Download

1 / 31

320 likes | 527 Views

Quantitative Analysis. Later lecture if time. Qualitative Analysis. Later Lecture if time. Momentum Investing. Later Lecture if time. Income Investing. Later Lecture if time. GARP Investing. Later Lecture if time. Value Investing. Later Lecture if time. Growth Investing. Later Lecture if time.

E N D

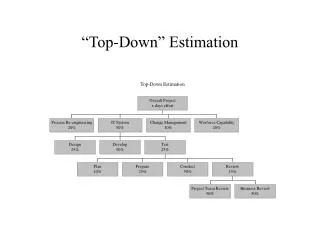

1. Top Down Approach to Investing Company Analysis

Fundamental Analysis

2. Quantitative Analysis Later lecture if time

3. Qualitative Analysis Later Lecture if time

4. Momentum Investing Later Lecture if time

5. Income Investing Later Lecture if time

6. GARP Investing Later Lecture if time

7. Value Investing Later Lecture if time

8. Growth Investing Later Lecture if time

9. Determining Value Based on Dividends Later Lecture if time

10. Determining Value Based on Cash Flow Later Lecture if time

11. Determining Value Based Upon P/E and EPS Forecasts The majority of the time the P/E is calculated using EPS from the last four quarters

Called the trailing P/E

Analysts attempt to estimate EPS for the next four quarters

P/E based on estimated EPS are called leading, projected, or forecasted P/E

12. Price/Earnings Ratios Historically, the average P/E ratio in the market has been around 15-25.

Fluctuates depending on economic conditions at the time

P/E ratios also vary widely between different companies and industries

13. Price/Earnings Ratios Theoretically, a stock�s P/E tells us how much investors are willing to pay per dollar of earnings

For this reason it is also called the �multiple� of a stock

In other words, a P/E ratio of 20 suggests that investors in the stock are willing to pay $20 for every $1 of earnings the company generates

14. Price/Earnings Ratios Stock prices reflect what investors think a company will be worth and so future growth is already accounted for in the stock price

The P/E ratio is actually a reflection of the market�s optimism concerning a firm�s growth prospects

15. Price/Earnings Ratios A company with a P/E higher than the market or industry average means the market is expecting big things over the next few months or years

A company with a high P/E ratio will eventually have to live up to the high rating by either substantially increasing its earnings or the stock price will need to drop

16. Price/Earnings Ratios You can�t compare P/E ratios of two totally different companies to determine which is a better value!

17. Price/Earnings Ratios It�s difficult to say in general whether a particular P/E is high or low without taking into account two main factors

Company growth rates.

How fast has the company been growing in the past, and are these rates expected to increase (or at least continue) into the future?

Something isn�t right if the company has only grown at 5% in the past and yet has a P/E in the stratosphere.

Industry

Comparing companies is useful only if they are in the same industry.

For example, consumer staples typically have low multiples because they are low growth, yet stable industries.

The technology industry, on the other hand, is characterized by screaming growth rates and constant change.

18. Problems Associated with P/E Analysis Accounting

Earnings is an accounting figure that includes non-cash items

To make matters more complicated, EPS can be twisted and prodded into many different numbers depending on how you do the books

It is difficult to know if you are comparing the same figures or apples to oranges

19. Problems Associated with P/E Analysis Inflation

In times of high inflation, inventory and deprecation costs tend to be understated because the replacement costs of costs of goods and equipment rises with the general level of prices

Thus, P/E ratios tend to be lower during times of high inflation because the market sees earnings as artificially distorted upwards

As with all ratios, it�s more valuable to look at the P/E over time in order to determine the trend

Inflation makes this difficult, as past information is less useful today

20. Problems Associated with P/E Analysis Many interpretations

A low P/E does not necessarily mean that a company is undervalued

Rather, it could mean that the market believes the company will be in trouble in the short future

Stocks that go down usually do so for a reason

It may be that a company has warned that earnings will come in lower than expected

This wouldn�t be reflected in a trailing P/E ratio until earnings are actually released, during which time the company may look undervalued

21. Forecasting Earnings Per Share Our dilemma

Our solution

Three companies specialize in providing forecasts of earnings and collecting multiple forecasts

IBES

Zacks

First Call

22. Forecasting Earnings Per Share IBES

Institutional Brokers Estimate System

Headquartered in New York City

Has been in the earnings forecasting business since 1971

Gathers financial data on 18,000 companies in 48 countries

For IBES information, visit Motley Fool�s Website: www.fool.com

23. Forecasting Earnings Per Share Zacks Investment Research

Headquartered in Chicago

Business for more than a decade

Compiles data from thousands of firms

http://my.zacks.com or http://biz.yahoo.com/zacks/extreme.html

24. Forecasting Earnings Per Share First Call

Financial research subsidiary of the Carson Group

New York City

www.firstcall.com

25. Forecasting Earnings Per Share IBES and Zacks employee make periodic phone calls to professional securities analysts, financial analysts, and investors at mutual funds, banks, and brokerage houses around the world and solicit their forecasts of corporations� earnings per share for 4 quarters of future earnings and up to 5 years of annual earnings.

They analyze these earnings forecast and publish the high, low, average, and median earnings the experts forecast for each firm and each future time period

The data is updated frequently so that it represents current estimates of the continuously changing consensus forecast

They also provide an annual earnings growth rate for each corporation

26. Cautions about EPS estimates Forecasters ten to overstimate earnings per share

Forecasters tend to revise their forecasts downward to improve their accuracy as the earnings announcements date draws near

Forecasters seem to be reluctant to say negative things about security issuers

Forecasters issue many more buy than sell recommendations

May want to use whisper numbers

27. Using P/E Ratios to Determine Value Let�s value APP using P/E ratios, earnings forecasts, and historical growth rates.

Go to http://finance.yahoo.com

Type in APPX for symbol

Click on Analyst Estimates

28. Using P/E Ratios to Determine Value

29. Using P/E Ratios to Determine Value Here is where the judgment call comes in:

I am going to use the highest P/E ratio for two reasons:

APPX has historically had a high P/E

Their growth rate is well above P/E

I am going to use the average and lowest estimate of EPS for two reasons:

Drug has not been approved

Still 6 months from year end

30. Using P/E Ratios to Determine Value Given these judgment calls, my range for APPX is:

$46.905 to $54.28

Currently it is selling for $31.50

31. PEG Ratio The relationship between the P/E ratio and earnings growth tells a much more complete story than the P/E on its own

The number used for annual growth rate can vary

It can be forward (predicted growth) or trailing

Looking for a number less than or equal to 1

32. PEG Ratio PEG Ratio for APPX is .82

APPX is a BUY using P/E, PEG, and some technical indicators