Download

1 / 11

110 likes | 257 Views

Globalisation and the knowledge economy. Ian Brinkley Director Knowledge Economy Programme Work Foundation. Globalisation – the story so far.

E N D

Globalisation and the knowledge economy Ian Brinkley Director Knowledge Economy Programme Work Foundation

Globalisation – the story so far • In OECD economies the big structural changes are driven primarily by technology and markets, with globalisation accelerating and reinforcing these fundamental shifts; • All OECD economies have seen an expansion of the technology and knowledge based industries and these have uniformly been big generators of new jobs; • Rapid growth in world trade and entry of BRIC economies over past decade has been associated with falling unemployment and rising living standards across the OECD; • Like all structural change, globalisation creates highly visible losers and economic minuses and less visible winners and economic pluses.

Globalisation and manufacturing • Even in the internationally exposed sectors of the economy such as manufacturing, trade has accounted for between 10 and 30 per cent of jobs lost in the decade to 2002 (Rowthorne and Coutts); • Many of the trade related impacts on jobs come from North-North rather than North-South trade (eg cars, engineering, high tech); • China is a low innovation, assembly economy with many exports dominated by factories owned or operating on behalf of US, Europe and Japanese multi-nationals; • Some of the increase in imports from China to Europe is replacing imports we would have otherwise taken from US and Japanese factories; • Some economies such as the UK have been unable to exploit the Chinese demand for high quality production goods in contrast to, say, Germany.

Offshoring of services • No statistics on offshoring impact, so have to rely on indirect measures, one-off studies and monitoring; • Most US studies suggest scale of actual job losses to offshoring is very small share of “natural” job loss rate in the economy; • European Restructuring Monitor in 2005 found just over 5 per cent of all job losses across the EU from restructuring due to offshoring; • UK “offshoring scare” in 2003: subsequent DTI/ONS studies show employment went up in UK callcentres and in occupations thought most vulnerable; • Trade in technology and knowledge based services (excluding transport, travel and tourism) is almost all North-North; • UK trade in services with India is small and – excluding travel and transport – we export more services by value to India than we import.

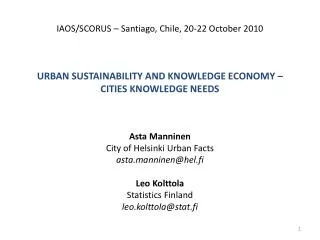

UK-India knowledge services trade in 2004financial, business, high tech, cultural services and royalties and licence fees. IT related are computer, information, and communication services. Source: Pink Book, 2006 edition.

Globalisation responses to competition from low wage manufacturing exports • High tech manufacturing now accounts for a higher share of exports in UK, Germany, France compared with the early 1990s – but not in US and Japan; • Except for the UK, the change has been modest and the vast majority of EU manufacturing exports are still from medium to low tech industries; • There has been no shift in trade towards services across the OECD; • The big exception is the UK – the only major OECD economy (so far) to specialise in technology and knowledge service trade

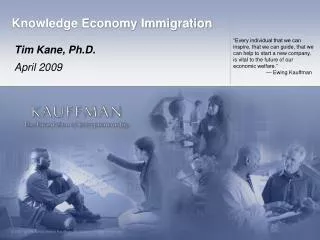

Trading in ideas and knowledge - UK becomes a world leaderBalance of trade as share of GDP in 2005WF definition: business services, finance, high tech, telecommunications, cultural, education: Source: Eurostat/OECD. All figures 2005 except Japan, 2004.)

Looking to the future – are we being too complacent? • Unprecedented scale of Chinese and Indian economies makes previous experience with OECD Asian economies unreliable guide; • Technology and increased supply of knowledge workers will create “high skill-low wage” economies across the OECD; • The first “great unbundling” of manufacturing production to Asia will be followed by a second “great unbundling” of service jobs; • The “great doubling” will flood world labour markets with unskilled, capital poor labour – pushing wages down among unskilled workers.

Looking to the future – an alternative view • Although trade will become more important as an agent of change, technology and markets will remain the key drivers of economic restructuring in major OECD economies; • The pace of structural change in the exposed sectors of the economy – manufacturing and some knowledge based services - will speed up as both North-North and North-South trade increase; • Big potential markets in non-OECD economies from what the World Bank terms the “global middle class” who will actively participate in the global economy and demand high quality products and high quality services; • Global supply of “knowledge workers” may struggle to keep up with demand, with OECD economies increasingly competing to attract “brightest and best”.

Looking to the future – how do we cope? • A more mature political and public debate – too easy for politicians and pundits to blame globalisation for all the economic and social ills of the world; • Investment in human capital at all levels, including expanding higher education, and developing the science and technology base; • A key issue will be how to cope with ever faster structural change – whether generated by technology or trade – and ensure individuals and communities that lose out are effectively helped and compensated; • One option is to move further towards the “flexisecurity” model of Nordics and Netherlands – liberal markets (including liberal migration policies), strong active labour market policies and more generous but employment friendly social welfare safety nets.