Download

1 / 14

140 likes | 161 Views

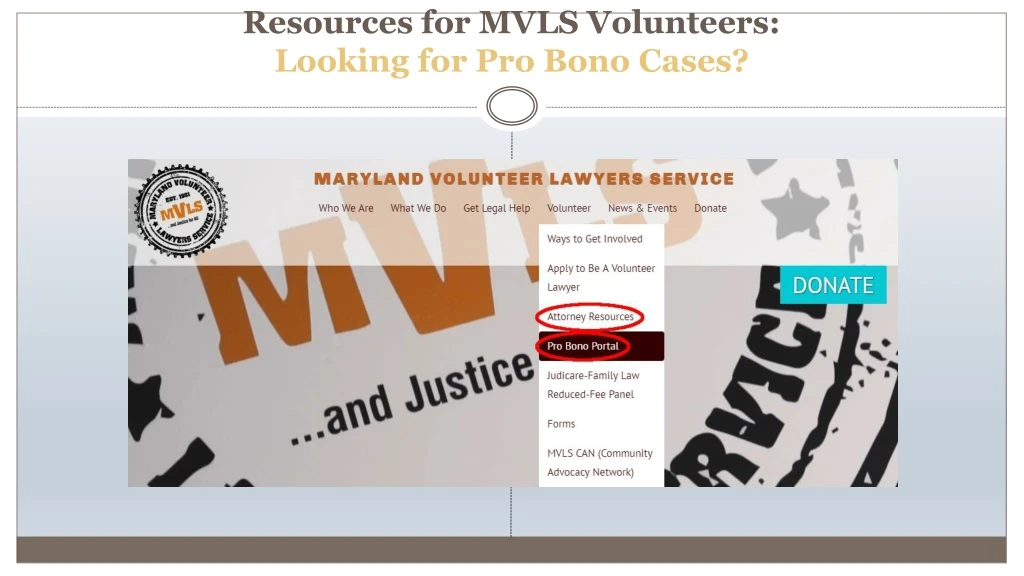

Find pro bono cases and get involved with the Maryland Volunteer Lawyers Service through their new Pro Bono Portal. Visit www.mvlslaw.org/events for more information on upcoming training and clinics!

E N D

facebook.com/MVLSProBono/ Maryland Volunteer Lawyers Service @MVLSProBono Visit www.mvlslaw.org/events for more info on upcoming training and clinics!

The Collection Due Process (CDP) Case(From Cradle to Grave) Stephen P. Kauffman, Esquire Skeen & Kauffman,llp 9256 Bendix road, unit 102 columbia, MD 21045 SKauffman@SKauffLaw.com (410) 382-9606 Results, not excuses

Triggers Giving Rise to IRS Contact • Balance Due on Filed Return • Highest Risk - - Will Receive Service Center Notices • Failure to File • High Risk - - IRC Section 6020(b) SFR or . . . • Inaccurate Return • Difficult to Quantify Risk in Abstract • Likelihood of Audit/Results/Appeal Process

Notice Sequence Tax Delinquency Starts Notice Sequence • Notice of Assessment and Demand for Payment • Balance Due • Final Notice before Levy (Triggers Right to File CDP) • NFTL Filed (Triggers Right to File CDP)

Responses to Notices Responses to Final Notice Nothing (Enforced Collection Action) NFTL Levy/Seizure Issuance of Passport Collection Appeal (Form 9423) Request for Taxpayer Assistance Order (Form 911) CDP (Form 12153)

Effect of Filing CDP Request • Stays Enforced Collection • Tolls Limitations on Collection • Review by Independent Appeals Officer • Judicial Review if timely. • Untimely Right to Equivalent Hearing if within 1 year • Beware Premature Filing

Exceptions to CDP Right • Collection in Jeopardy • State Tax Refund Levy • Federal Contractor Levy • Disqualified Employment Tax Levy (the 2-year Rule)

Issues That Can Be Raised in CDP Hearing • Procedural Defect • Underlying Liability (if no prior ability to contest) • Spousal Defenses • Appropriateness of Collection • Collection Alternatives • IA • OIC • CNC

Process • Duration • Record Rule • Need to Document • Avoid Excess and Duplication • Write for the Court

Appeals Officer Determination • All Procedural Requirements Met • Issues Raised by Taxpayer • Proposed Collection Action balances need for the efficient collection of taxes with the legitimate concern that any collection action be no more intrusive than necessary

Post Determination • Judicial Review • Tax Court Petition within 30 days • De Novo v. “On the Record” • Appeal Beyond Tax Court • Appeals Retained Jurisdiction • Enforce Determination • Changed Circumstances

Q & A Any further questions or suggestions, contact Steve at skauffman@skaufflaw.com or (410) 382-9606 (Mobile) (410) 625-2228 Ext. 1 (Office) Results, Not Excuses A Passion for the Process