than $25,000 360 versus 365 day year Frequency of interest payments: usually calculated daily, but paid monthly Maturity: Long-term loans always have a stated maturity date Short-term loans may be outstanding (rolled over) for a long time.

The Cost of Bank Loans Promissory note elements: Discount interest: interest is paid in advance, reducing the usable loan amount, and thus increasing the effective interest rate. Other cost elements: Compensating balance Commitment fee Key-person insurance: bank may require key persons to carry life insurance to pay off the loan in the event of their death.

The Cost of Bank Loans Annual percentage rate = APR (as defined in Truth in Lending Act) = effective periodic rate annualized without recognizing the effects of compounding. = effective periodic rate * number of interest periods in a year The APR is calculate as:

The Cost of Bank Loans Effective annual rate = EAR (a.k.a. Effective Annual Yield or EAY, defined in Truth in Savings Act) = effective periodic rate annualized to incorporate the effects of compounding. = (1 + effective periodic rate)number of interest periods in a year – 1 The EAR overcomes the problems noted above for the APR, but is not required reporting for loans. It is used, however, in reporting rates earned on savings.

The Cost of Bank Loans Consider a loan of $100,000 at a nominal (stated) rate of 8%, with a 360 day year (used by most banks). Regular (Simple) Interest Interest rate per day = nominal rate / 360= .08 / 360 = 0.0002222222 So, the interest on a three month (90 day) loan would be: Interest = (loan period)(daily rate)(amount borrowed)= (90 days)(0.0002222222 / day)($100,000) = $2,000.00 APR = (2,000 / 100,000)(365 / 90) = 0.08111 = 8.111% EAR = (1 + 2,000 / 100,000)365/90 – 1 = .08362 = 8.362%

The Cost of Bank Loans Consider a loan of $100,000 at a nominal (stated) rate of 8%, with a 360 day year (used by most banks). Discount Interest Interest rate per day = nominal rate / 360= .08 / 360 = 0.0002222222 So, the interest on a three month (90 day) loan would be: Interest = (loan period)(daily rate)(amount borrowed)= (90 days)(0.0002222222 / day)($100,000) = $2,000.00 This $2,000 is subtracted from the loan amount, and the borrower has use of only $98,000. APR = (2,000 / 98,000)(365/90) = 0.08277 = 8.277% EAR = (1 + 2,000 / 98,000)365/90 – 1 = .08538 = 8.538%

The Cost of Bank Loans Consider a loan of $100,000 at a nominal (stated) rate of 8%, with a 360 day year (used by most banks). Compensating Balance and Simple Interest Interest rate per day = nominal rate / 360= .08 / 360 = 0.0002222222 So, the interest on a three month (90 day) loan would be: Interest = (loan period)(daily rate)(amount borrowed)= (90 days)(0.0002222222 / day)($100,000) = $2,000.00 Compensating balance = 20% = $20,000 APR = (2,000 / 80,000)(365/90) = 0.10139 = 10.139% EAR = (1 + 2,000 / 80,000)365/90 – 1 = .10533 = 10.533%

Choosing A Bank Willingness to Assume Risks Depends on Personalities of bank officers Characteristics of its deposit liabilities Geographic and industry diversification of lending portfolio Advice and Counsel Bank lending officer may have valuable knowledge and experience that could be used by borrowing firms. Loyalty to Customers Will the bank work with customers experiencing difficulties, or call its loans?

Choosing A Bank Specialization Some large banks have departments that specialize in certain types of loans, e.g. agricultural. Lending officer will understand the market better, and be more receptive to borrowers. Maximum Loan Size Maximum loan to any one customer is limited to 15% of capital stock plus retained earnings. So, large firms will need to work with larger banks.

Commercial Paper Short term, unsecured promissory note issued by large, creditworthy firms. Sold to other businesses, insurance companies, mutual funds, and banks. Maturity and Cost Must be less than 271 days, to avoid SEC registration. Interest cost is below prime rate, but above T-bill rate. Use of Commercial Paper Usually restricted to firms with net worth of $100,000,000 or more, and annual borrowings of $10,000,000 or more.